“I've been around for a long time in investing – 40 years now,” explained Barchart’s senior technical strategist on our call. “I usually make the joke that I've been around the block a few times and I know where all the good parking is.”

John Rowland, CMT, doesn’t want to be negative about artificial intelligence (AI). But right now, he can see more than a few parallels with our current Great AI Land Race of the 2020s and the Tech 1.0-era broadband boom.

“You had this rush to build out broadband, and they were laying fiber optic cables everywhere,” recalled Rowland. “But in reality, the demand was only maybe five percent of all the supply that was out there.”

And as we all know, regardless of investing experience, none of the good parking is ever parallel.

“So I’m not saying that AI is not going to disrupt our lives and make our lives different – I'm just saying that demand might not be there in the beginning relative to the supply being built out. And there’s going to be winners and losers.”

Exclusive to our Barchart audience, here are the winners, the losers, and the hidden narratives of the AI data center race that investors should be watching – starting from the Big 4 hyperscalers all the way across the supply chain, from natural gas to nuclear power to jet fuel, with a focus on the investment opportunities that matter the most right now.

For more exclusive content from this interview with John Rowland – including NIMBY pushback against Big Tech, data centers in space, and the SpaceX IPO – head over to our official Barchart Substack >>

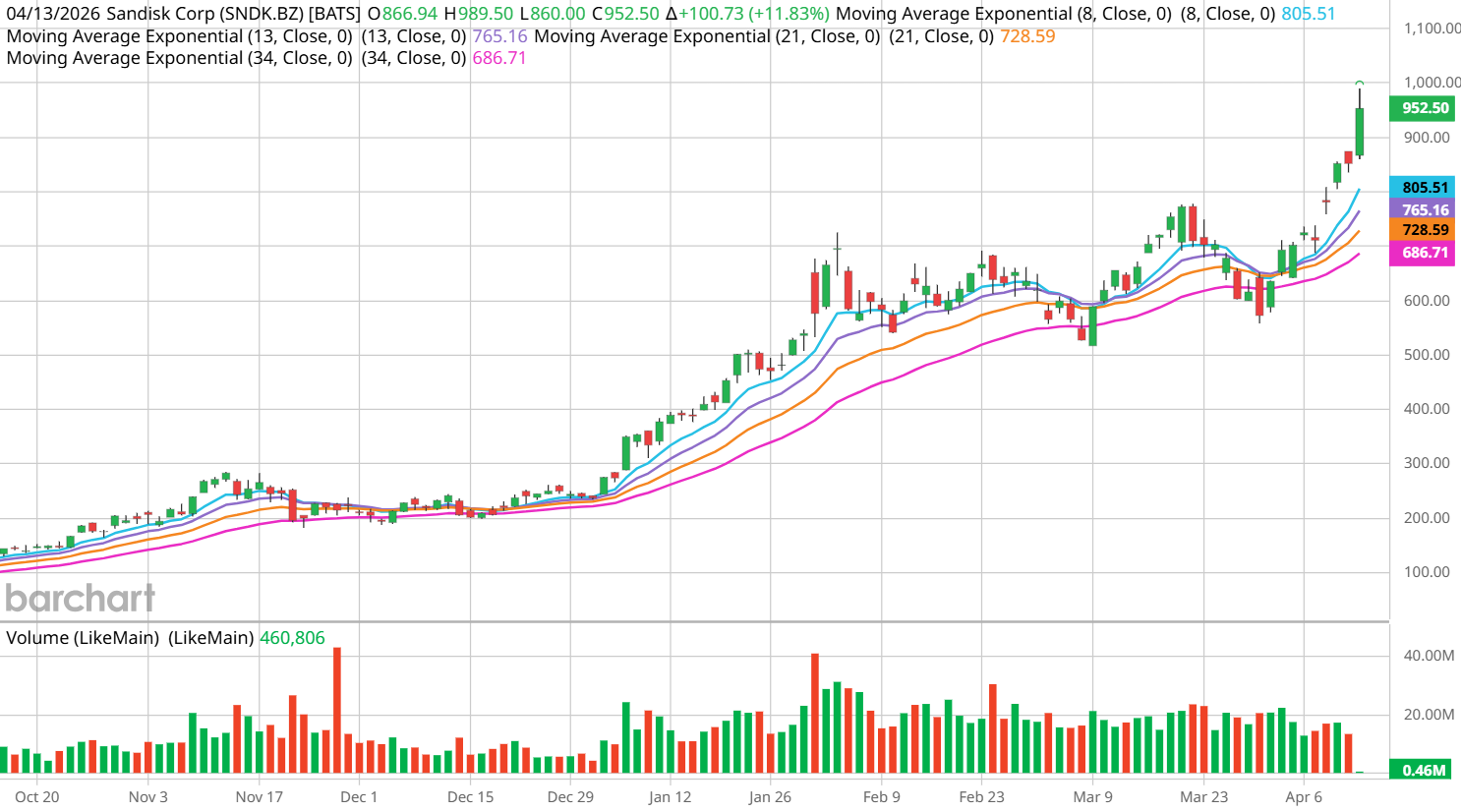

Remember Sandisk?

If I were in the whimsical kind of mood to run an AI prompt on my work inbox, I might ask it to create a word cloud of the topics I most often email about with my colleague here at Barchart, our Market on Close host John Rowland.

Data centers, it would probably tell me in massive bold letters right in the middle, with the other big ideas including themes like nuclear power, battery storage, and natural gas. (Imagine me drinking a tremendous amount of water while I type this paragraph, as the meme goes, and I’m practically Gemini.)

That’s just simple pattern recognition, though. Over the past nine months or so, John and I have collaborated on so many shorter pieces for Barchart around these investing themes that we ultimately published this longer article back in January, tying together some of our favorite ideas around AI data centers, energy generation, and battery storage.

