Although Independent Bank (currently trading at $67.05 per share) has gained 13.5% over the last six months, it has trailed the S&P 500’s 23.8% return during that period. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Independent Bank, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

Why Is Independent Bank Not Exciting?

We don't have much confidence in Independent Bank. Here are three reasons we avoid INDB and a stock we'd rather own.

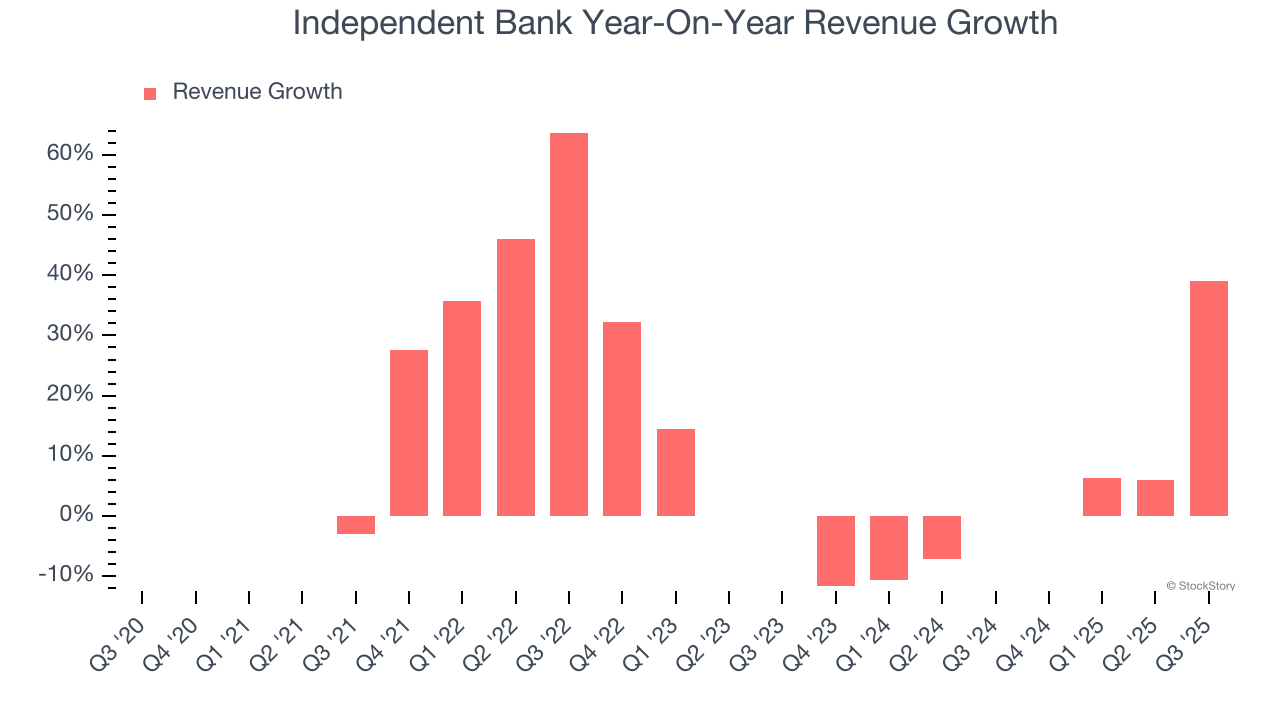

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Independent Bank’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 1.6% over the last two years was well below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

