Looking back on personal loan stocks’ Q1 earnings, we examine this quarter’s best and worst performers, including Nubank (NYSE: NU) and its peers.

Personal loan providers offer unsecured credit for various consumer needs. The sector benefits from digital application processes, increasing consumer comfort with online financial services, and opportunities in underserved credit segments. Headwinds include credit risk management in unsecured lending, regulatory oversight of lending practices, and intense competition affecting margins from both traditional and fintech lenders.

The 9 personal loan stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 2% while next quarter’s revenue guidance was 0.8% below.

In light of this news, share prices of the companies have held steady as they are up 2.7% on average since the latest earnings results.

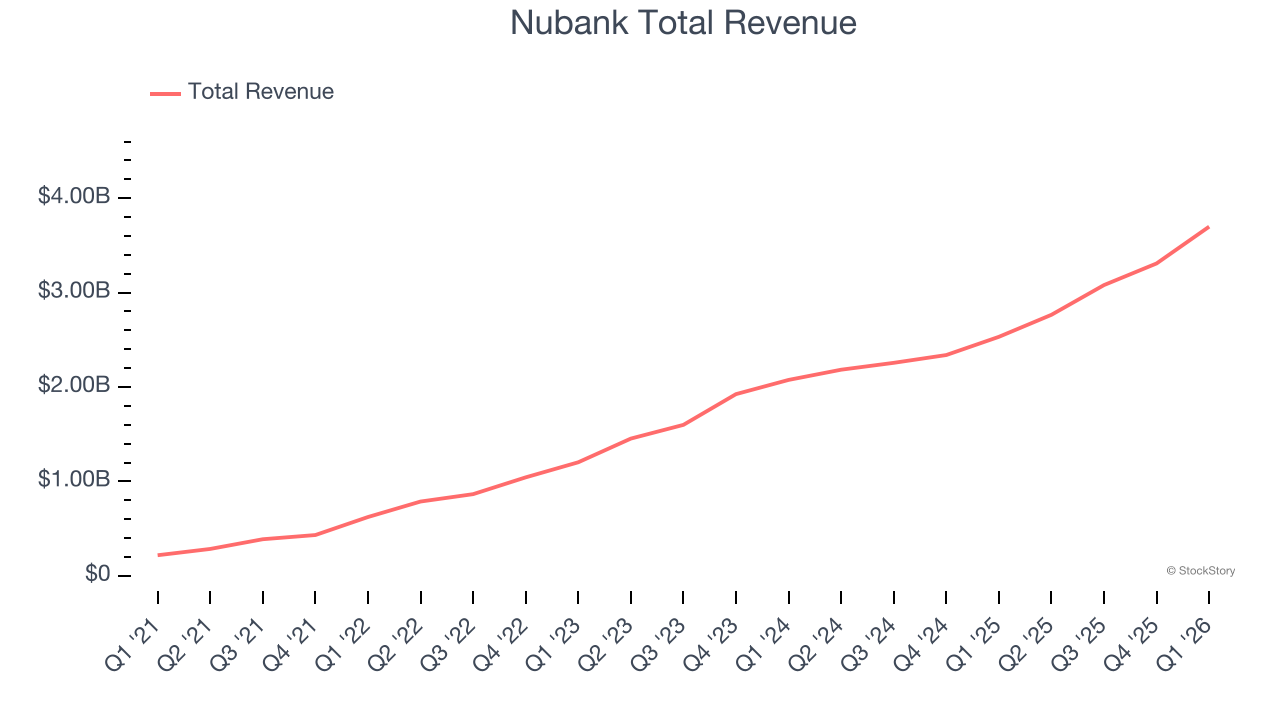

Nubank (NYSE: NU)

With well over one hundred million customers across Brazil, Mexico, and Colombia through its viral member-get-member referral program, Nubank (NYSE: NU) is a digital banking platform that offers financial services including spending, saving, investing, borrowing, and protection products to millions of customers across Latin America.

Nubank reported revenues of $3.70 billion, up 46.1% year on year. This print exceeded analysts’ expectations by 3.6%. Despite the top-line beat, it was still a mixed quarter for the company with a solid beat of analysts’ revenue estimates but a significant miss of analysts’ EPS estimates.

Unsurprisingly, the stock is down 8.1% since reporting and currently trades at $11.89.

Is now the time to buy Nubank? Access our full analysis of the earnings results here, it’s free.