Mission accomplished, I thought, hanging up the banner as I hit “Publish.” But less than three months later, this niche of the market is moving so quickly that our analysis is already in need of a refresh.

Since then, we’ve had news that NIMBY-minded New Englanders in Maine are set to enact the first statewide ban on data centers. Elsewhere, Google is partnering on AI data center power with a Texas gas plant that emits more carbon dioxide each year than the city of San Francisco. And Oracle issued a press release touting its new CFO’s bona fides from industrials like Schneider Electric and AES, where she gained experience in “complex, capital-intensive infrastructure investments.”

Of course, circling back to that utter lack of whimsy, it’s important to point out that a war has also started since we last addressed this subject. That’s had no small impact on the energy prices and supply chains driving this AI data center narrative.

While the U.S. has remained somewhat insulated, as we’ll discuss, global markets are feeling the crunch. To that point, students of history will no doubt recognize the strength of “fed up” as a statement by a sitting prime minister, suggesting that the recent flare-up in energy prices has strained an otherwise fairly special post-war relationship.

Indeed, OpenAI on April 9 said it would pause plans for the Stargate UK data center first revealed last September, telling Bloomberg News the project “will move forward when the right conditions such as regulation and the cost of energy enable long-term infrastructure investment.”

And then there’s Sandisk (SNDK).

“The theory behind the investment aspect of it is that you have this still pond, and then you throw this giant rock in the middle of the pond, and it creates these ripples. And as each one of these ripples rolls out through the pond, those are all of the different types of investment opportunities,” said John.

“Think about it – it all started with chips, right? And then it rippled out to hardware and infrastructure and the hyperscalers and the models that they’re gonna use and then the applications. And then there’s the demand for power behind the meter, and maybe some of the hidden opportunities, the hidden alphas.

“I think you look at a company like Sandisk – I mean, I don’t know if you remember Sandisk; it was just those little, you know, USB sticks that you use, right? Now it’s a $700 company, right?”

He was right; it was a $700 company when he said that. And then Nasdaq announced that SNDK would be joining its benchmark Nasdaq-100 Index, and suddenly it was a $900 stock just days later.

I wasn’t sure if I could write this draft fast enough.

