As the global financial markets navigate the opening weeks of 2026, the spotlight has once again intensified on Veldhoven, Netherlands. ASML Holding N.V. (NASDAQ: ASML), the world’s sole provider of the extreme ultraviolet (EUV) lithography machines required to print the world’s most advanced microchips, has solidified its role as the ultimate bellwether for the technology sector. With a market capitalization now comfortably exceeding the $500 billion milestone, ASML’s recent guidance and the high-volume rollout of its "High-NA" EUV systems are dictating the pulse of the US semiconductor supply chain and shaping the strategic roadmap for the world’s largest chipmakers.

The immediate implications of ASML’s current trajectory are profound. As the industry transitions into what analysts are calling the "AI Infrastructure Supercycle," the demand for specialized hardware to support generative AI and high-performance computing (HPC) has reached a fever pitch. In mid-January 2026, a surge in sentiment across the semiconductor equipment sector—often referred to as "semicap"—was triggered by record capital expenditure (capex) forecasts from ASML’s primary customers. This has effectively silenced concerns over a potential slowdown in the broader tech sector, positioning the lithography giant as the linchpin of global technological sovereignty.

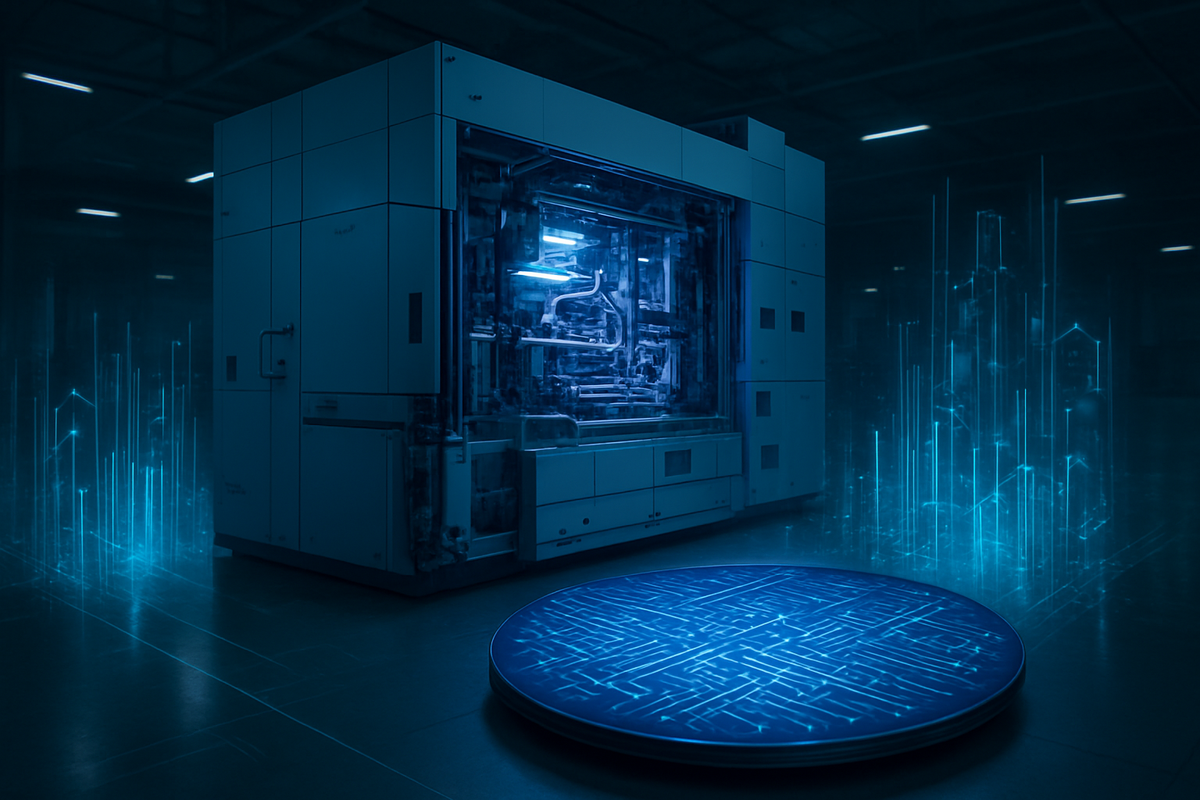

The High-NA Era: A Transition in Real-Time

The final months of 2025 and the start of 2026 have marked a pivotal shift from experimental testing to high-volume manufacturing (HVM) for ASML’s most advanced tool: the High-NA (0.55 Numerical Aperture) EUV machine. Priced at roughly $380 million per unit, these massive systems are the size of a double-decker bus and are essential for producing chips at the 2-nanometer (2nm) node and beyond. Intel (NASDAQ: INTC) has emerged as an early champion of this technology, having finalized acceptance testing for its first High-NA systems in late 2025 to support its "14A" node. This aggressive adoption is part of a multi-year effort to reclaim the manufacturing crown from rivals in East Asia.

