Over the past six months, TFS Financial has been a great trade, beating the S&P 500 by 24.8%. Its stock price has climbed to $17.54, representing a healthy 31% increase. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in TFS Financial, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think TFS Financial Will Underperform?

We’re happy investors have made money, but we don’t have much confidence in TFS Financial. Here are three reasons why TFSL doesn’t excite us, plus one stock we’d rather own.

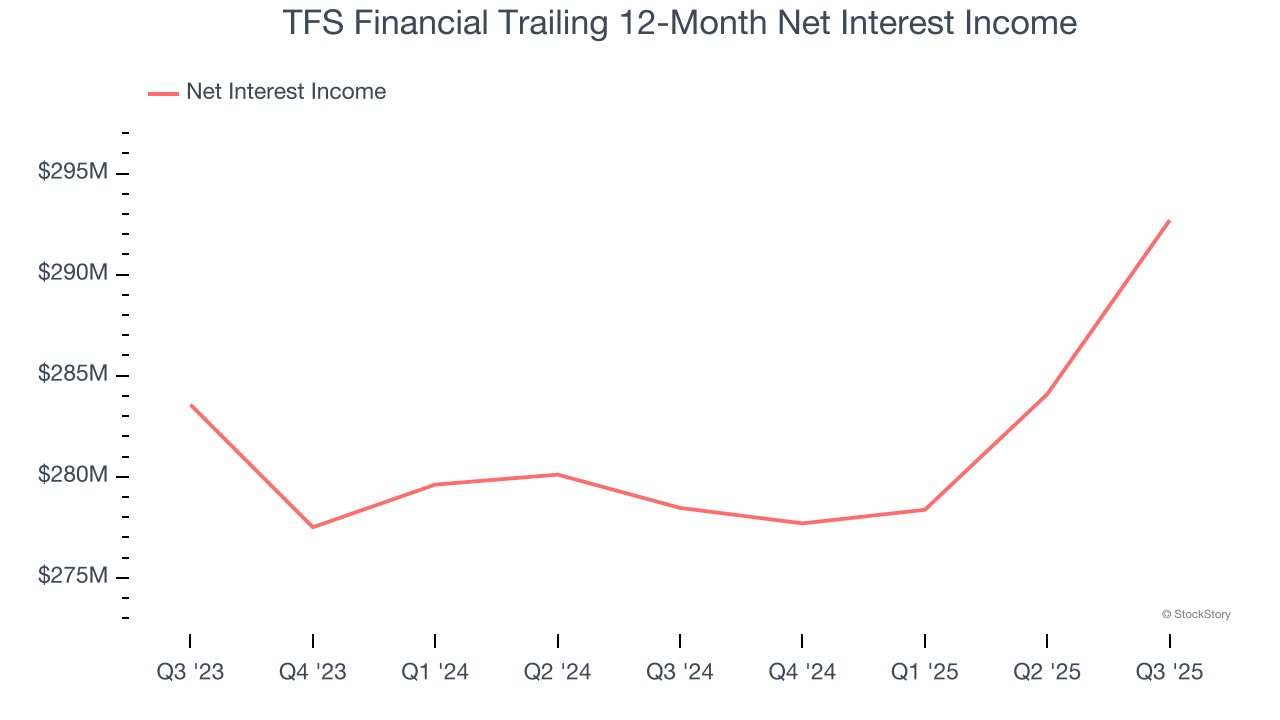

1. Net Interest Income Points to Soft Demand

While banks generate revenue from multiple sources, investors view net interest income as a cornerstone — its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

TFS Financial’s net interest income has grown at a 3.9% annualized rate over the last five years, much worse than the broader banking industry. This was driven by its loan growth as its net interest margin, which represents how much a bank earns in relation to its outstanding loan book, declined throughout that period.