“What Changed is That They Spent the Money.”

Surely by now you’ve met the Magnificent 7. But like the classic rectangle/square subset relationship – while all of the Big 4 hyperscalers are Mag 7, not all of the Mag 7 are Big 4 hyperscalers.

The “Big 4,” for our purposes, are Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOG) (GOOGL), and Meta (META). When we talk about AI hyperscalers, we refer to these Big Tech giants that have the resources, motivation, and cash on hand – or borrowing ability – to build out physical data centers for artificial intelligence (AI) training and compute at scale.

This year, Amazon plans about $200 billion in spending. Meta forecasts up to $135 billion, and Google is budgeting up to $185 billion. Microsoft looks modest at around $120 billion in planned spending for 2026, and CNBC pegs the combined plan spend at $700 billion for this fiscal year.

Another key up-and-coming player in the AI hyperscaler game is legacy software company Oracle (ORCL), although it has yet to unseat iCloud titan Apple (AAPL) in the unofficial “Big 5.” (Apple, for its part, is not on any particular data center spending spree, and is busy trying to make sure you can fold your iPhone in half.) Oracle, which has been cutting jobs for months to free up cash flow, announced plans earlier this year to raise $50 billion in capital to support its data center dreams.

Elizabeth Volk: So there’s kind of a land race right now to get these AI data centers approved and built. And there's obviously a ton of capital expenditure (CapEx) involved in that.

But do all of them have the same ability to fund that spending? Or are there some hyperscalers that have an edge in terms of the stability of their core business model and cash flows, when you think about Google versus Meta versus Oracle?

John Rowland: Well, when we came into this cycle, the hyperscalers initially were all cash-rich. The Googles and the Amazons of the world – they were cash-rich, and they were heavy asset-poor.

And what dynamically has changed in a very short period of time is that they had the money to spend, they spent it, and now maybe they might be cash-poor and heavy asset-rich.

That means hyperscalers have had to go out and raise capital, explained Rowland, which means they now have to justify a funding gap to investors – from spending to revenue all the way down to shareholder benefit.

EV: And Meta just extended their CoreWeave deal for another $21 billion today.

JR: They're spending like drunken sailors, right. It's insane.

It’s this kind of “spend first, ask questions later” accounting that captured the attention of one Dr. Michael “Big Short” Burry. Last November, Burry famously called out the AI data center economy for what he described as circular dealmaking, and questionable loans that seemed to outlive the usefulness of the chips they were financing.

While Rowland doesn’t throw around the word “fraud,” he’s open to the idea that valuations are elevated.

JR: Is there some type of circular financing where everybody's just raising the valuations of their companies based on, “hey, I'll buy from you, you buy from me, and then I'll buy from this guy”? I would think there is some aspect of that to it.

But the question I have when I look at the valuation of some of these companies is – if we are in this AI race, is there a finish line? Because it seems like the goalposts keep moving.

Even if there is a finish line, there might be bad news for the oldest players in the race:

“When you have a disruptor technology, usually the first disruptor is not the one that succeeds,” John pointed out. “Typically, their competitors learn from their mistakes and they're a little bit more nimble and able to adjust to changing market conditions.”

In particular, Rowland says that Meta – following its recent court losses over social media addiction – looks most vulnerable of the Big 4 to data center cash bleed, not to mention bad PR blowback.

Whereas a company like Google, he noted, is basically a monopoly, and generates revenue through multiple different streams. Previously, Rowland has compared Alphabet’s model to the “Big Oil” of AI.

Conversely, as the company’s debt-to-equity ratio was soaring last December, Rowland highlighted 3 high-yield pipeline picks to play the power generation side of Oracle’s data center growth.

All of which is a wonderfully suitable transition into the energy portion of our conversation.

All Gas, No Brakes

Natural gas is hardly a newcomer to the AI data center story. Rowland, a veteran of the commodities world himself, notes that natgas is among the “cheapest, effective, and most reliable” power sources.

