Over the past six months, Matador Resources has been a great trade, beating the S&P 500 by 14.1%. Its stock price has climbed to $51.03, representing a healthy 23.3% increase. This run-up might have investors contemplating their next move.

Is now still a good time to buy MTDR? Or are investors being too optimistic? Find out in our full research report, it’s free.

Why Are We Positive on MTDR?

Operating primarily in the Delaware Basin where multiple oil-bearing layers lie stacked thousands of feet deep, Matador Resources (NYSE: MTDR) explores for, drills, and produces oil and natural gas from underground rock formations in New Mexico and Texas.

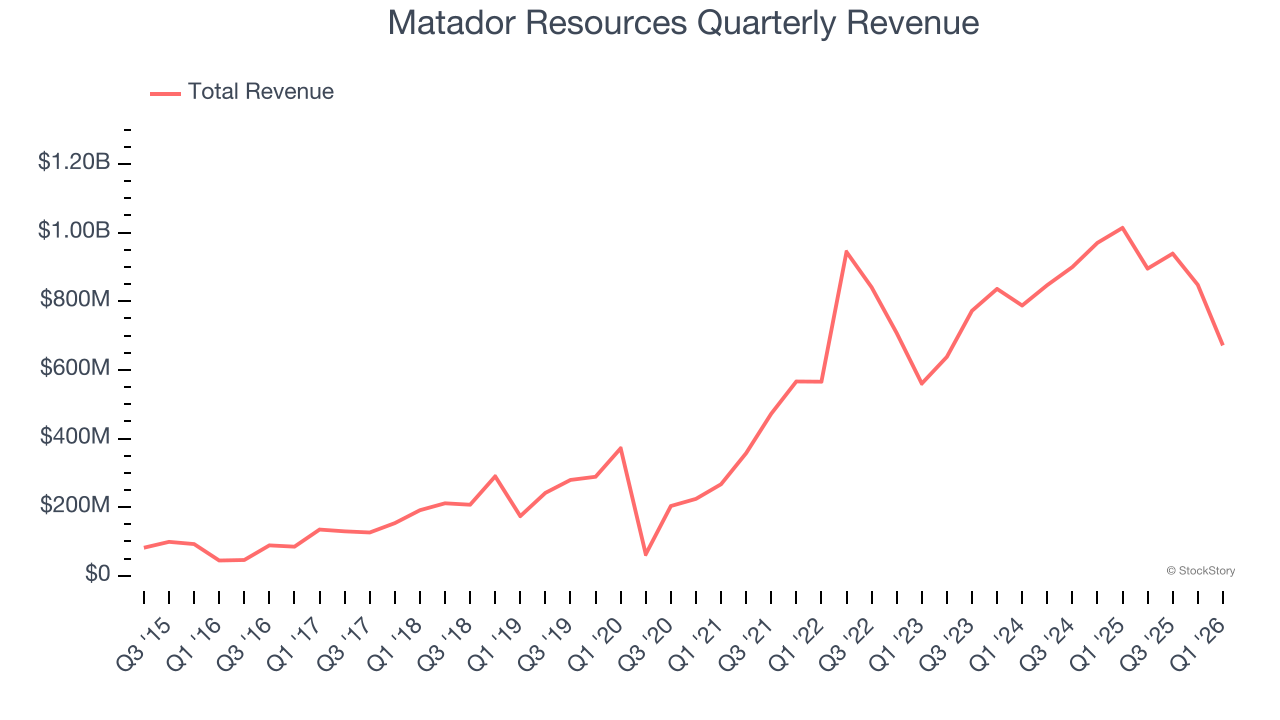

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Thankfully, Matador Resources’s 34.7% annualized revenue growth over the last five years was incredible. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

