Genuine Parts currently trades at $130.33 per share and has shown little upside over the past six months, posting a middling return of 4.7%.

Is there a buying opportunity in Genuine Parts, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Genuine Parts Will Underperform?

We don’t have much confidence in Genuine Parts. Here are three reasons why there are better opportunities than GPC, plus one stock we’d rather own.

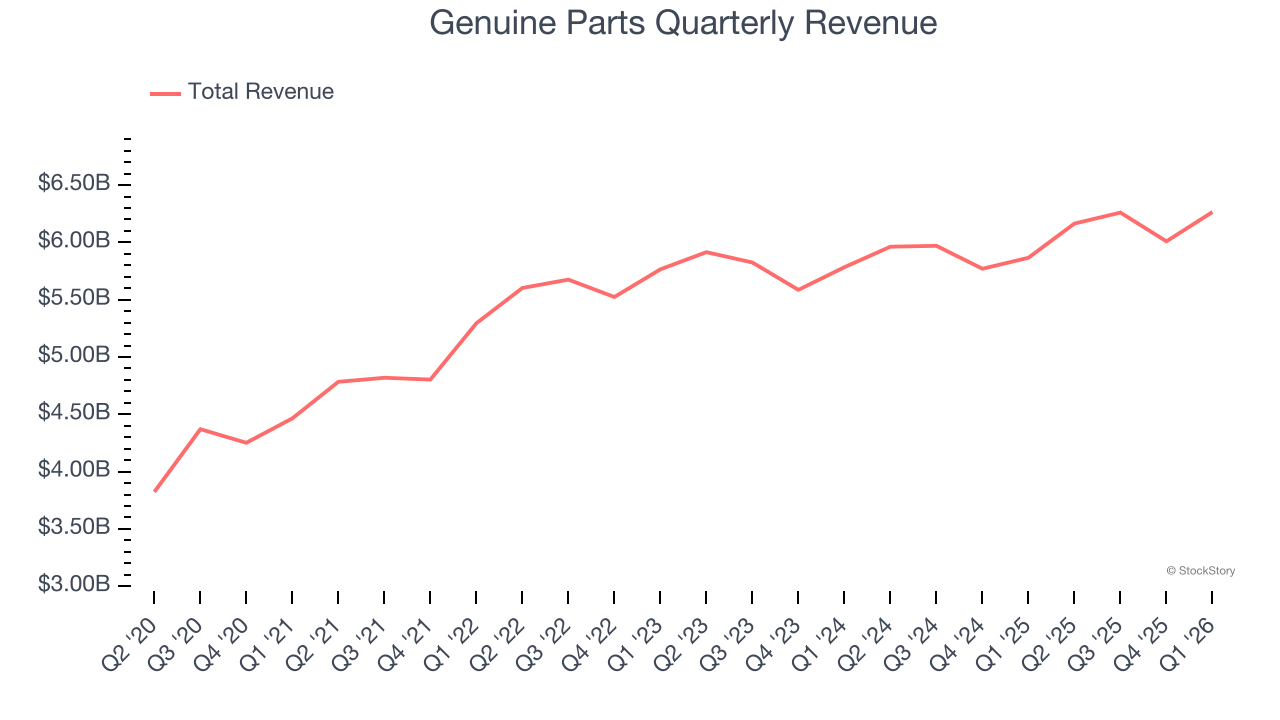

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Genuine Parts’s sales grew at a sluggish 3.1% compounded annual growth rate over the last three years. This fell short of our benchmark for the consumer retail sector.