But the current Big 4 race – for land, for specialized AI chips, for power, and for grid access – means that speed to market is now the greatest advantage natural gas can offer a hyperscaler.

Rather than getting hooked up to a PJM- or ERCOT-regulated grid when capacity permits – in, say, 2029 – hyperscalers want that “competitive currency” of speed, explained John: “Without that, the data centers are dead in the water.”

But “the grid” is not just a social construct; it’s a very real and physical piece of aging infrastructure with limits on its capacity. So when a small army of Silicon Valley hyperscalers descended on PJM demanding access, it shook up the industry. (Also, quite possibly, your utility bills.)

The solution? Bring your own power. As we reported for Barchart in November:

As more and more data centers are looking to come online, four governors recently proposed a unique plan to ease the strain on PJM Interconnection – the largest U.S. power grid, and one that’s currently serving large data center-density states. The proposal, backed by Pennsylvania, Maryland, New Jersey and Virginia, suggests fast-tracking data center approval for candidates who can generate their own power and add it to the grid.

And so natural gas, once optimistically described as the “bridge” in the global transition from fossil fuels to clean energy, has transitioned itself – from bridge fuel to ultimate destination for many hyperscalers.

This, Rowland explained, becomes another “ripple” in the AI data center pond.

JR: Hyperscalers wanted to be hooked up tomorrow, right? So the “bring your own power” initiative created another derivative trade, which was: OK, let's build our own power plants. And what’s the most reliable way to do that? Well, gas turbines. And that has been reflected in multiple companies.

The one that you and I touted months ago was GE Vernova, and you’ve also got Siemens, Mitsubishi, Hitachi – and it's not only the gas turbines, but it's the capacitors that connect to the grid, and the mechanics and hardware.

So that's kind of where we're at now, is where are we going to get our power? Data centers are useless without power. So that becomes the number one priority – not chips or servers or hardware. It's power.

“...the conventional model of relying on grid power is facing challenges in terms of long lines to get a permit to connect to the grid,” agrees the page on GE Vernova’s website touting its gas turbines. “That’s why many data centers are considering islanded operations with gas turbines to get their power needs in a timely manner and to avoid the wait times that could impact their Time To Revenue (TTR).”

EV: With the Iran war now, we've seen energy prices get insanely volatile. And then OpenAI is actually halting the UK Stargate project, with energy prices being cited as one of the drivers.

Does this kind of macro backdrop impact the ability of hyperscalers to keep building out data centers at pace, or are they going to have to change their calculus in terms of capex?

JR: Well, I think there's two dynamics we have to think about. What is happening in the Strait of Hormuz will have minimal impact on the natural gas market here in the U.S. Now, our natural gas market is tied to global markets through LNG, liquefied natural gas. And with the supply disruption in Qatar to their production, yes, that might have a slight impact.

But certainly supply chain issues around the world could have an effect on data center buildouts.

EV: We did see some volatility in semiconductor stocks related to the initial strait closure. So do you see that as being an issue? Because we don't really have our own domestic version of Taiwan Semiconductor here in the U.S.

JR: This is a little outside my expertise, but there’s helium used in the process of making chips that comes out of the Gulf. So that might now affect the data center supply chain.

In fact, a new note this week from Pavilion Global reports that about one-third of the world’s helium supply is currently out of the market, thanks to the Iran war. Supplies in Qatar could take up to five years to bring back online, due to the infrastructure damage incurred.

Oil, though, is primarily a transport fuel – and Rowland called out the timeline for shipping and refining crude into products like jet fuel, as the chokehold on tanker traffic through the strait is already causing a steep drawdown in supplies.

“The last cargo of European jet fuel to pass through the strait of Hormuz before the war began is due to arrive in Copenhagen” as of last Saturday, per The Guardian, and that leaves European airlines with just a few weeks of runway (sorry) before they’re out of fuel.

“If the situation with jet fuel becomes critical, that could have a ripple effect through all supply chains,” warned Rowland.

