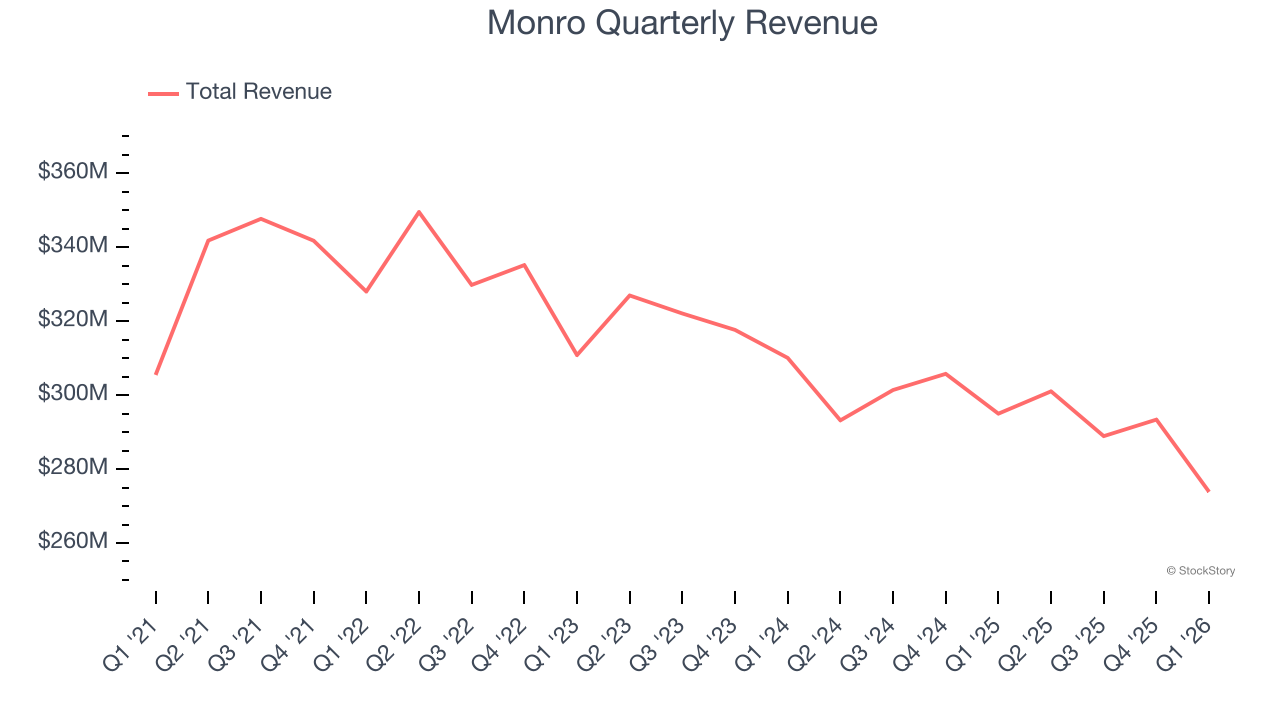

Auto services provider Monro (NASDAQ: MNRO) fell short of the market’s revenue expectations in Q1 CY2026, with sales falling 7.2% year on year to $273.8 million. Its non-GAAP loss of $0.16 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Monro? Find out by accessing our full research report, it’s free.

Monro (MNRO) Q1 CY2026 Highlights:

- Revenue: $273.8 million vs analyst estimates of $283.7 million (7.2% year-on-year decline, 3.5% miss)

- Adjusted EPS: -$0.16 vs analyst estimates of -$0.05 (miss)

- Adjusted Operating Income: -$2.55 million vs analyst estimates of $1.66 million (-0.9% margin, miss)

