Crown Holdings has been treading water for the past six months, recording a small loss of 2.3% while holding steady at $95.12. The stock also fell short of the S&P 500’s 10.9% gain during that period.

Is there a buying opportunity in Crown Holdings, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Crown Holdings Not Exciting?

We’re sitting this one out for now. Here are three reasons we avoid CCK, plus one stock we’d rather own.

1. Long-Term Revenue Growth Disappoints

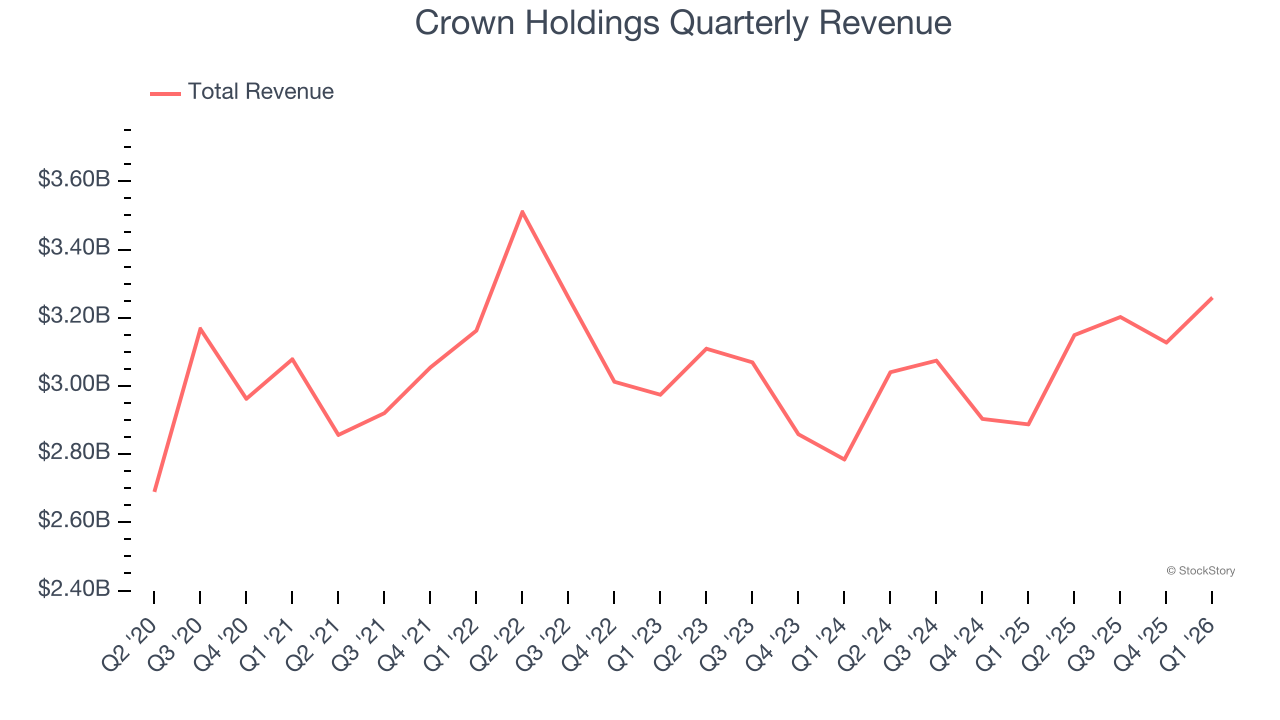

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Crown Holdings grew its sales at a weak 1.4% compounded annual growth rate. This fell short of our benchmarks.

2. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

Crown Holdings has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 20.3% gross margin over the last five years. Said differently, Crown Holdings had to pay a chunky $79.65 to its suppliers for every $100 in revenue.

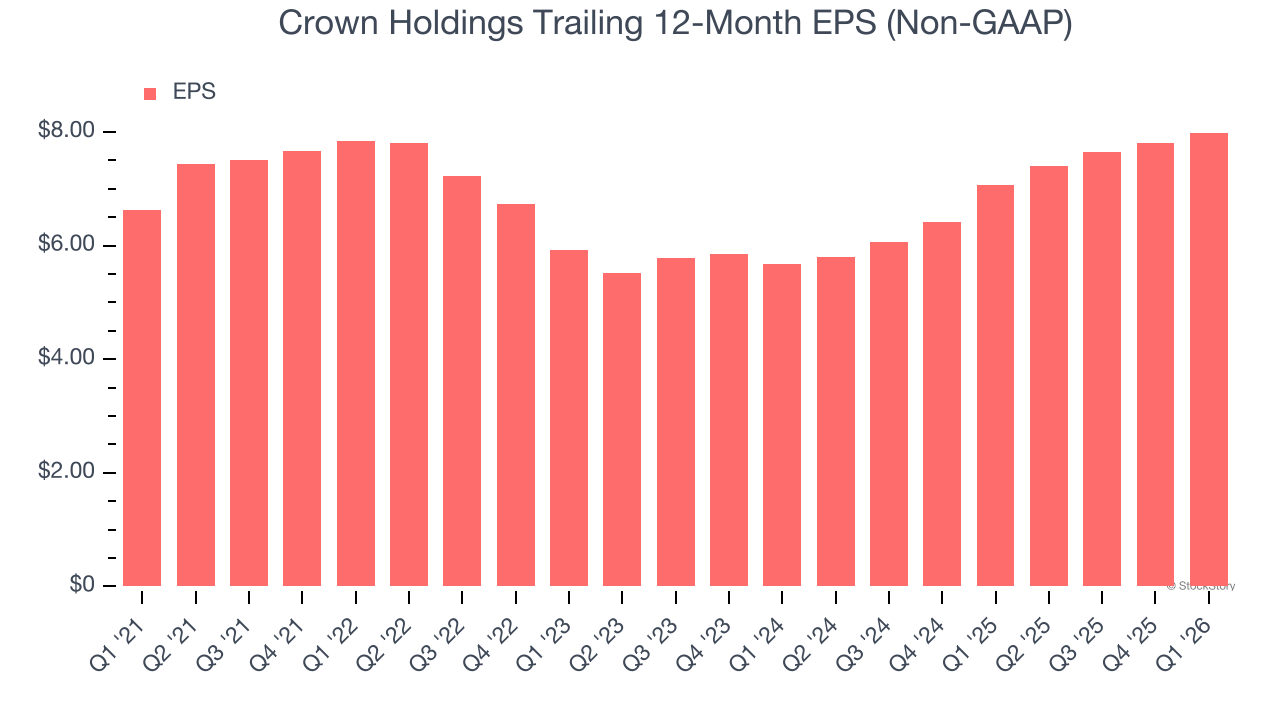

3. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Crown Holdings’s EPS grew at 3.8% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 1.4% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

Crown Holdings isn’t a terrible business, but it doesn’t pass our quality test. With its shares trailing the market in recent months, the stock trades at 12× forward P/E (or $95.12 per share). This valuation multiple is fair, but we don’t have much faith in the company. We’re pretty confident there are superior stocks to buy right now. We’d recommend looking at a dominant aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Crown Holdings

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.