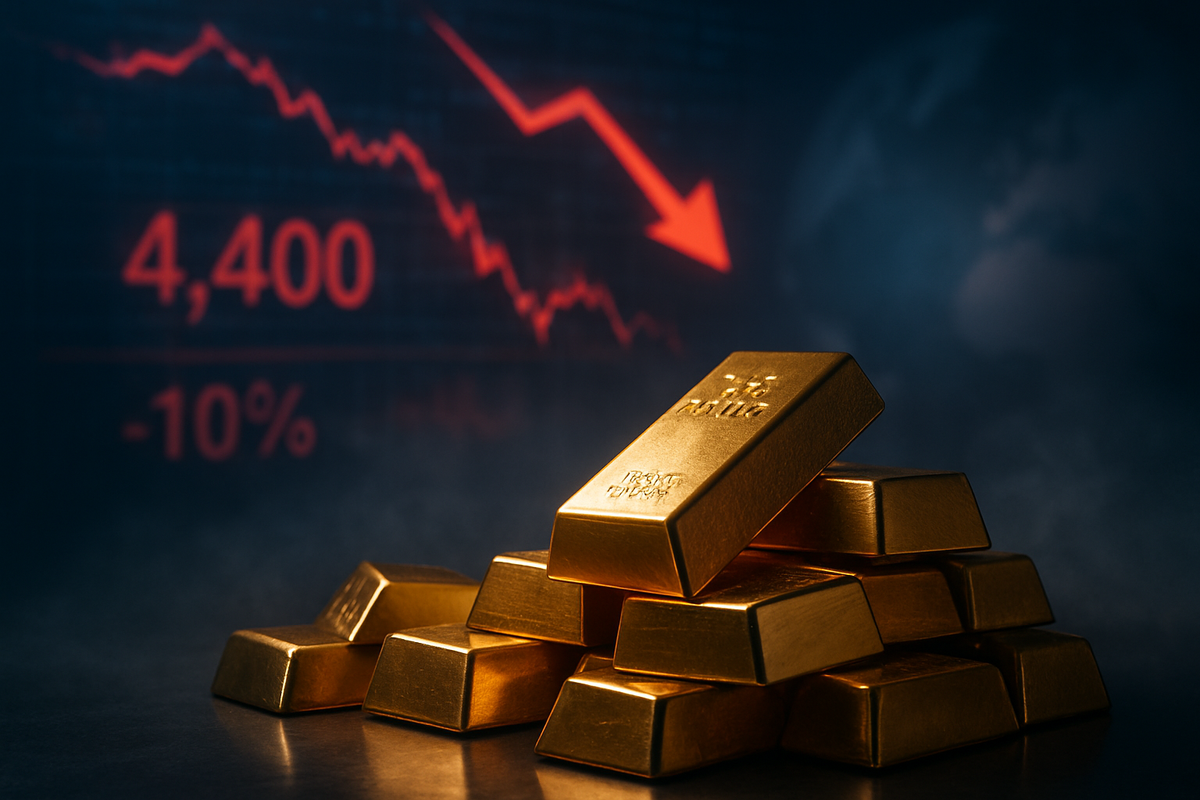

The gold market has been rocked by its most volatile week in over four decades, as the "safe-haven" trade that dominated 2025 suddenly evaporated. In a staggering reversal of fortune, gold prices plummeted more than 10% over the last five trading days, crashing through the critical psychological support of $4,400 per ounce. As of March 23, 2026, the precious metal is grappling with a dual-threat environment: a resurgent, hawkish Federal Reserve and a sudden de-escalation in Middle Eastern tensions that has stripped away the geopolitical risk premium.

This historic sell-off marks the worst weekly performance for gold since 1983, a period defined by the aggressive disinflationary policies of the Volcker era. For investors who viewed gold as an untouchable "store of value" during the recent surge toward $5,500, the current week has been a sobering reminder of the metal’s sensitivity to real interest rates and liquidity shifts. The $400-plus drop in a single week has triggered a cascade of margin calls, forcing institutional liquidations across the commodity complex.

The Perfect Storm: Hawkish Fed and Diplomatic Breakthroughs

The roots of this week’s carnage lie in the March Federal Open Market Committee (FOMC) meeting, which blindsided markets that had been pricing in a series of rate cuts for the latter half of 2026. Instead, the Fed maintained its benchmark rate at a restrictive 3.5%–3.75% range and signaled via an updated "dot plot" that higher rates are here to stay. Federal Reserve officials cited stubborn "oil-linked" inflation as a primary concern, suggesting that not only are rate cuts off the table, but a further hike may be necessary by autumn. This pivot sent "real yields" on U.S. Treasuries soaring, making non-yielding gold an increasingly expensive asset to hold in a portfolio.

Compounding the Fed’s hawkishness was a surprise diplomatic breakthrough in the Middle East. After months of heightened military tension that had pushed gold to record highs, reports of a comprehensive de-escalation framework and a tentative ceasefire between regional powers began to circulate early in the week. The sudden removal of this "war premium" led to an immediate exodus from safe-haven assets. By Wednesday, the sell-off had turned into a rout, with gold breaking below $4,800 and $4,600 in rapid succession before finally breaching the $4,400 level on Friday afternoon.

