Expand Energy has been treading water for the past six months, holding steady at $109.39. However, the stock is beating the S&P 500’s 5.5% decline during that period.

Given the relative strength, is there still a buying opportunity in EXE? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Are We Positive On Expand Energy?

Rebranded from Chesapeake Energy in 2024 after emerging from bankruptcy, Expand Energy (NASDAQ: EXE) produces natural gas, oil, and natural gas liquids from underground shale formations in Louisiana, Pennsylvania, Ohio, and West Virginia.

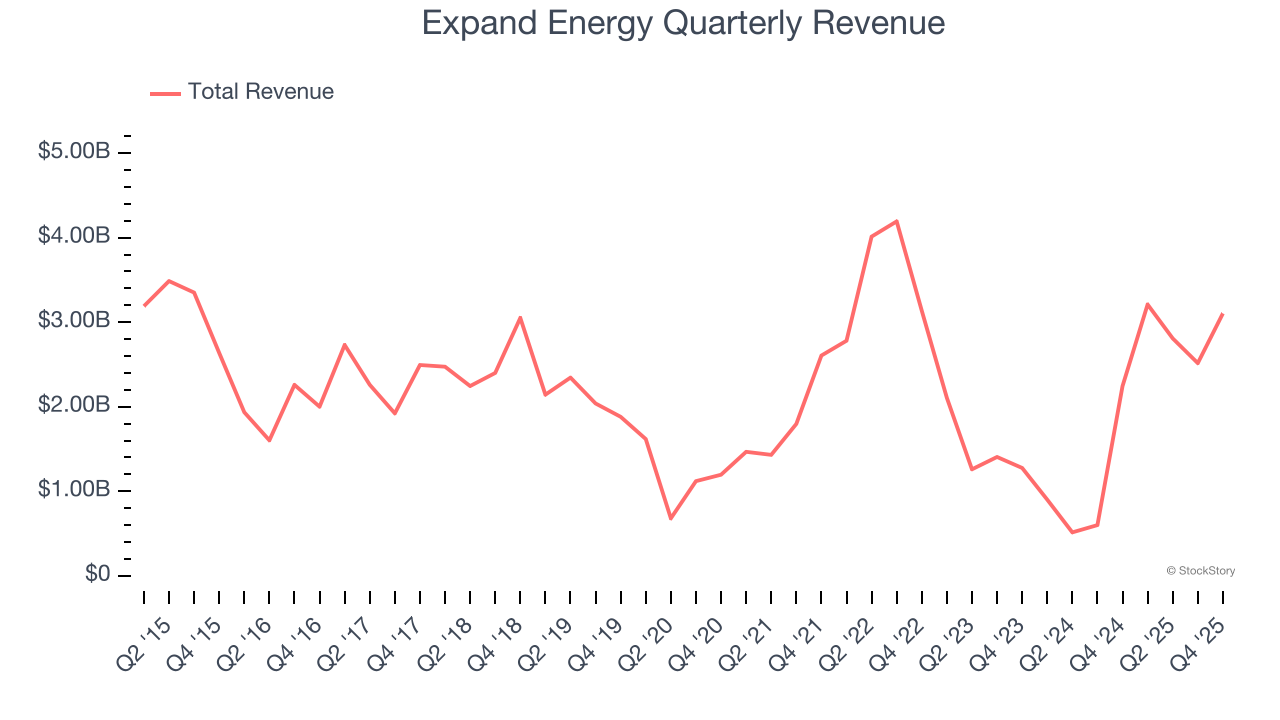

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Over the last five years, Expand Energy grew its sales at an excellent 20.3% compounded annual growth rate. Its growth surpassed the average energy upstream and integrated energy company and shows its offerings resonate with customers.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

In Energy, scale separates fragile single-asset producers from platform-style businesses that generate revenue across entire basins and infrastructure networks.

Expand Energy’s $11.64 billion of revenue in the last year is top-tier for the industry, suggesting the company has hit a level of diversification where investors can sleep easy at night.

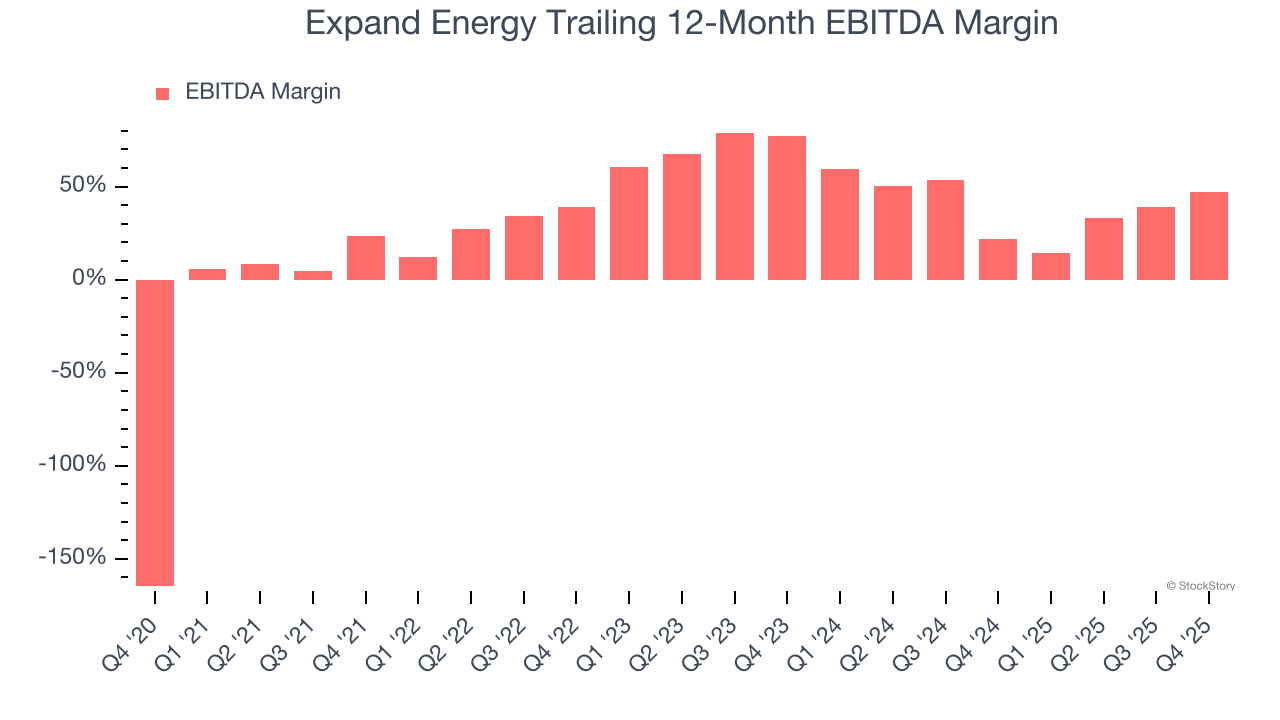

3. EBITDA Margin Rising, Profits Up

Adjusted EBITDA margin captures the true operating profitability of an energy producer by removing accounting noise around depletion and capitalized drilling costs. It reveals how much cash the asset base generates before capital structure and reinvestment requirements shape reported earnings.

Analyzing the trend in its profitability, Expand Energy’s EBITDA margin rose by 23.6 percentage points over the last year, showing its efficiency has meaningfully improved. . Its EBITDA margin for the trailing 12 months was 46.8%.

Final Judgment

These are just a few reasons Expand Energy is a rock-solid business worth owning, and with its recent outperformance amid a softer market environment, the stock trades at 12× forward P/E (or $109.39 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.