Overall, this paints a long-term bull case for natural gas, according to John. In his view, there is going to be a time “where it becomes obvious that demand is outpacing supply for natural gas” – but how should retail traders invest in the so-called “widow maker” of commodities?

Natural gas futures can be volatile and risky for the uninitiated – and for that matter, even the initiated – and Rowland warns that even tracking products like the US Natural Gas Fund (UNG) offer barriers to entry for market rookies:

“You have to understand how the ETFs are designed, when the underlying futures contracts are set to roll, that the underlying contracts might not reflect the spot price, and so on,” he explained.

Instead, retail traders can dodge some of the commodity’s day-to-day volatility with once-removed natural gas stocks like Cheniere (LNG), EQT (EQT), Coterra (CTRA), and Devon (DVN), the last of which is one that John owns as of this writing.

Investing in these natgas stocks, he told me, is a way to participate in the commodity’s price increase as it falls directly to the company’s bottom line.

And for those who fear that surging demand for old-school energy dug out of the earth will send us spiraling ever further from our climate goals, don’t worry. The economics of Big Tech’s insatiable appetite for natgas, John told me, will eventually force the hyperscalers back toward clean energy.

Were We Early to the Renaissance?

You probably heard the big news when Microsoft announced it was going to partner with Constellation Energy (CEG) to restart the notorious Three Mile Island nuclear reactor. It was the emblematic headline of what we all (myself included) described as a “nuclear renaissance,” with multiple hyperscalers signing power purchase agreements to help fuel what they envisioned as a new era of fusion-driven AI.

You probably heard much less about the various regulatory snags the Three Mile Island project has run into since that big “grand reopening” announcement. Most recently, CEG stock slipped on reports that the equally notorious PJM may not be able to connect the site to the grid until 2031, which is a pretty significant whiff on Constellation’s target date of 2027.

Rowland says the market may have gotten ahead of itself when it comes to “perception versus reality” on nuclear stocks.

JR: I think what we had is too many companies with no track record of success promoting these unproven nuclear technologies, like small modular reactors (SMRs). And the reality – again, market perception versus reality – is that even at best, you have nuclear regulations, you’ve got NIMBYs to worry about, you have an unproven technology.

Even relative success stories like Oklo (OKLO), John added, are still in the development phase. “The fact remains that they've never really built one of these machines or that their technology might not work.”

JR: If you're going to look at nuclear, you have to look at proven providers. Again, one of the companies that you and I have talked about in the past is GE Vernova. Not only are they in the natural gas turbine space, but they're also in the nuclear space.

They’re partnered with Hitachi to build these SMRs, and they have one currently under construction that's going to come online relatively soon. I think it's in Canada, and they're building another one in Tennessee. And they have the blessings not only of the utility regulator, but also of the Department of Energy and the Department of Defense.

Because if you're going to look in the nuclear space – and I'm not completely discounting the small companies that are just coming online – I think it's more important to look at those that have been proven. And there's a lot of regulatory landmines that they need to navigate. So that's why I like companies that have already built nuclear reactors and also understand the federal regulations.

EV: Do you think there's less upside potential for these nuclear and solar names now that hyperscalers are shifting toward natural gas for speed and reliability? Or do you think it's just more of a long-term story?

JR: I think it's a combination of both. First, due to that heavy demand for natural gas and then for gas generators, they’re now telling folks, “Hey, if you want a gas turbine, you're probably looking at 2029, 2030,” right?

So given the urgency to create this “behind the meter” power supply, then you have to look for alternatives. And if the costs get too high for the more dependable stuff like natural gas, then that makes alternatives like solar and nuclear more viable.

Now nuclear, as we’ve discussed, is a different narrative, but solar – the EIA just came out with a report that said in the last year, over 50% of the new power generation that was added to the grid came from solar. So I don't think that solar is lagging behind, and it’s actually moving forward at a very rapid pace because it's becoming cheap.

Along with battery storage, John believes that solar power is a critical component of the energy supply story for AI data centers, and says there’s “a lot of alpha” in both areas.