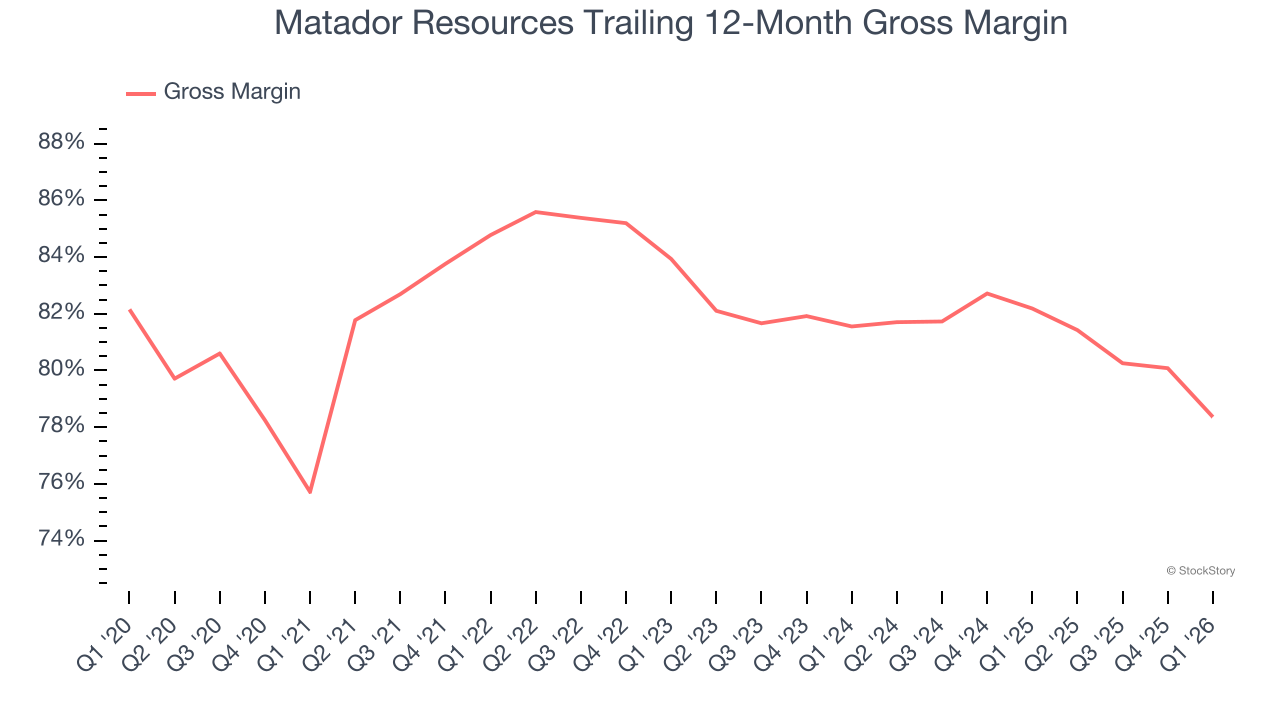

2. Elite Gross Margin Powers Best-In-Class Business Model

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

Matador Resources, which averaged 81.9% gross margin over the last five years, exhibits enviable unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an advantaged starting point for ultimate operating profits and free cash flow generation.

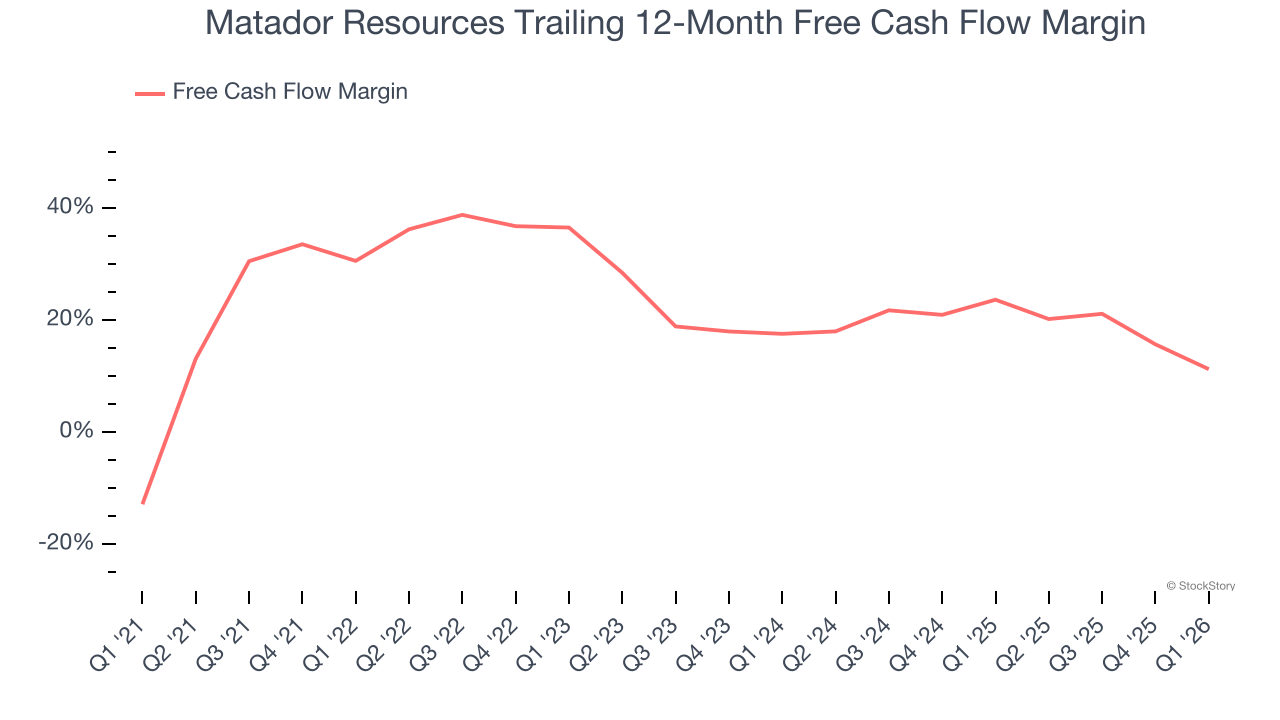

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Matador Resources has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging 23.2% over the last five years.

Final Judgment

These are just a few reasons why Matador Resources is a cream-of-the-crop energy upstream and integrated energy company, and with its shares beating the market recently, the stock trades at 6.2× forward P/E (or $51.03 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.