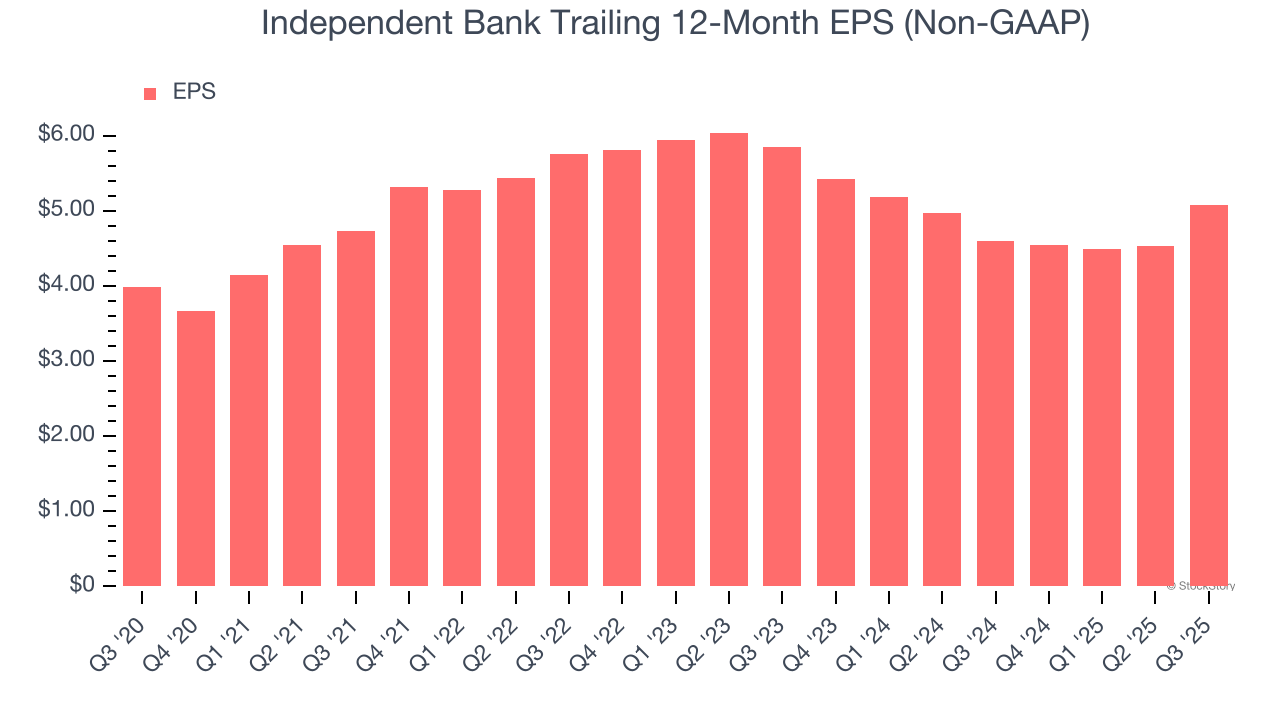

2. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Independent Bank’s EPS grew at an unimpressive 4.9% compounded annual growth rate over the last five years, lower than its 9.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

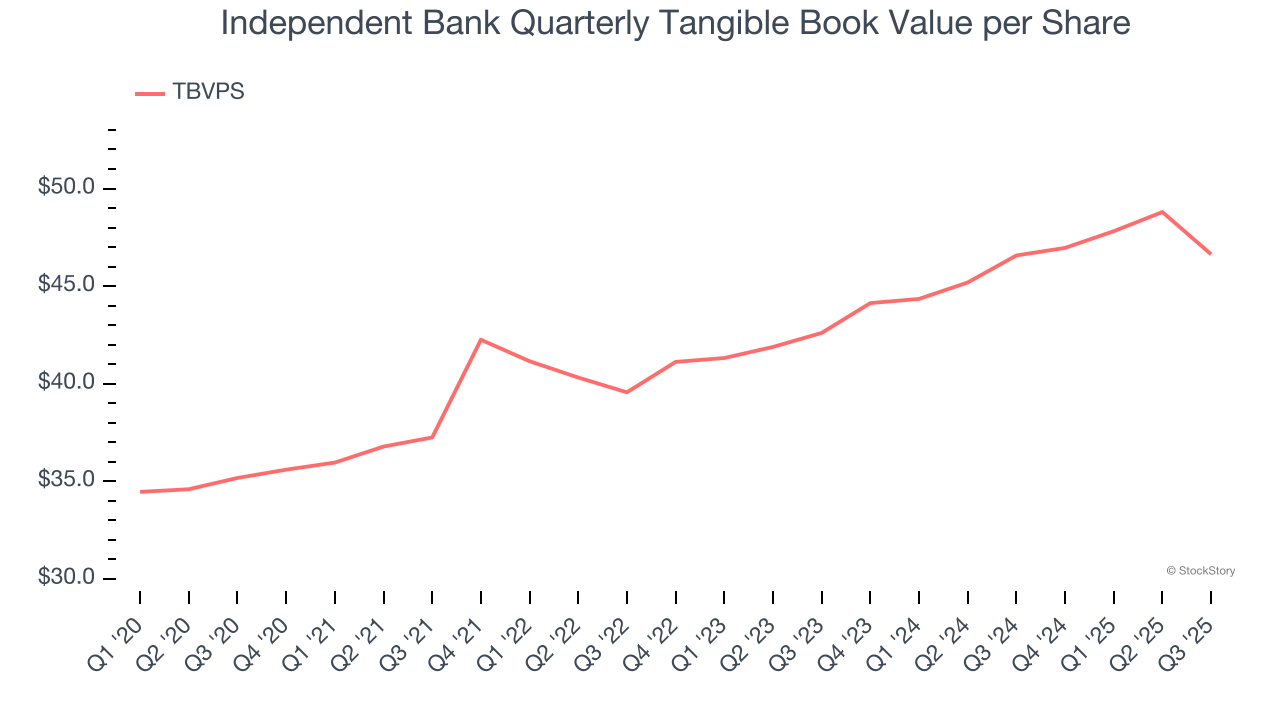

3. Substandard TBVPS Growth Indicates Limited Asset Expansion

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

Although Independent Bank’s TBVPS increased by 5.8% annually over the last five years, growth has recently decelerated a bit to a sluggish 4.6% over the past two years (from $42.60 to $46.63 per share).

Final Judgment

Independent Bank’s business quality ultimately falls short of our standards. With its shares underperforming the market lately, the stock trades at 0.9× forward P/B (or $67.05 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Would Buy Instead of Independent Bank

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.