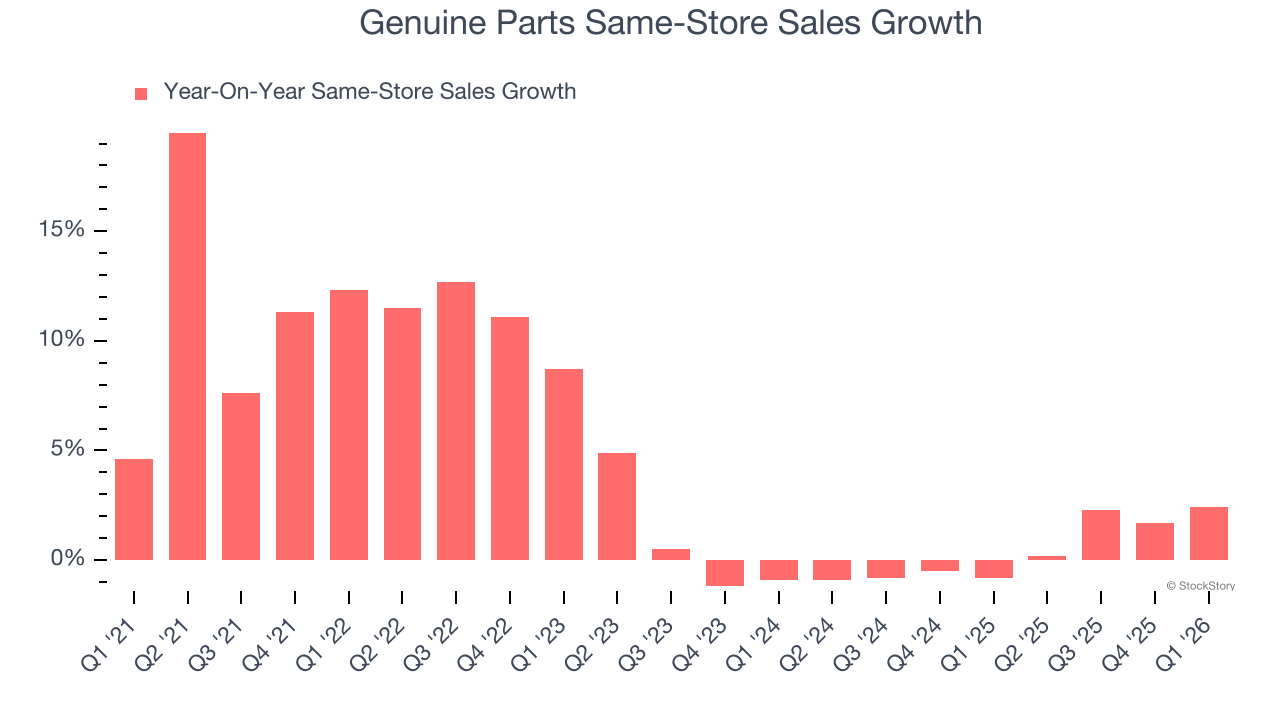

2. Flat Same-Store Sales Indicate Weak Demand

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Genuine Parts’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat.

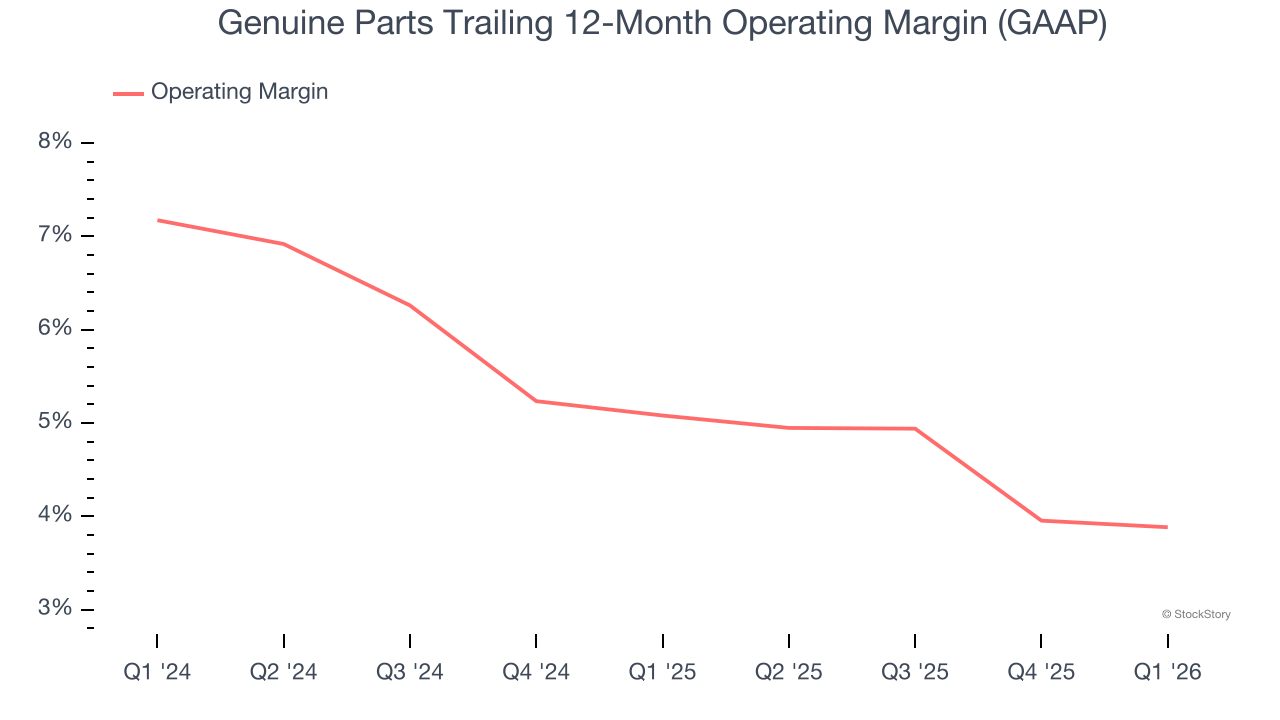

3. Weak Operating Margin Could Cause Trouble

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Genuine Parts was profitable over the last two years but held back by its large cost base. Its average operating margin of 4.5% was weak for a consumer retail business. This result isn’t too surprising given its low gross margin as a starting point.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Genuine Parts, we’ll be cheering from the sidelines. That said, the stock currently trades at 16.8× forward P/E (or $130.33 per share). At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere. We’d suggest looking at the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.