Over the last six months, Stryker’s shares have sunk to $310.00, producing a disappointing 11.9% loss - a stark contrast to the S&P 500’s 9.3% gain. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Following the drawdown, is now the time to buy SYK? Find out in our full research report, it’s free.

Why Do Investors Watch Stryker?

With over 150 million patients impacted annually through its innovative healthcare technologies, Stryker (NYSE: SYK) develops and manufactures advanced medical devices and equipment across orthopedics, surgical tools, neurotechnology, and patient care solutions.

Three Things to Like:

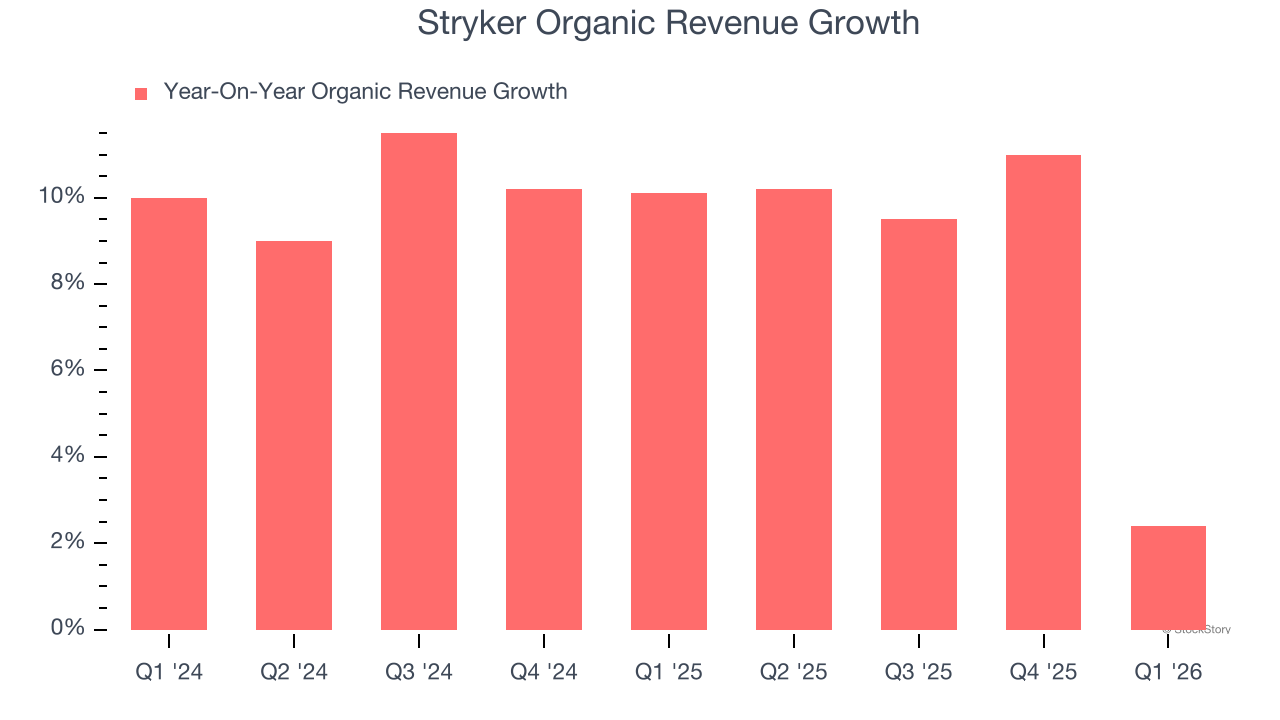

1. Organic Growth Indicates Solid Core Business

Investors interested in Medical Devices & Supplies - Diversified companies should track organic revenue in addition to reported revenue. This metric gives visibility into Stryker’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Stryker’s organic revenue averaged 9.2% year-on-year growth. This performance was solid and shows it can expand steadily without relying on expensive (and risky) acquisitions.

