Government IT services provider Science Applications International Corporation (NASDAQ: SAIC) announced better-than-expected revenue in Q1 CY2026, with sales up 1.5% year on year to $1.91 billion. On the other hand, the company’s full-year revenue guidance of $7.1 billion at the midpoint came in 0.7% below analysts’ estimates. Its non-GAAP profit of $3.23 per share was 41.8% above analysts’ consensus estimates.

Is now the time to buy SAIC? Find out by accessing our full research report, it’s free.

SAIC (SAIC) Q1 CY2026 Highlights:

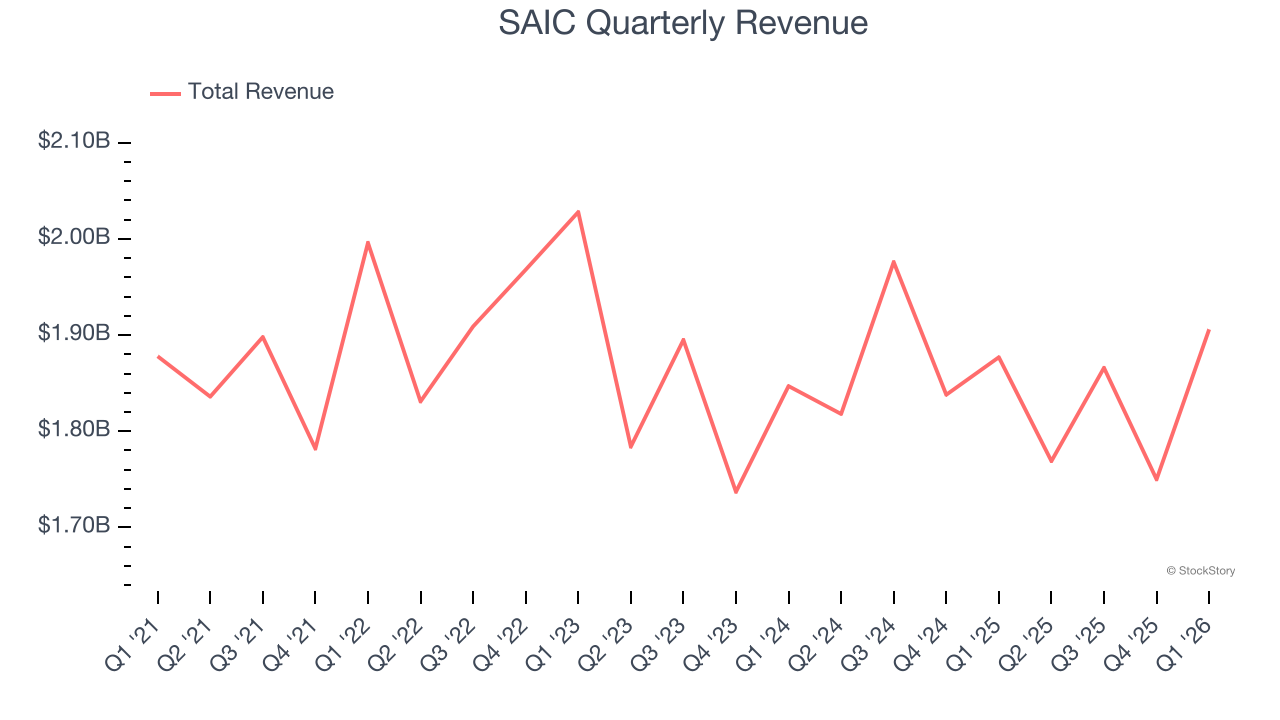