He called out First Solar (FSLR) during our conversation for its integrated business model, from silicon wafer to installation, and then picked up the stock days later on a TTM Squeeze signal.

As for the battery side of the trade, Rowland is currently evaluating private and international companies to find a new favorite.

“Battery storage has to evolve in order for AI data centers to get to where they want to be,” he told me.

Finding the Opportunity in Data Center Sprawl

There’s already been a lot of money made on this investing theme, and Rowland fondly recalls putting together the Power & Electricity Infrastructure Watchlist for a Barchart webinar not too long ago.

Names like Mastec (MTZ), Powell Industries (POWL), and Quanta Services (PWR) have exploded in value since then, “because of this amount of money that is chasing this data center buildout,” he said. “If I could have launched this as an ETF…”

As for current opportunities, the balance sheet inversion Rowland mentioned at the beginning of our conversation – AI hyperscalers moving from cash-rich to asset-heavy – is a striking transition, and it’s one that caught the eye of Bloomberg columnist Matt Levine recently too, vis a vis the upcoming SpaceX IPO:

If you had told me in 2016 “my company will build rockets and send them to Mars in order to generate free cash flow to subsidize a capital-intensive money-losing website that will use machine learning algorithms to answer people’s questions,” I would have been like: No no no, the other way.

But it’s true that our robot overlords are unlikely to arrive in hologram form, at least in this first generation. Or as John Rowland once told me, “Robots and rockets aren’t made from hopes and wishes,” which I then used to title his article.

“The whole gamut of aluminum, titanium, copper, rare earths – I don’t think that story’s going away, though it might shift week to week,” said John.

For example, Rowland noted that aluminum in particular has come to the forefront lately amid Iran-related smelter damage and supply snags, but the aluminum story more broadly is not new to his radar.

“These base metals that are used in the development of data centers, rocket ships, satellites – that story is not going away,” said Rowland. “That is a mega-trend commodity story that will play out for another 10-15 years.”

He particularly likes Alcoa (AA) and Freeport-McMoRan (FCX), and owns both. Shortly after our call, Alcoa was upgraded to “Overweight” at Morgan Stanley, which cited a tight physical market, higher pricing, and supply disruptions for the bullish note.

EV: Where are the “hidden trades” in this AI data center narrative?

JR: Water [FIW] hasn’t really been addressed, but will come more to the forefront. And carbon capturing is going to come to the forefront soon.

Geothermal is rapidly advancing, and gathering a foothold with financing. I think it offers the best of all worlds: renewable, scalable, and zero-carbon. One I’ve mentioned before is Fervo Energy, which is still private, but they’ll be bringing an IPO sometime this year.

Fervo is actually partnered with Google already – and Google wants to get to carbon neutral, by the way. And geothermal is nice, but if they're simultaneously building this power station that’s billowing up CO2 at the same rate as San Francisco, how do they get to carbon neutral?

So maybe the next trade includes companies that do carbon capture or smokestack scrubbing, like Chart Industries (GTLS) or Occidental (OXY).

EV: And finally, we’ve been talking about AI data centers for, I think, years now. Which other stock market stories or investing opportunities is this currently drowning out that investors might be missing?