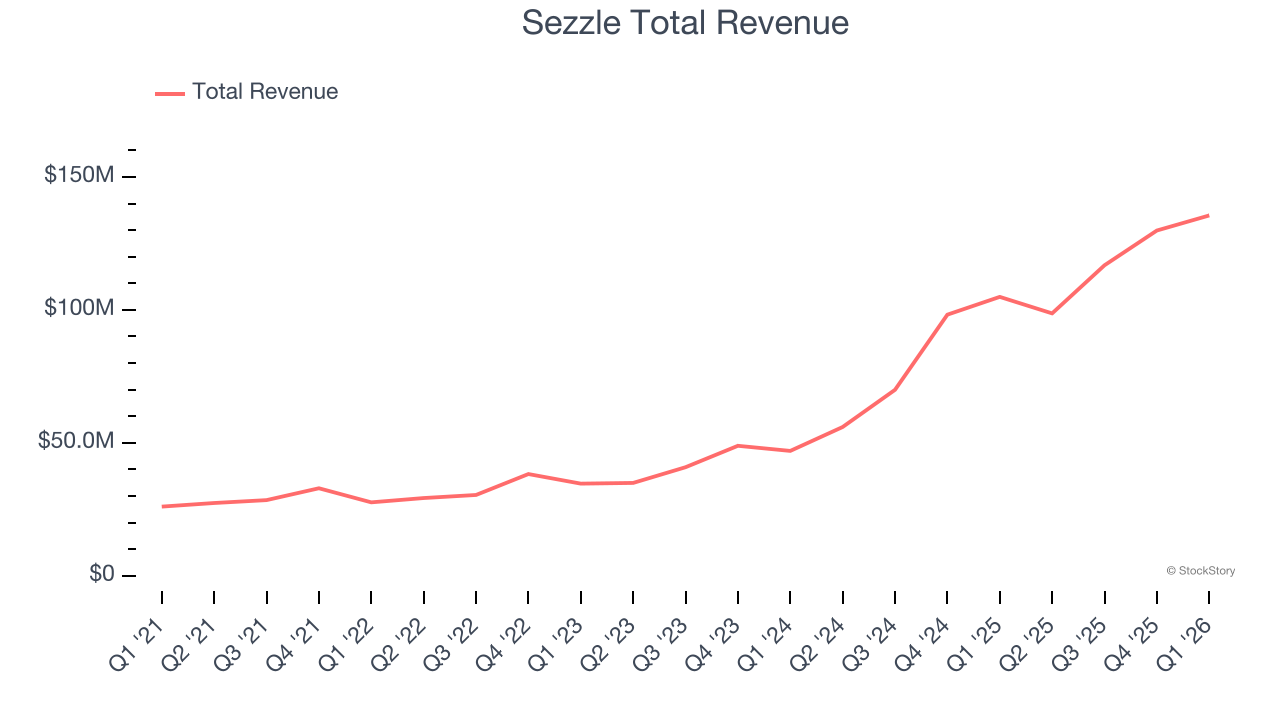

Best Q1: Sezzle (NASDAQ: SEZL)

Founded in 2016 as an alternative to traditional credit cards for younger shoppers, Sezzle (NASDAQ: SEZL) provides a payment platform that allows consumers to split purchases into four interest-free installments over six weeks at participating retailers.

Sezzle reported revenues of $135.5 million, up 29.2% year on year, outperforming analysts’ expectations by 5.3%. The business had a stunning quarter with full-year EPS guidance exceeding analysts’ expectations and an impressive beat of analysts’ EBITDA estimates.

Sezzle delivered the biggest analyst estimate beat among its peers. The market seems happy with the results as the stock is up 38.5% since reporting. It currently trades at $119.18.

Is now the time to buy Sezzle? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Affirm (NASDAQ: AFRM)

Founded by PayPal co-founder Max Levchin with a mission to create honest financial products, Affirm (NASDAQ: AFRM) provides a payment network that allows consumers to make purchases and pay for them over time with transparent, flexible installment loans.

Affirm reported revenues of $1.04 billion, up 32.6% year on year, exceeding analysts’ expectations by 4.3%. Still, it was a slower quarter as it posted a significant miss of analysts’ EPS estimates.

Interestingly, the stock is up 4.5% since the results and currently trades at $70.39.

Read our full analysis of Affirm’s results here.

OneMain (NYSE: OMF)

Dating back to 1912 and formerly known as Springleaf, OneMain Holdings (NYSE: OMF) provides personal loans, auto financing, and credit cards to nonprime consumers who have limited access to traditional banking services.

OneMain reported revenues of $1.26 billion, up 6.6% year on year. This result met analysts’ expectations. Aside from that, it was a mixed quarter as it also produced a beat of analysts’ EPS estimates but revenue in line with analysts’ estimates.

OneMain had the slowest revenue growth among its peers. The stock is down 8.3% since reporting and currently trades at $53.87.

Read our full, actionable report on OneMain here, it’s free.

FirstCash (NASDAQ: FCFS)

Offering a financial lifeline to the unbanked and credit-constrained since 1988, FirstCash (NASDAQ: FCFS) operates pawn stores across the U.S. and Latin America while also providing retail point-of-sale payment solutions for credit-constrained consumers.

FirstCash reported revenues of $1.05 billion, up 25.7% year on year. This print surpassed analysts’ expectations by 4.8%. It was an exceptional quarter as it also recorded an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ revenue estimates.

The stock is down 1.5% since reporting and currently trades at $209.25.

Read our full, actionable report on FirstCash here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.