Pangaea has been treading water for the past six months, recording a small return of 1.7% while holding steady at $7.31. The stock also fell short of the S&P 500’s 11% gain during that period.

Is now the time to buy Pangaea, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Pangaea Not Exciting?

We don’t have much confidence in Pangaea. Here are three reasons we avoid PANL, plus one stock we’d rather own.

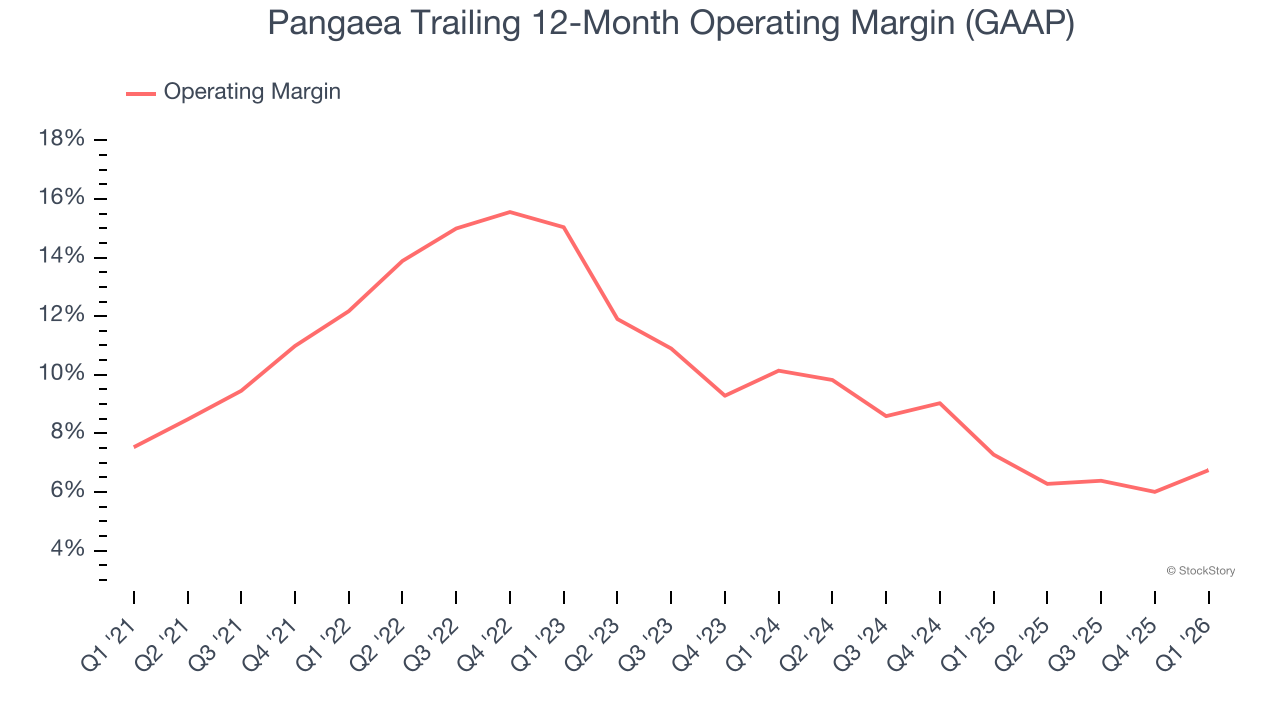

1. Shrinking Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses — everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Looking at the trend in its profitability, Pangaea’s operating margin decreased by 5.4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 6.7%.

