Natural gas producer EQT (NYSE: EQT) will be reporting earnings this Tuesday after market hours. Here’s what to expect.

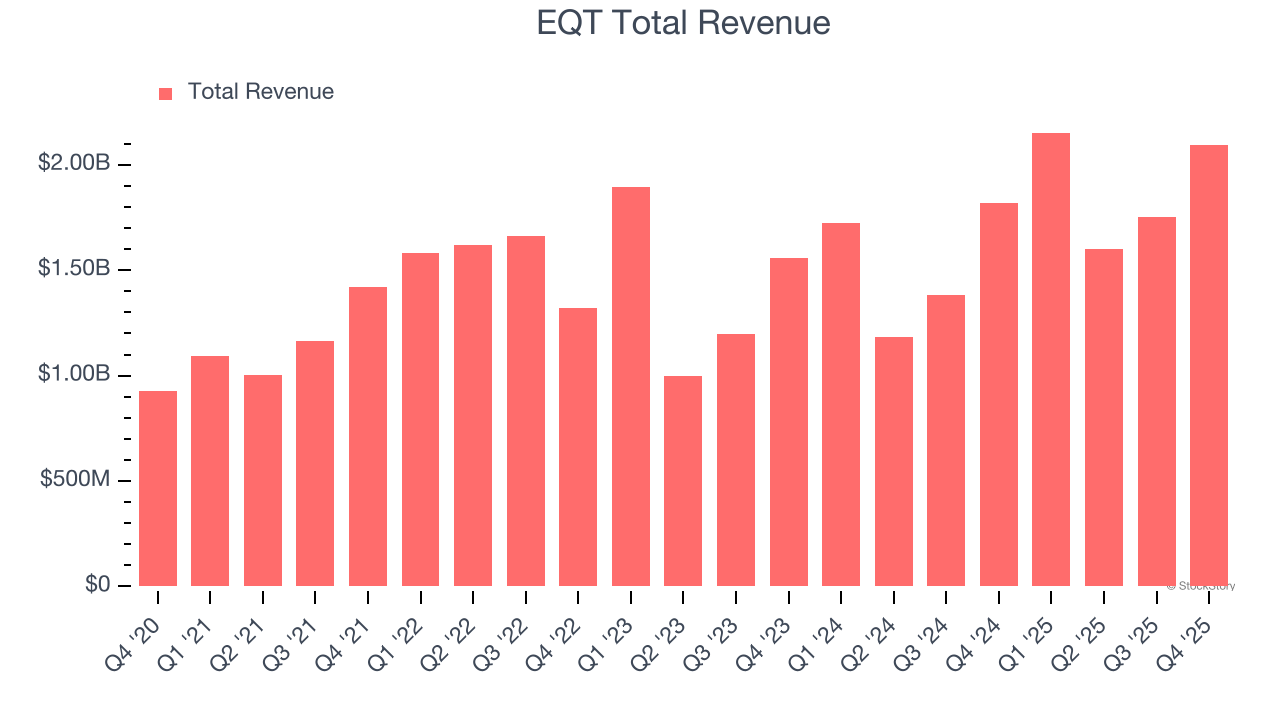

EQT missed analysts’ revenue expectations last quarter, reporting revenues of $2.09 billion, up 15% year on year. It was a strong quarter for the company, with a beat of analysts’ EPS and EBITDA estimates.

Is EQT a buy or sell going into earnings? Read our full analysis here, it’s free for active Edge members.

This quarter, the market is expecting EQT’s revenue to grow 49.6% year on year, improving from the 25% increase it recorded in the same quarter last year.

Heading into earnings, analysts covering the company have grown increasingly bullish with revenue estimates seeing in majority upward revisions over the last 30 days. EQT has missed Wall Street’s revenue estimates multiple times over the last two years.

With EQT being the first among its peers to report earnings this season, we don’t have anywhere else to look to get a hint at how this quarter will unravel for upstream & integrated stocks. However, the whole sector has been hit hard over the last month as stocks in EQT’s peer group are down 4.1% on average. EQT is down 10.1% during the same time .

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.