Shareholders of GoDaddy would probably like to forget the past six months even happened. The stock dropped 32.9% and now trades at $119.86. This might have investors contemplating their next move.

Is now the time to buy GoDaddy, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Why Do We Think GoDaddy Will Underperform?

Even though the stock has become cheaper, we don't have much confidence in GoDaddy. Here are three reasons why GDDY doesn't excite us and a stock we'd rather own.

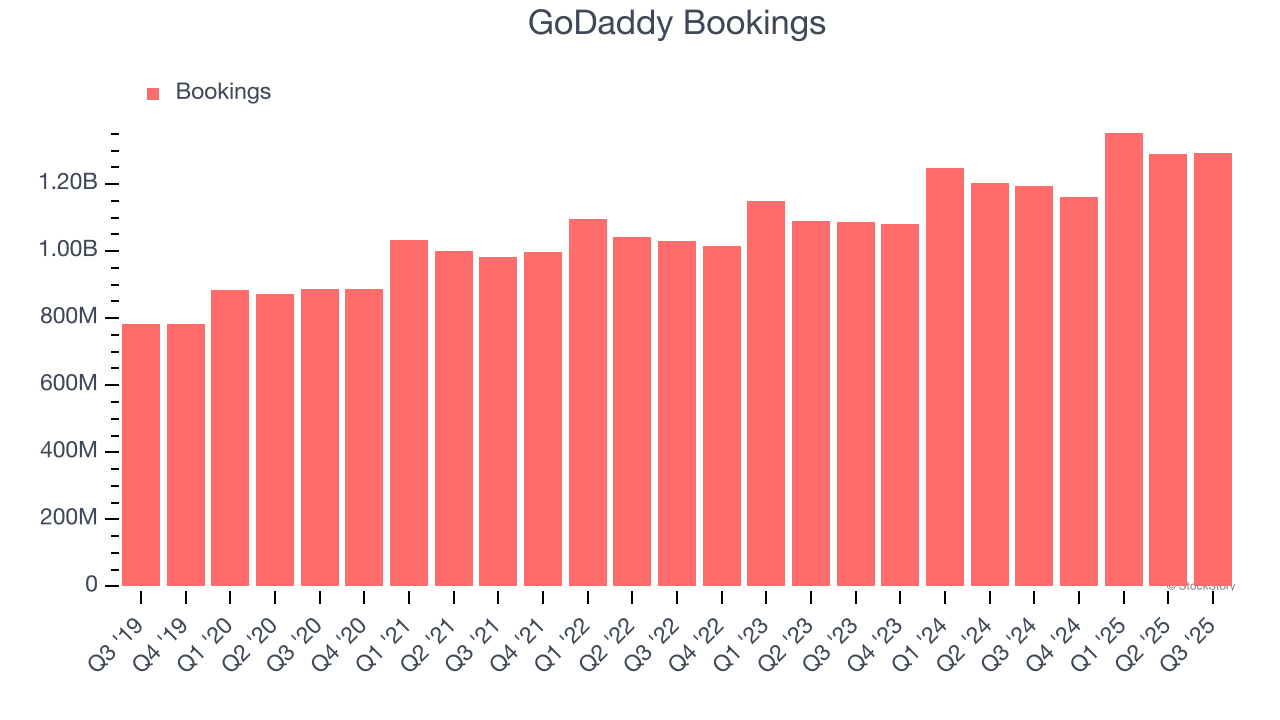

1. Weak Bookings Point to Soft Demand

In addition to reported revenue, it is useful to analyze bookings for GoDaddy because they show the value of contracts signed in a period. It could be a better indicator of demand, as reported revenue is subject to recognition rules based on when products and services are delivered.

GoDaddy’s bookings came in at $1.29 billion in Q3, and over the last four quarters, its year-on-year growth averaged 7.8%. This performance was underwhelming and suggests that increasing competition is causing challenges in securing new contracts or renewals.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect GoDaddy’s revenue to rise by 6.5%, close to its 8.6% annualized growth for the past five years. This projection doesn't excite us and implies its newer products and services will not catalyze better top-line performance yet.

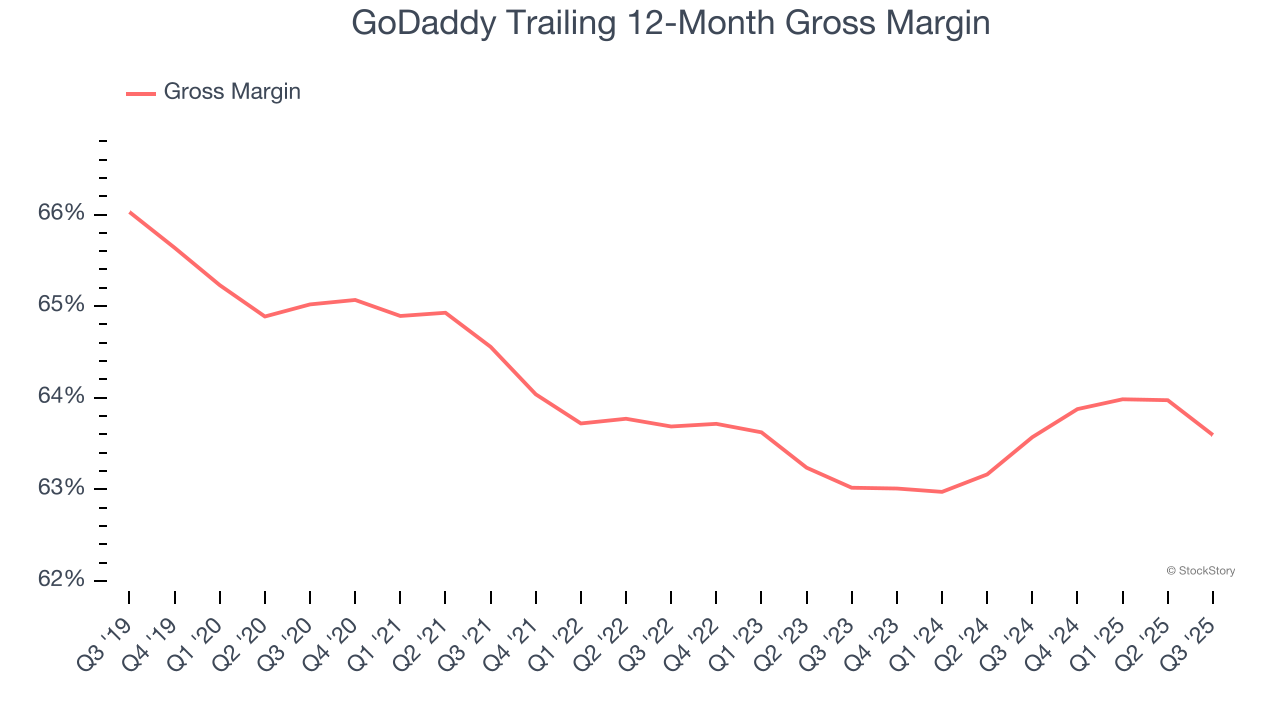

3. Low Gross Margin Reveals Weak Structural Profitability

For software companies like GoDaddy, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

GoDaddy’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 63.6% gross margin over the last year. Said differently, GoDaddy had to pay a chunky $36.41 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. GoDaddy has seen gross margins improve by 0.6 percentage points over the last 2 year, which is slightly better than average for software.

Final Judgment

GoDaddy doesn’t pass our quality test. Following the recent decline, the stock trades at 3.2× forward price-to-sales (or $119.86 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are superior stocks to buy right now. We’d suggest looking at one of our top digital advertising picks.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.