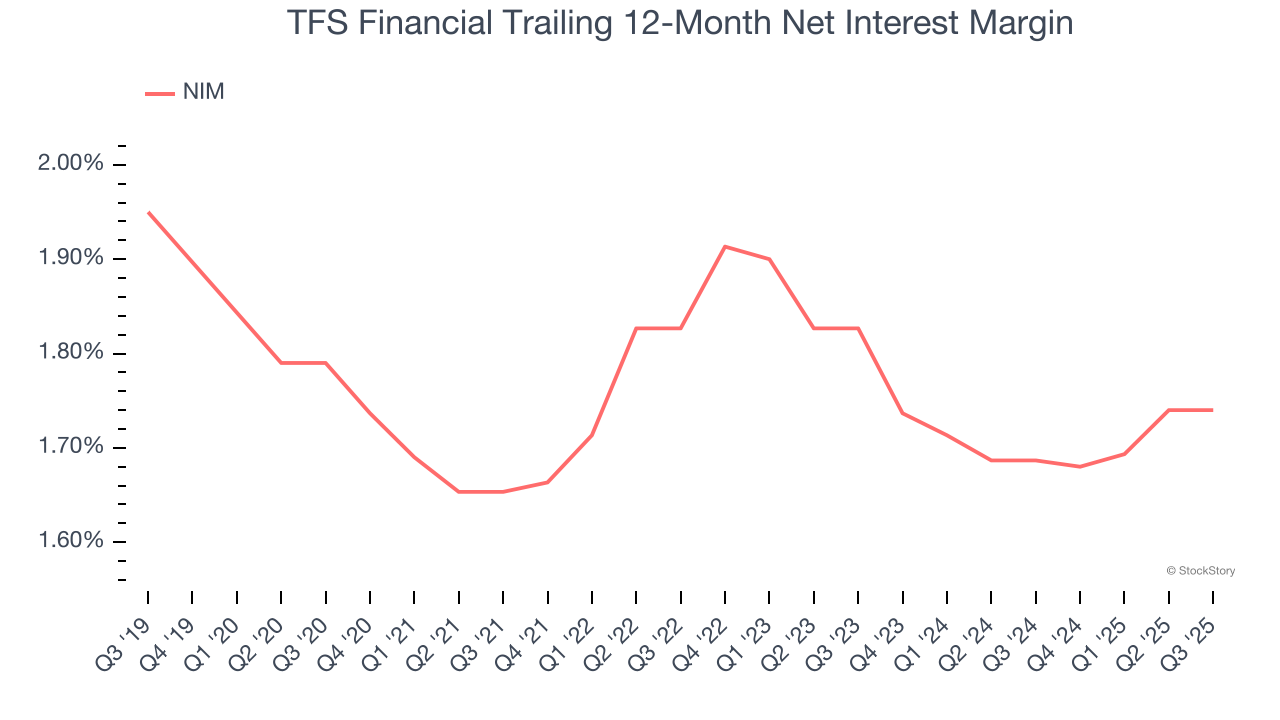

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It’s one of the most important metrics to track because it shows how a bank’s loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, we can see that TFS Financial’s net interest margin averaged a poor 1.7%, indicating the company has weak loan book economics.

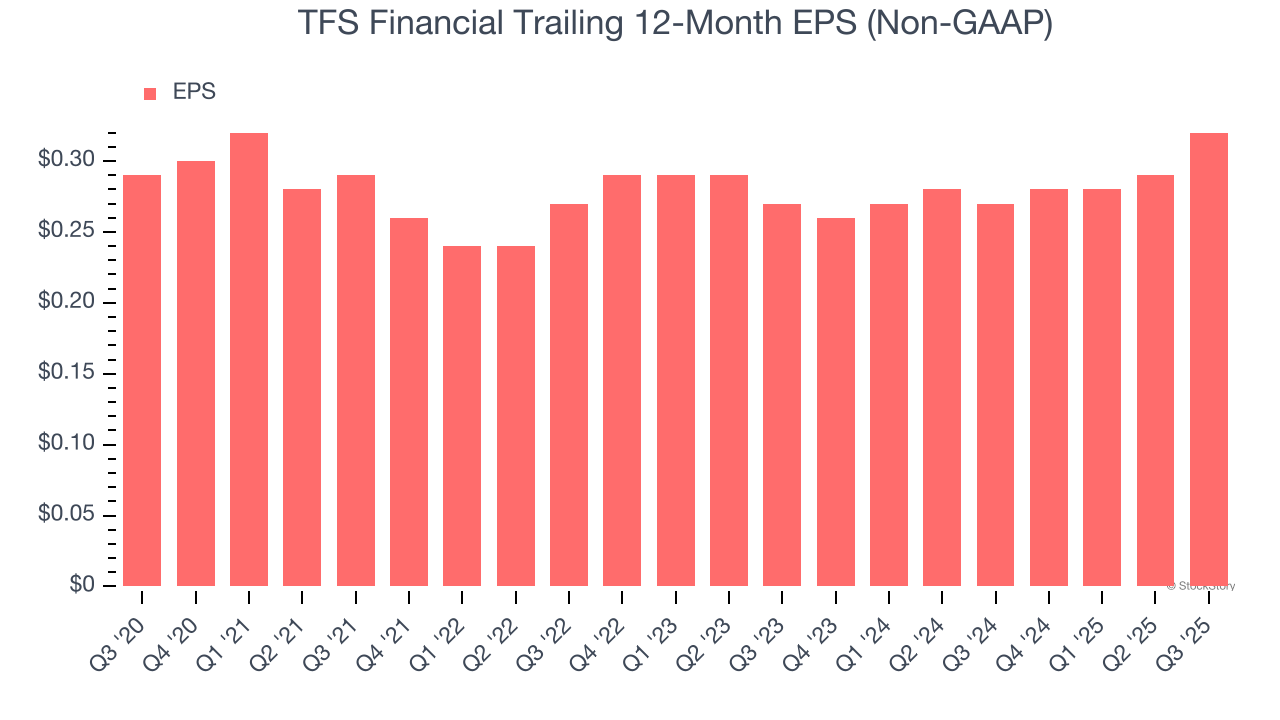

3. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

TFS Financial’s weak 2% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Final Judgment

TFS Financial falls short of our quality standards. With its shares outperforming the market lately, the stock trades at 2.5× forward P/B (or $17.54 per share). At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now. We’d suggest looking at our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of TFS Financial

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.