- Operating Margin: -1.9%, up from -8.1% in the same quarter last year

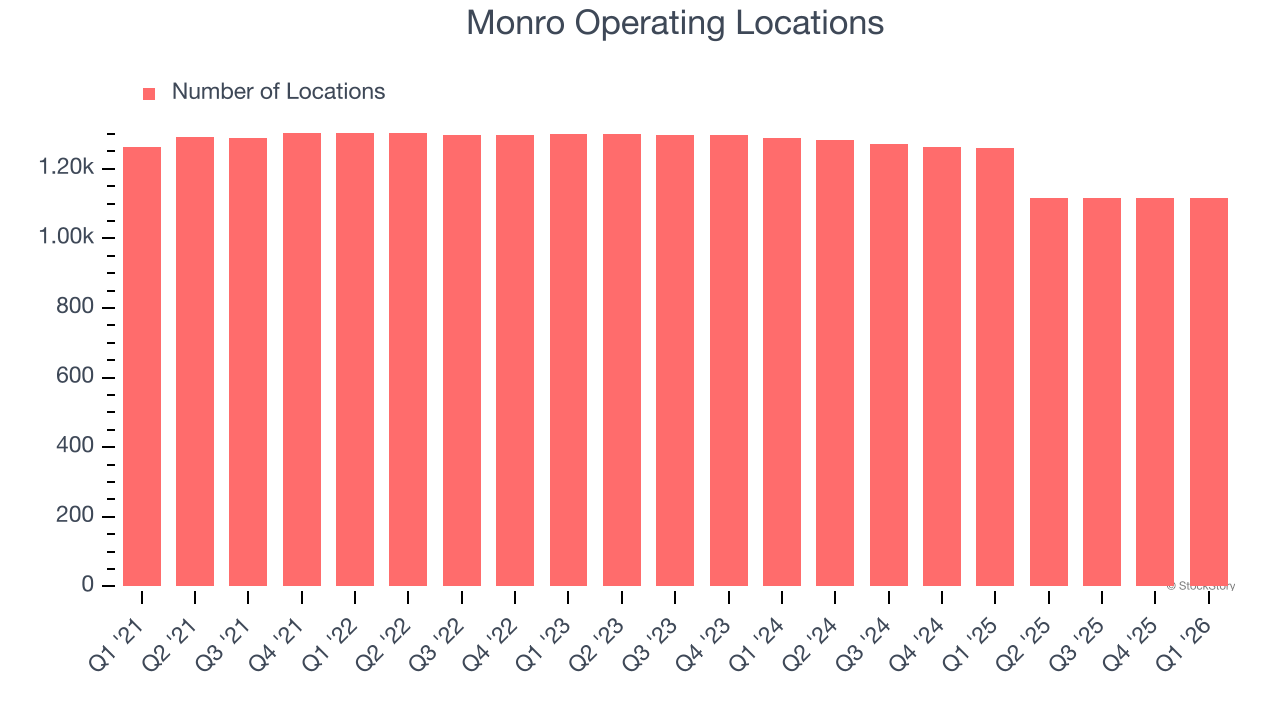

- Locations: 1,115 at quarter end, down from 1,260 in the same quarter last year

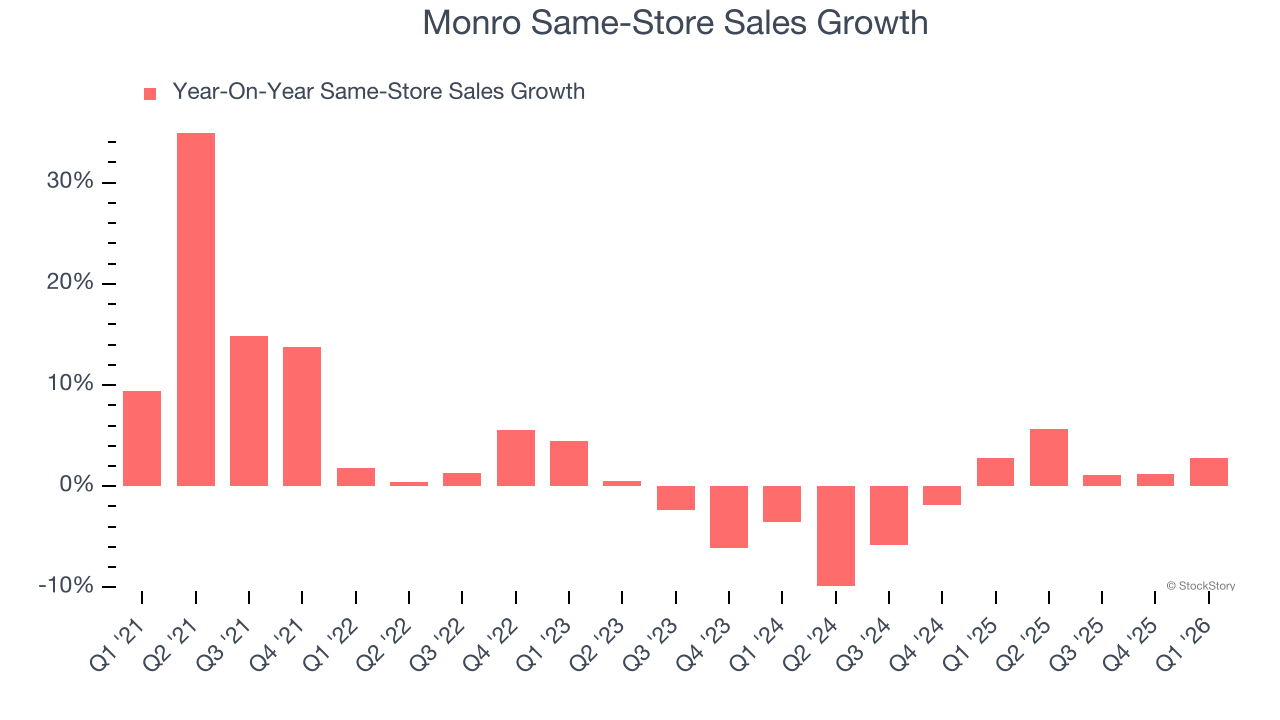

- Same-Store Sales rose 2.8% year on year, in line with the same quarter last year

- Market Capitalization: $497.1 million

“Our fourth quarter results were challenged by a difficult operating environment in the full-service auto aftermarket. As we believe was the case with other tire sellers, this was primarily driven by persistent weakness in tire units that began in fiscal January and continued throughout the quarter. In addition, severe winter weather in fiscal February across our geographic footprint forced temporary store closures and significantly reduced customer traffic during what should have been a busy winter maintenance period. We experienced a 5% decline in tire units during the quarter, which we believe aligns with broader industry trends. Our tire category was pressured as consumers continued to defer spending in higher-ticket categories and gravitated toward lower-cost alternatives. Both comparable store sales and tire units showed sequential improvement in fiscal March, partially recovering from the February weather disruptions. Store traffic also improved sequentially, giving us confidence that underlying demand for our services remains intact, despite a challenging backdrop. Despite the overall sales challenges, our higher-margin service categories continued to deliver value to our many full-service customers and reinforces our strength as a full-service provider. This capability serves as proof that our store teams are effectively utilizing ConfiDrive to identify and communicate service needs to customers. Our gross margin performance was a bright spot, expanding 90 basis points year-over-year to 33.9%. This improvement demonstrates productivity gains from our labor force, even as we navigate cost pressures and shifting customer preferences toward lower-tier products. Importantly, we maintained our marketing investment throughout the quarter, despite the