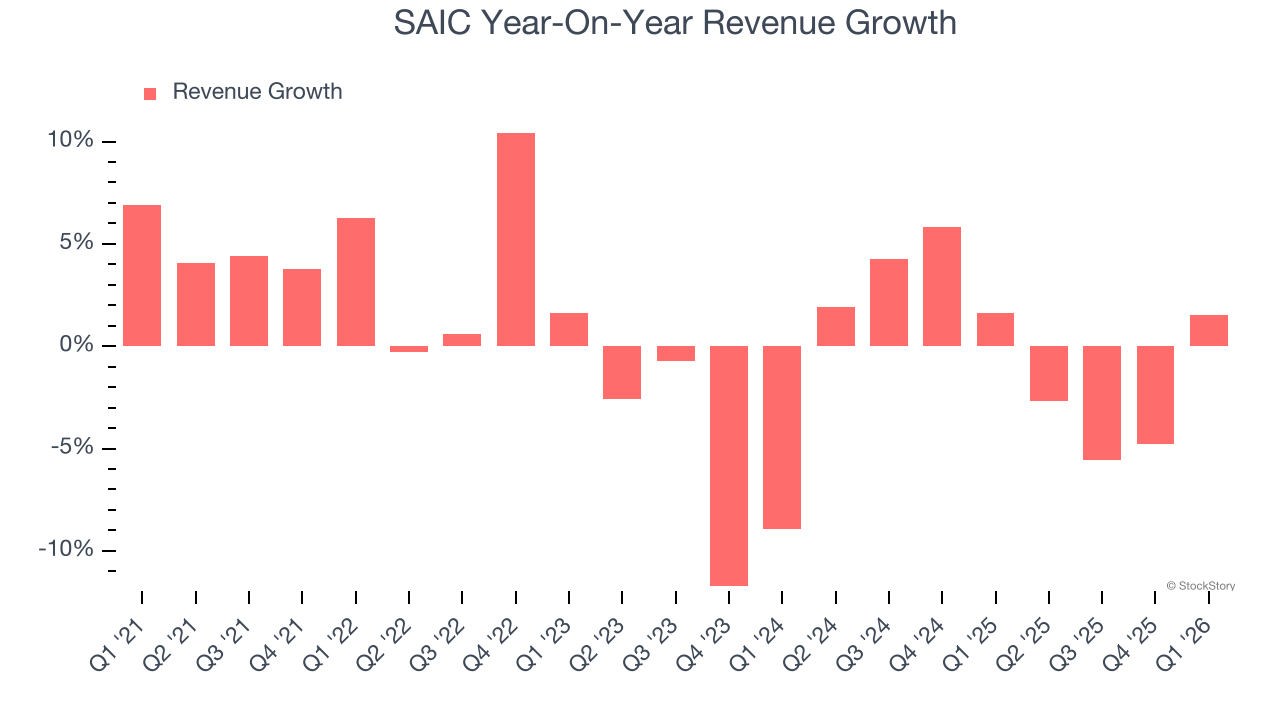

- Revenue: $1.91 billion vs analyst estimates of $1.83 billion (1.5% year-on-year growth, 4.1% beat)

- Adjusted EPS: $3.23 vs analyst estimates of $2.28 (41.8% beat)

- Adjusted EBITDA: $222 million vs analyst estimates of $175.1 million (11.6% margin, 26.8% beat)

- The company reconfirmed its revenue guidance for the full year of $7.1 billion at the midpoint

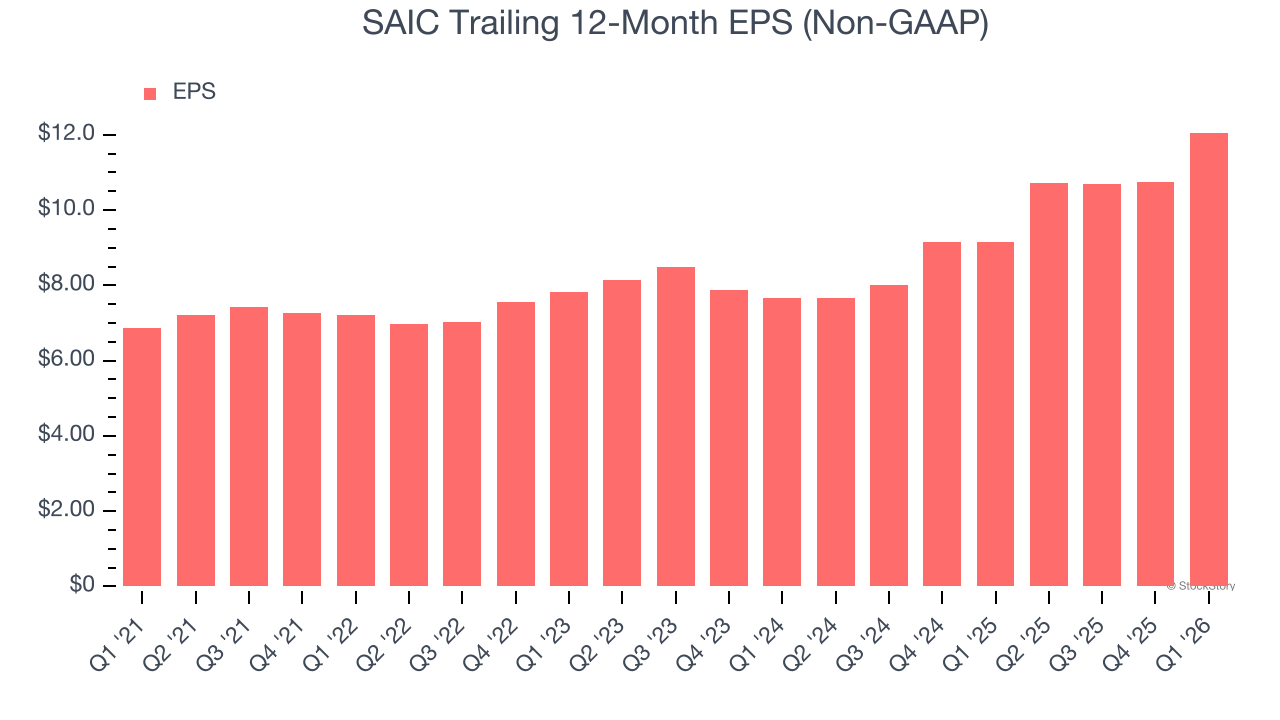

- Management raised its full-year Adjusted EPS guidance to $10 at the midpoint, a 4.2% increase