The timeline leading to this moment has been defined by a complex dance of engineering and logistics. Throughout 2024 and 2025, ASML worked through a "transition year," clearing older inventory and readying its supply chain for the EXE:5000 and EXE:5200 series machines. Key players such as Taiwan Semiconductor Manufacturing Co. (NYSE: TSM) and Samsung Electronics (OTC: SSNLF) have since followed suit, with Samsung reportedly receiving its latest High-NA deliveries in early January 2026 to bolster its 2nm foundry capacity. The initial market reaction has been one of cautious optimism, as investors weigh the immense cost of these machines against the skyrocketing demand for the AI chips they produce.

Winners and Losers in the Equipment Arms Race

The ripples from ASML’s dominance are being felt across the entire US semicap landscape. Among the primary winners is Taiwan Semiconductor Manufacturing Co. (NYSE: TSM), which recently announced a staggering 2026 capex budget of $52 billion to $56 billion. This massive investment reinforces TSMC's position as the world's leading foundry and ensures it remains ASML's largest customer for the foreseeable future. Similarly, Applied Materials (NASDAQ: AMAT) and Lam Research (NASDAQ: LRCX) have seen their shares rally in early 2026. AMAT is benefiting from the industry’s shift toward "Gate-All-Around" (GAA) transistor architectures, while Lam Research is seeing "insatiable" demand for its etching tools used in the production of HBM4 (High Bandwidth Memory) for AI servers.

However, the landscape is not without its casualties. Companies heavily reliant on "lagging-edge" or mature-node capacity in China are facing a reckoning. As US and Dutch export controls have tightened, the revenue contribution from China for equipment makers has begun to "normalize." ASML itself expects its China revenue to drop from 36% in 2024 to approximately 20% by the end of 2026. Companies that failed to pivot their portfolios toward advanced AI packaging and sub-2nm nodes are finding themselves sidelined as capital is diverted toward the most sophisticated—and restricted—technologies.

Geopolitics and the "Silicon Shield"

The broader significance of ASML’s current position cannot be overstated. The company is now a central figure in a global geopolitical chess match. In December 2025, the Netherlands officially joined the US-led "Pax Silica" alliance, a strategic pact aimed at securing Western AI supply chains. This move effectively unified Dutch and US export policies, requiring ASML to navigate a more stringent licensing environment for even its mid-range Deep Ultraviolet (DUV) tools. This shift represents a transition from "de-risking" to a more formal "technological containment" strategy regarding advanced semiconductor manufacturing in restricted regions.

This event fits into a wider trend of "technological sovereignism," where nations are prioritizing domestic chip production to ensure national security. The historical precedent for this is the Cold War-era export controls, but the scale today is vastly different. The "Silicon Shield" that once protected global trade is being replaced by a more fragmented, alliance-based trade model. For competitors and partners alike, this means that the location of a factory is now just as important as the technology inside it. The regulatory landscape in 2026 is increasingly defined by these security-first alliances, which direct the flow of multi-billion-dollar equipment orders.

The Road Ahead: Hyper-NA and Beyond

Looking toward the remainder of 2026 and into 2027, the semiconductor industry is preparing for the next frontier of lithography. While High-NA is currently the focus, ASML has already begun briefing its most elite customers on "Hyper-NA" (0.75+ NA) research. This next generation of machines will likely be required for the turn of the decade, as the industry chases the 1nm limit. In the short term, the market will be watching for ASML’s Q4 2025 earnings report on January 28, 2026, which is expected to show net sales of approximately €32.5 billion for the full year.

Strategic pivots are already underway. ASML is increasingly focusing on the software and service aspect of its business, providing the metrology and computational lithography needed to optimize its hardware. The primary challenge for the company will be maintaining its gross margins—expected to settle around 52% in 2026—while scaling the production of its most expensive systems. If logic demand stays strong and memory makers like SK Hynix (KRX: 000660) continue their aggressive HBM4 roadmaps, ASML could see a projected surge in revenue through 2027 and 2028.

A Crucial Year for Investors

In summary, ASML’s role in 2026 is that of a "gatekeeper" for the next generation of computing. The company’s ability to successfully scale High-NA EUV while managing a volatile geopolitical environment has become the primary metric for the health of the entire tech sector. For investors, the takeaway is clear: the semiconductor market is no longer a monolith but a tiered ecosystem where advanced logic and AI memory are the only reliable growth engines.

Moving forward, the market should watch for any retaliatory trade measures from China and the pace of 2nm adoption among the big three—Intel, TSMC, and Samsung. As ASML’s market cap flirts with record highs, its performance will remain the single most influential factor in US semiconductor equipment sentiment. The "AI Infrastructure Supercycle" is well underway, and in 2026, all roads to the future still lead through Veldhoven.

This content is intended for informational purposes only and is not financial advice.