Nature's Sunshine has been treading water for the past six months, recording a small loss of 4.7% while holding steady at $20.81. The stock also fell short of the S&P 500’s 7.8% gain during that period.

Is now the time to buy Nature's Sunshine, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Nature's Sunshine Not Exciting?

We don’t have much confidence in Nature's Sunshine. Here are three reasons we avoid NATR, plus one stock we’d rather own.

1. Long-Term Revenue Growth Disappoints

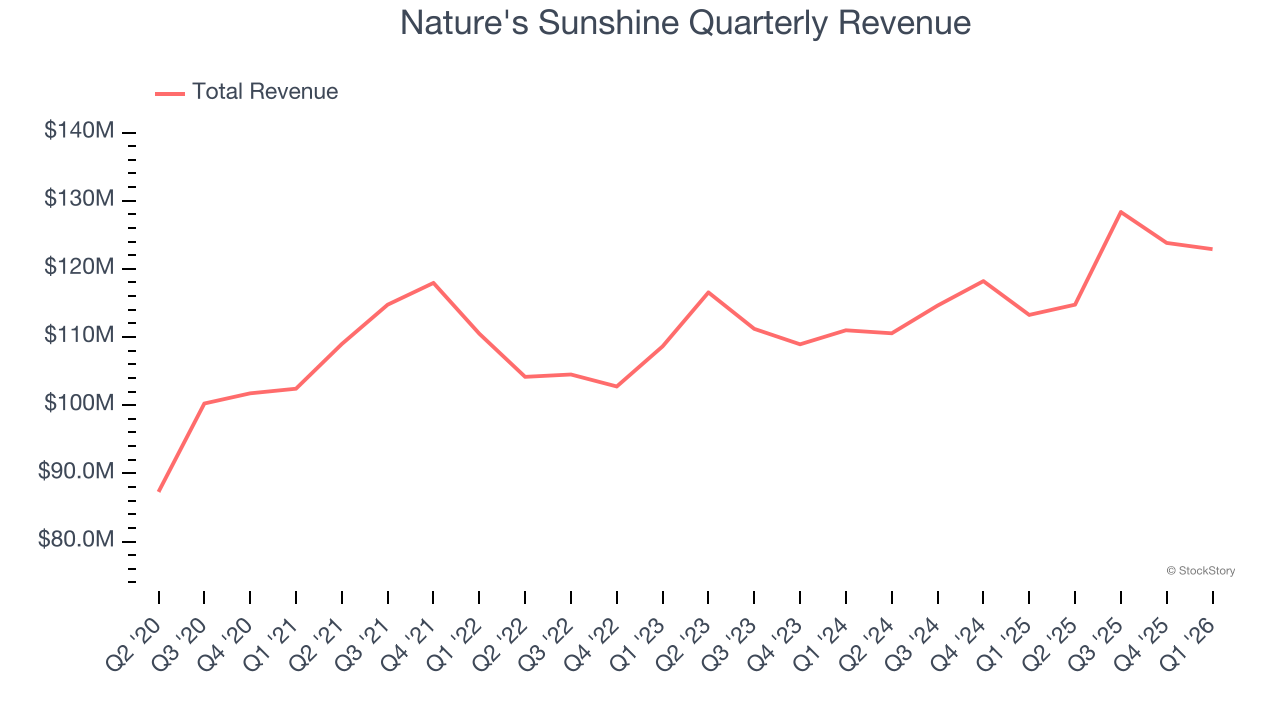

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Nature's Sunshine’s sales grew at a tepid 5.3% compounded annual growth rate over the last three years. This was below our standard for the consumer staples sector.

2. Fewer Distribution Channels Limit Its Ceiling

With $489.8 million in revenue over the past 12 months, Nature's Sunshine is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

3. Weak Operating Margin Could Cause Trouble

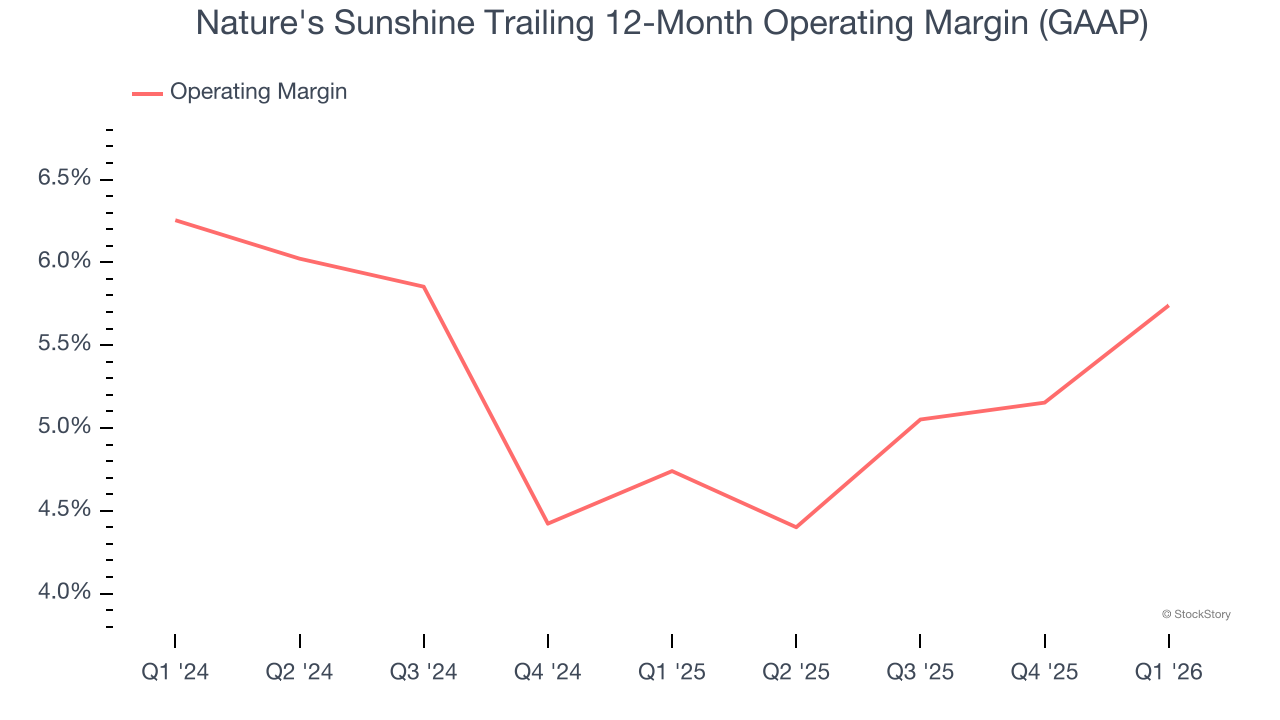

Operating margin is a key profitability metric because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

Nature's Sunshine was profitable over the last two years but held back by its large cost base. Its average operating margin of 5.3% was weak for a consumer staples business. This result is surprising given its high gross margin as a starting point.

Final Judgment

Nature's Sunshine isn’t a terrible business, but it doesn’t pass our quality test. With its shares trailing the market in recent months, the stock trades at 16.7× forward P/E (or $20.81 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We’re fairly confident there are better investments elsewhere. We’d recommend looking at an all-weather company that owns household favorite Taco Bell.

Stocks We Would Buy Instead of Nature's Sunshine

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.