- EBITDA guidance for the full year is $725 million at the midpoint, above analyst estimates of $712.3 million

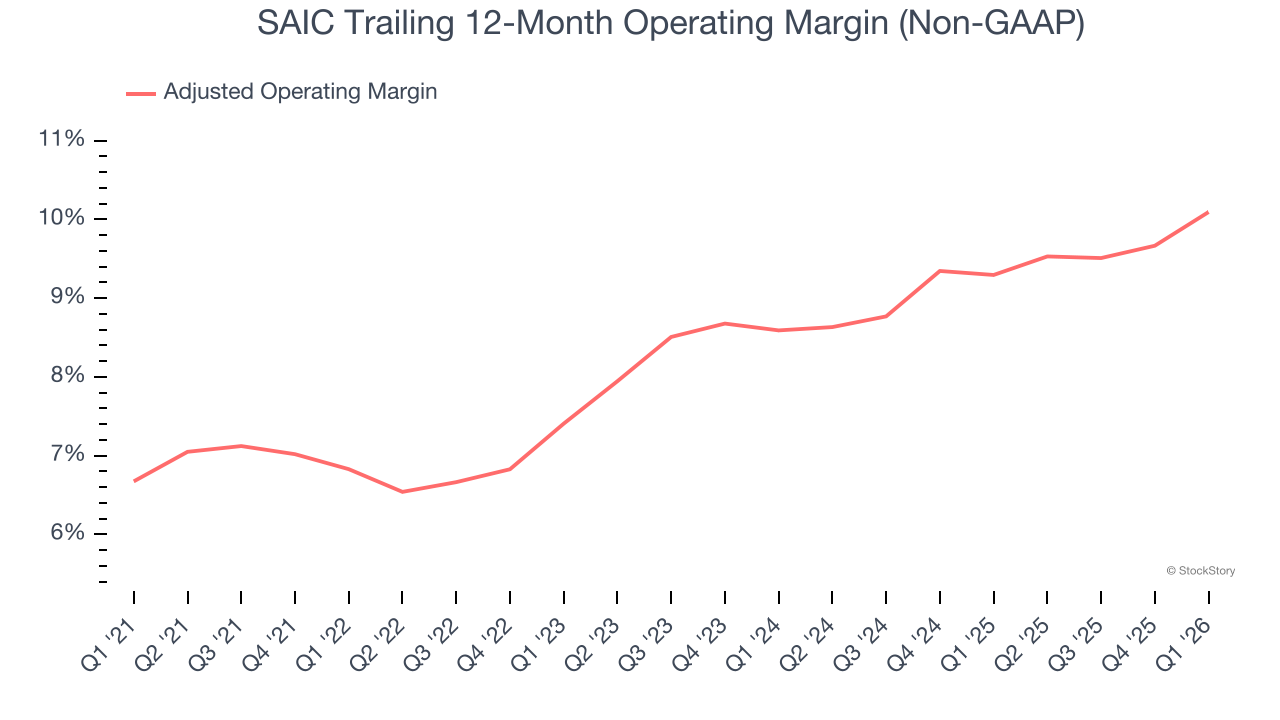

- Operating Margin: 9.4%, up from 6.4% in the same quarter last year

- Free Cash Flow was $118 million, up from -$44 million in the same quarter last year

- Backlog: $22.9 billion at quarter end, up 2.5% year on year

- Market Capitalization: $4.49 billion

Company Overview

With over five decades of experience supporting national security missions, Science Applications International Corporation (NASDAQ: SAIC) provides technical, engineering, and enterprise IT services primarily to U.S. government agencies and military branches.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $7.29 billion in revenue over the past 12 months, SAIC is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s challenging to maintain high growth rates when you’ve already captured a large portion of the addressable market. To accelerate sales, SAIC likely needs to optimize its pricing or lean into new offerings and international expansion.

As you can see below, SAIC struggled to increase demand as its $7.29 billion of sales for the trailing 12 months was close to its revenue five years ago. This shows demand was soft, a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Just like its five-year trend, SAIC’s revenue over the last two years was flat, suggesting it is in a slump.