sales headwinds. Monro delivered positive comp store sales in fiscal 2026 for the first time in three years, closed 145 stores that were not going to reach our profit expectations, and dramatically improved our inventory position. And, while the fourth quarter tested our resolve, our results for the full year of fiscal 2026 also validate that our strategic initiatives are working well over time and position us to capitalize when market conditions improve”, said Peter Fitzsimmons, President and Chief Executive Officer.

Company Overview

Started as a single location in Rochester, New York, Monro (NASDAQ: MNRO) provides common auto services such as brake repairs, tire replacements, and oil changes.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $1.16 billion in revenue over the past 12 months, Monro is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Monro struggled to generate demand over the last three years. Its sales dropped by 4.4% annually as it closed stores.

This quarter, Monro missed Wall Street’s estimates and reported a rather uninspiring 7.2% year-on-year revenue decline, generating $273.8 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.5% over the next 12 months. Although this projection indicates its newer products will catalyze better top-line performance, it is still below average for the sector.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Monro operated 1,115 locations in the latest quarter. Over the last two years, the company has generally closed its stores, averaging 7.1% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Monro’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and Monro is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Monro’s same-store sales rose 2.8% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

Key Takeaways from Monro’s Q1 Results

We struggled to find many positives in these results. Its EPS missed and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. Still, the stock traded up 1.1% to $16.75 immediately after reporting.

Is Monro an attractive investment opportunity right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).