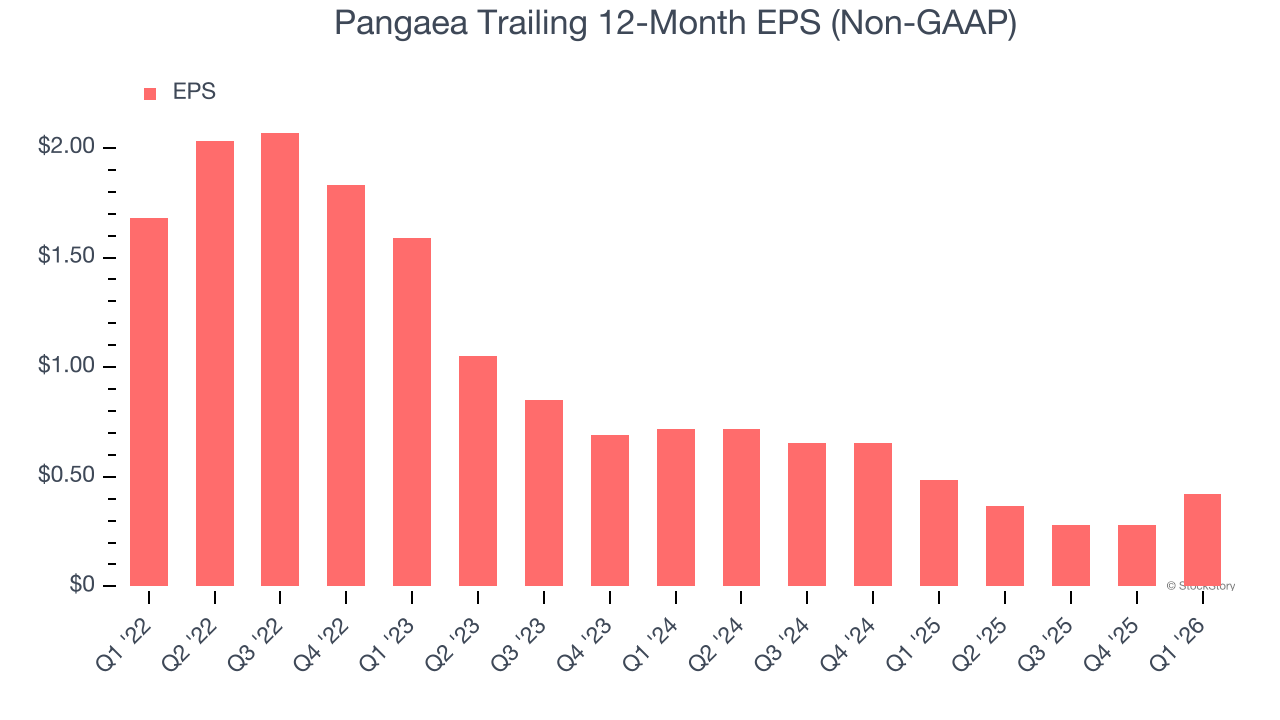

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Pangaea’s full-year EPS dropped 179%, or 29.3% annually, over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Pangaea’s low margin of safety could leave its stock price susceptible to large downswings.

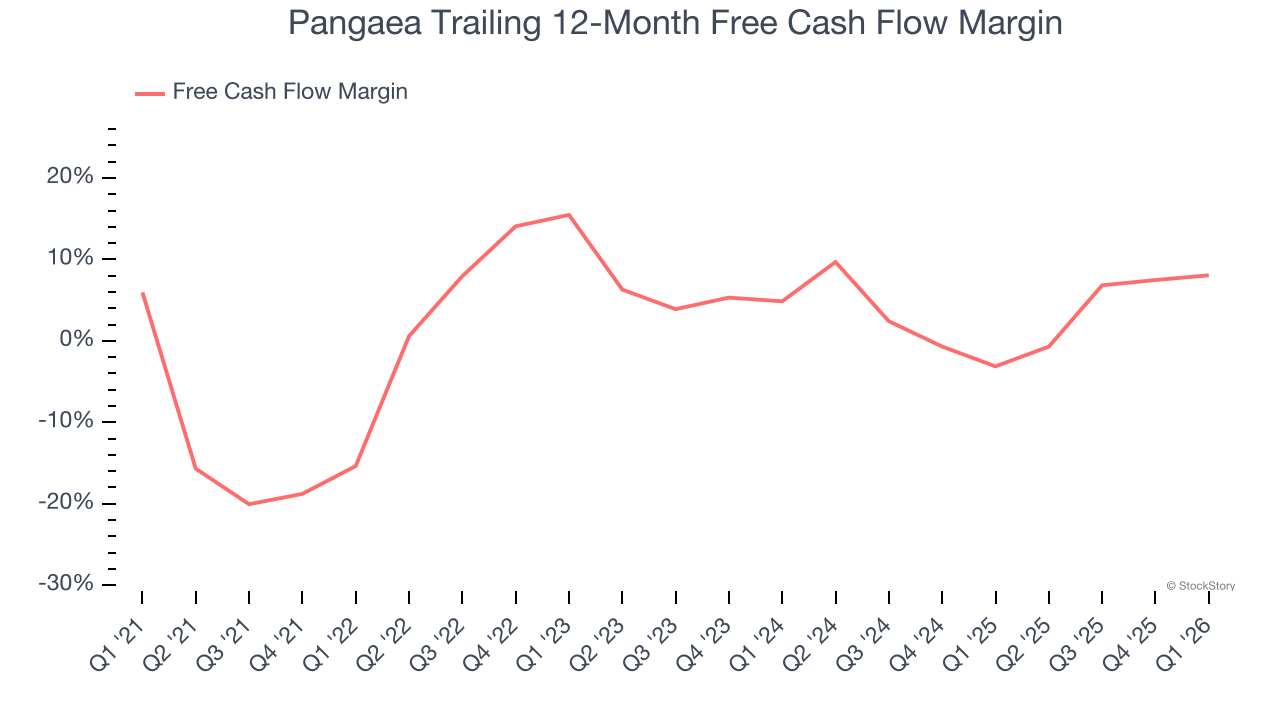

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Pangaea has shown poor cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.2%, below what we’d expect for an industrials business. The divergence from its good operating margin stems from its capital-intensive business model, which requires Pangaea to make large cash investments in working capital and capital expenditures.

Final Judgment

Pangaea’s business quality ultimately falls short of our standards. With its shares underperforming the market lately, the stock trades at $7.31 per share (or a trailing 12-month price-to-sales ratio of 0.8×). The market typically values companies like Pangaea based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. Let us point you toward the most entrenched endpoint security platform on the market.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.