This quarter, SAIC reported modest year-on-year revenue growth of 1.5% but beat Wall Street’s estimates by 4.1%.

Looking ahead, sell-side analysts expect revenue to decline by 2.3% over the next 12 months, a slight deceleration versus the last two years. This projection doesn’t excite us and suggests its products and services will face some demand challenges.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

SAIC was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 8.4% was weak for a business services business.

On the plus side, SAIC’s adjusted operating margin rose by 3.3 percentage points over the last five years.

This quarter, SAIC generated an adjusted operating margin profit margin of 10.1%, up 1.7 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth — for example, a company could inflate its sales through excessive spending on advertising and promotions.

SAIC’s EPS grew at 11.9% compounded annual growth rate over the last five years, higher than its flat revenue. This tells us management responded to softer demand by adapting its cost structure.

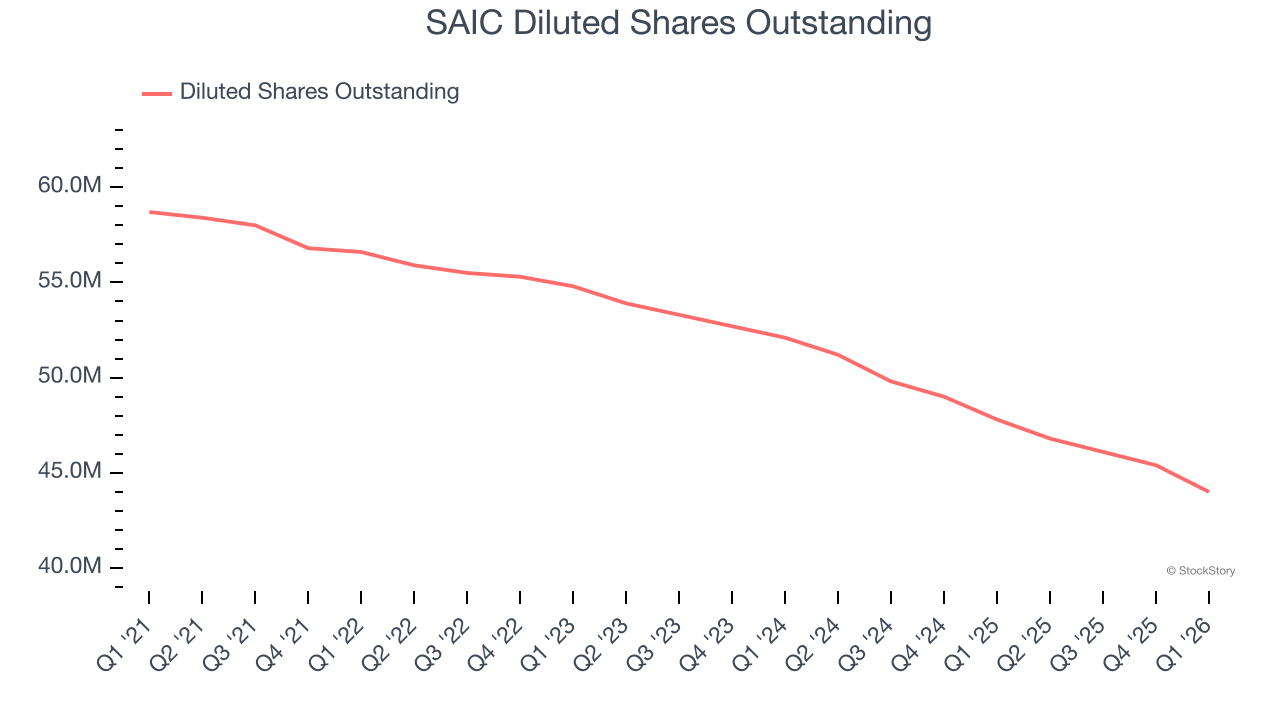

We can take a deeper look into SAIC’s earnings to better understand the drivers of its performance. As we mentioned earlier, SAIC’s adjusted operating margin expanded by 3.3 percentage points over the last five years. On top of that, its share count shrank by 25%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For SAIC, its two-year annual EPS growth of 25.4% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, SAIC reported adjusted EPS of $3.23, up from $1.92 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects SAIC’s full-year EPS to shrink by 17.4% from $12.06 to $9.96.

Key Takeaways from SAIC’s Q1 Results

It was good to see SAIC beat analysts’ revenue, EBITDA, and EPS expectations this quarter. We were also glad its full-year EBITDA guidance beat and its full-year EPS guidance was raised. Zooming out, we think this was a very good print. The stock traded up 8.1% to $112.62 immediately following the results.

Sure, SAIC had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).