The speed of the decline was accelerated by technical selling. As the price fell, it triggered thousands of automated "stop-loss" orders held by hedge funds and retail traders alike. By the time the closing bell rang on March 23, the metal had recorded a weekly loss of approximately 10.8%, a figure not seen since the "Gold-for-Cash" crisis of the early 1980s. The psychological blow to the "store of value" thesis has been profound, as many younger investors who entered the market during the 2025 bull run are experiencing their first major commodity crash.

Winners and Losers: Mining Giants Face a New Reality

The immediate victims of the price collapse have been the major gold producers, who saw billions in market capitalization vanish overnight. Newmont Corporation (NYSE: NEM), the world’s largest gold miner, saw its shares tumble as investors recalibrated their earnings expectations for the coming fiscal year. While Newmont entered 2026 with a robust balance sheet and a massive $6 billion share repurchase program, the sheer velocity of the gold price drop has raised questions about the sustainability of its dividend at current levels. Similarly, Barrick Gold (NYSE: GOLD) faced intense selling pressure, despite its strategic pivot toward copper and its "Tier One" low-cost assets, which should theoretically provide a cushion against lower spot prices.

Exchange-traded funds were not spared either. The SPDR Gold Shares (NYSE Arca: GLD), the largest gold-backed ETF in the world, recorded its highest weekly outflow since its inception, as institutional "paper gold" holders rushed for the exits. This mass liquidation has had a secondary effect on royalty and streaming companies like Franco-Nevada Corporation (NYSE: FNV) and Wheaton Precious Metals (NYSE: WPM). Although these firms boast higher margins than traditional miners, their valuations are intrinsically tied to long-term gold price assumptions, which are currently being slashed across Wall Street.

Conversely, the U.S. Dollar and short-term Treasury bulls have emerged as the primary beneficiaries. The Invesco DB US Dollar Index Bullish Fund (NYSE Arca: UUP) surged as capital repatriated into the greenback, seeking the safety of yield rather than the safety of bullion. Banks and financial institutions that had been hedged against inflation may also see a reprieve, as the cooling of gold prices suggests a broader cooling of inflation expectations, potentially stabilizing the banking sector's net interest margins as the yield curve remains elevated.

A Crisis of Faith: The End of the 'Store of Value' Trade?

The significance of this week’s crash extends beyond simple price action; it represents a fundamental challenge to the "store of value" narrative that has underpinned the market for years. Throughout 2024 and 2025, gold was marketed as the ultimate hedge against a fracturing global order and central bank overreach. However, the current event demonstrates that when liquidity is prized above all else, even gold can be sold to cover losses in other asset classes. This mirrors the 1983 crash, where Middle Eastern producers dumped gold to raise cash amidst falling oil revenues, proving that gold often behaves as a liquidity source rather than a stable anchor during times of stress.

Furthermore, the "hawkish Fed" narrative suggests a return to traditional monetary orthodoxy. If the Federal Reserve is successful in maintaining high real rates without breaking the economy, the opportunity cost of holding gold remains prohibitively high. This fits into a broader industry trend where digital assets and high-yield credit are competing for the "inflation hedge" slot in institutional portfolios. The ripple effect may be felt in the central bank community, where the aggressive gold-buying spree of the last three years may now pause as emerging market banks reassess the volatility of their reserves.

Historically, periods of extreme gold volatility like this lead to a "washout" of speculative players. The 1983 precedent suggests that while the long-term upward trend of gold can remain intact, a multi-year consolidation phase is likely to follow. For policy-makers, the crash is a double-edged sword: it signals a reduction in immediate geopolitical risk and inflation panic, but it also warns of potential systemic stress if the rapid liquidation of such a massive asset class leads to broader market instability.

Looking Ahead: The Search for a Floor

In the short term, all eyes are on the $4,000 support level. Market analysts suggest that if gold fails to stabilize above $4,350 in the coming week, a test of the $4,000 mark is inevitable. Miners will likely need to engage in strategic pivots, perhaps deferring high-cost exploration projects and focusing on high-grade "sweet spots" to maintain profitability in a sub-$4,500 environment. Investors should also watch for a "dead cat bounce," as the oversold conditions may attract bargain hunters looking to play a temporary retracement.

The long-term outlook depends heavily on whether the Middle East de-escalation holds and whether the Fed follows through with its hawkish rhetoric. If inflation remains sticky despite the Fed's efforts, gold could find a bottom sooner than expected as the "real rate" argument softens. However, a new era of "Gold 2.0"—where the metal is treated more like a volatile commodity and less like a sovereign currency—appears to be emerging. Strategic adaptations will be required for both retail and institutional portfolios that had become over-indexed to the "permanent bull market" in gold.

Conclusion: A Turning Point for Commodities

The week ending March 23, 2026, will be remembered as the moment the golden bull finally stumbled. The 10% decline and the breach of $4,400 represent more than just a price correction; they signify a shift in the global macroeconomic regime. The combination of a disciplined Federal Reserve and a cooling geopolitical climate has removed the two strongest pillars supporting gold’s record-breaking run.

Moving forward, the market will likely see increased scrutiny of gold’s role as a portfolio diversifier. While the "store of value" trade isn't dead, its reputation has been severely tarnished by this 43-year outlier event. Investors should watch for the next round of FOMC minutes and any signs of renewed friction in global trade or diplomacy, as these will be the only catalysts capable of restoring gold's lost luster. For now, the "Golden Age" has given way to an era of high-yield reality.

This content is intended for informational purposes only and is not financial advice.