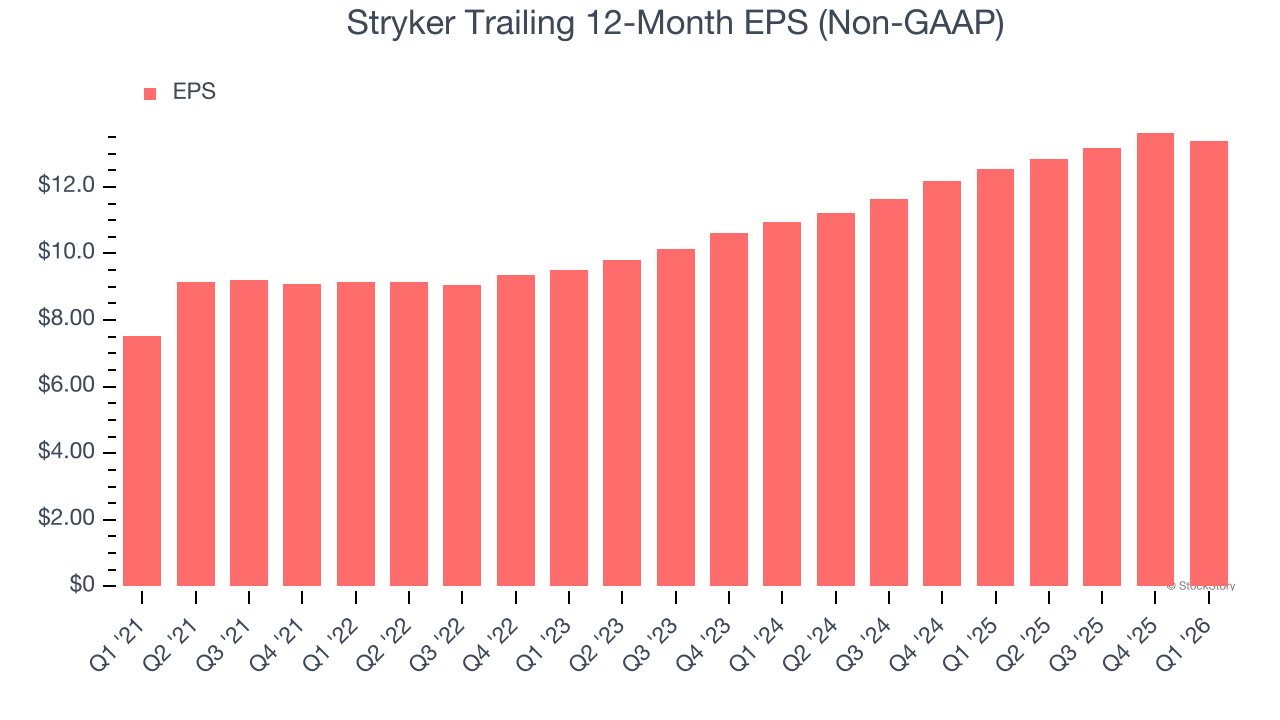

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Stryker’s spectacular 12.2% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

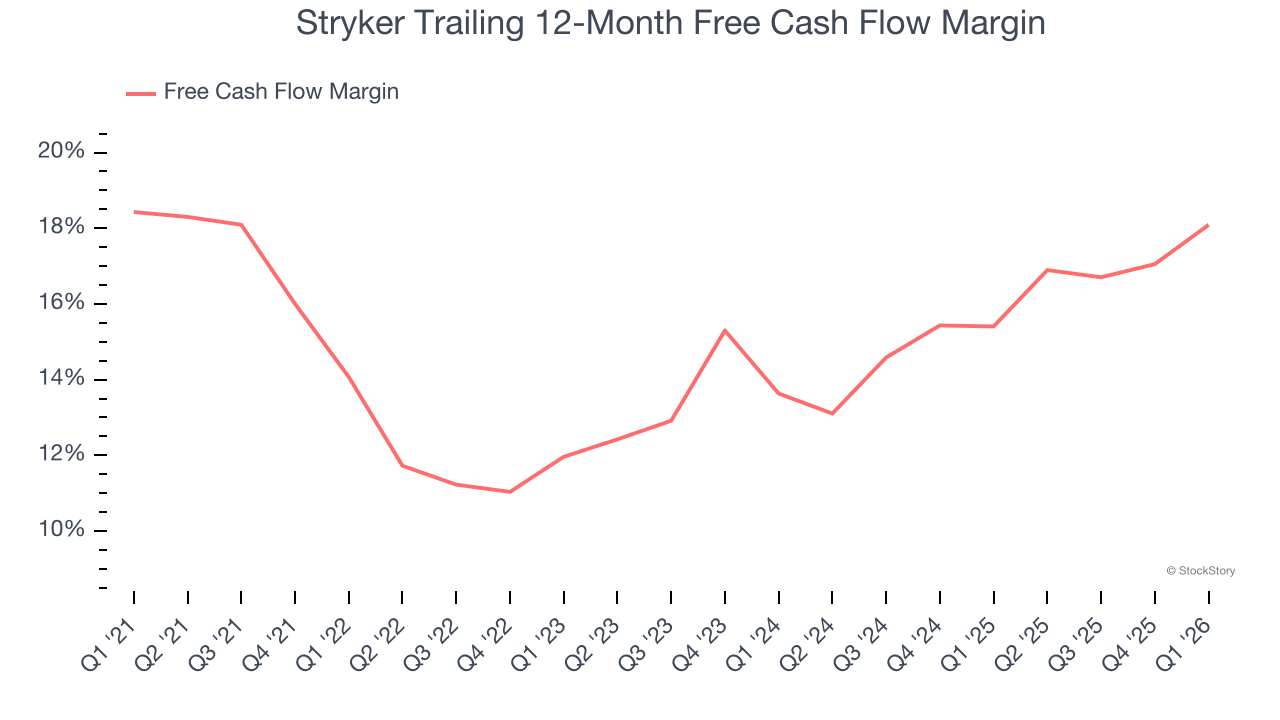

3. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Stryker’s margin expanded by 4 percentage points over the last five years. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat. Stryker’s free cash flow margin for the trailing 12 months was 18.1%.

Final Judgment

Stryker possesses several positive attributes. With the recent decline, the stock trades at 19.9× forward P/E (or $310.00 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.