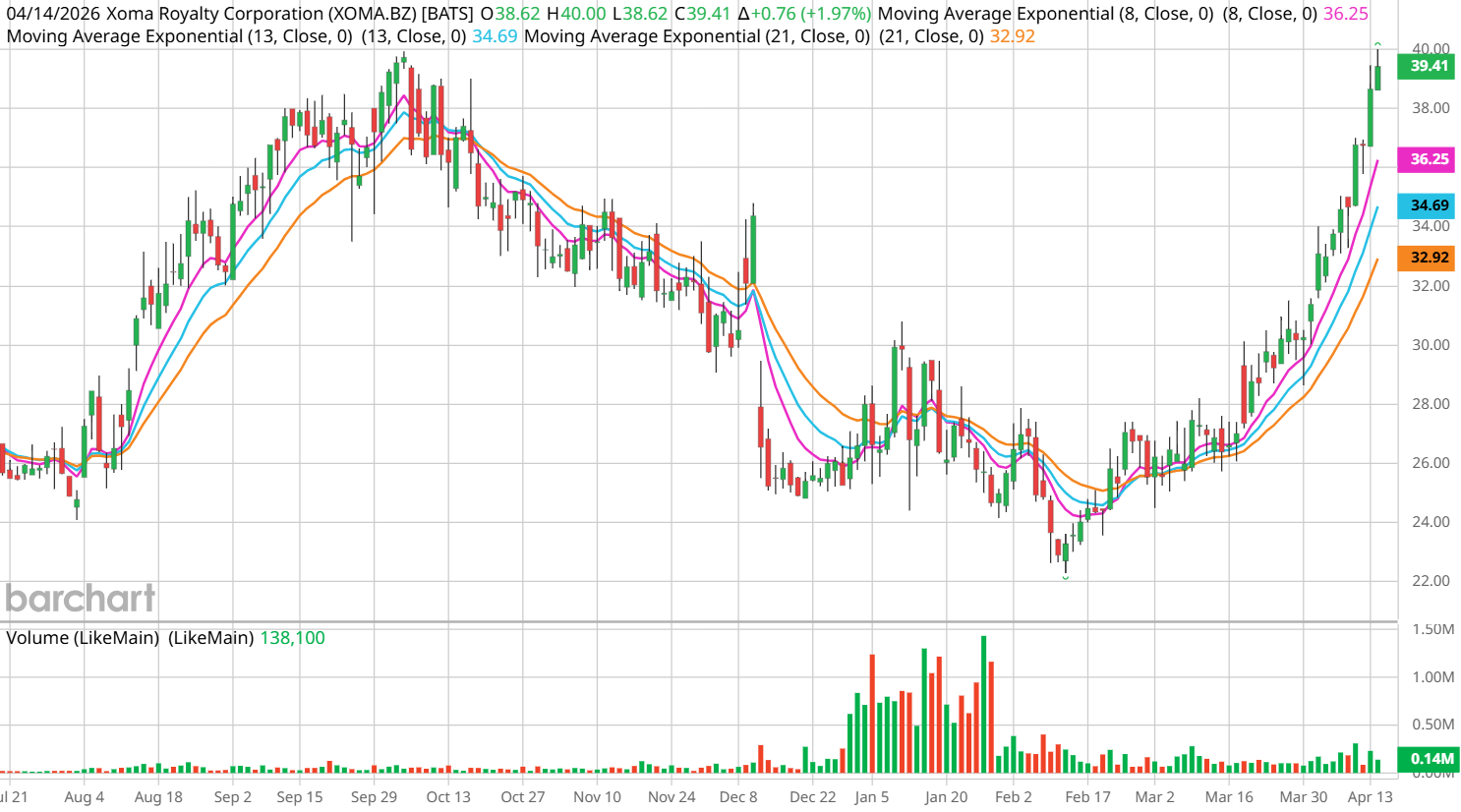

JR: AI biotech is another area I would be looking at. The percentage of new drugs that are going into clinical phasing, a high percentage of them are due to AI.

He called out XOMA Royalty (XOMA), which is a company that he warns requires plenty of due diligence. Rowland uncovered this one using Barchart screeners, and told me it might be interesting over the long haul, for traders who can navigate a little short-term FOMO (John would be looking for about a 10% pullback from the current rip higher).

Before we wrap this up, one final thought from John Rowland, and it’s on the topic of Meta stealing Google’s advertising crown.

With more of the internet’s advertising dollars flowing away from Google search and through Meta’s AI-tailored social media algorithms, John emailed to pose the idea that perhaps the hyperscaler race was, for lack of a better term, simply a Ricky Bobby situation:

“If you’re not first, you’re last.”

This interview has been edited for clarity. For more from John Rowland, CMT, sign up to be notified when Market on Close goes live. To stay in touch with Elizabeth Volk, subscribe to the Barchart Brief.

On the date of publication, Elizabeth H. Volk did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart