Electronics distributor Richardson Electronics (NASDAQ: RELL) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 3.1% year on year to $55.47 million. Its non-GAAP profit of $0.07 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Richardson Electronics? Find out by accessing our full research report, it’s free.

Richardson Electronics (RELL) Q1 CY2026 Highlights:

- Revenue: $55.47 million vs analyst estimates of $53.13 million (3.1% year-on-year growth, 4.4% beat)

- Adjusted EPS: $0.07 vs analyst estimates of $0.02 (significant beat)

- Adjusted EBITDA: $2.18 million vs analyst estimates of $1.73 million (3.9% margin, relatively in line)

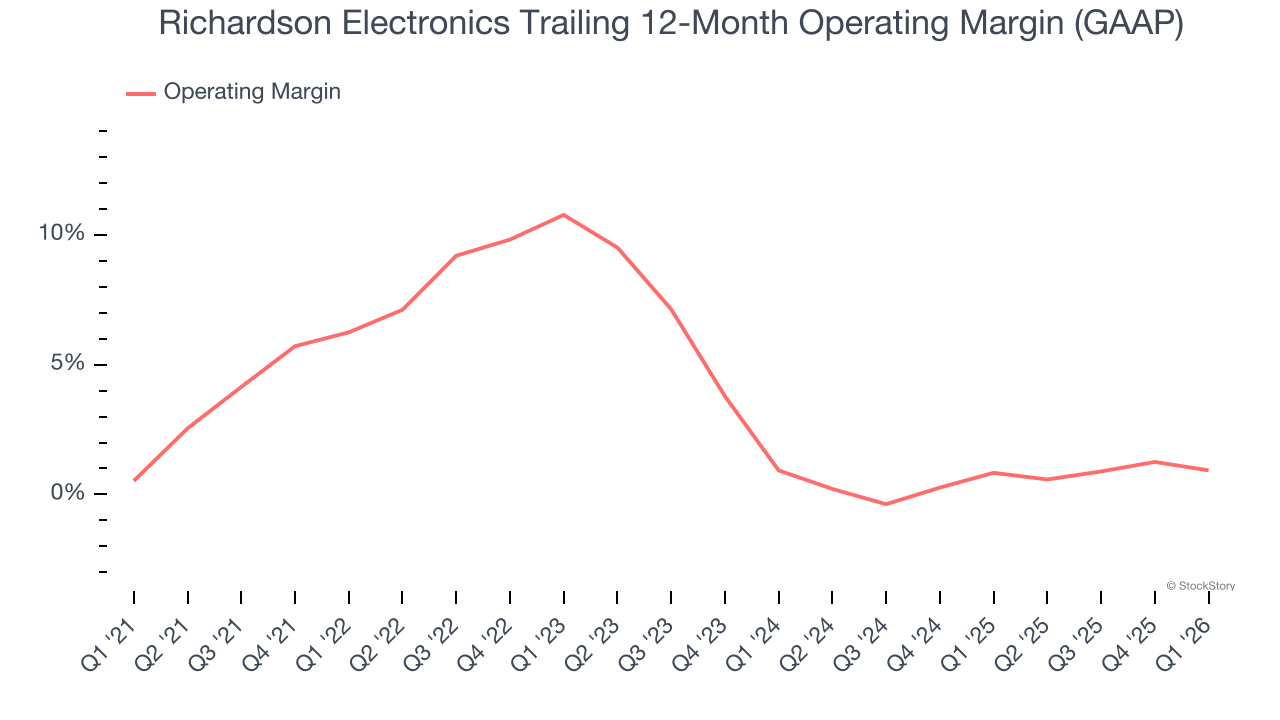

- Operating Margin: 2.7%, down from 4% in the same quarter last year

- Free Cash Flow was -$3.41 million, down from $4.05 million in the same quarter last year

- Backlog: $151.2 million at quarter end, up 12.8% year on year

- Market Capitalization: $162.7 million

“I am pleased to report that Richardson Electronics has now delivered seven consecutive quarters of year-over-year sales growth, reflecting continued progress in executing our multi-year strategy. Our performance this quarter was led by strong momentum in PMT, particularly in EDG and the semifab equipment market. Third quarter sales growth was supported by continued discipline around gross margin and operating expenses. Our performance reflects the strength of our team, as we continue to invest across the organization to build depth, technical expertise, and operating performance,” said Edward J. Richardson, Chairman, CEO, and President.

Company Overview

Founded in 1947, Richardson Electronics (NASDAQ: RELL) is a distributor of power grid and microwave tubes as well as consumables related to those products.

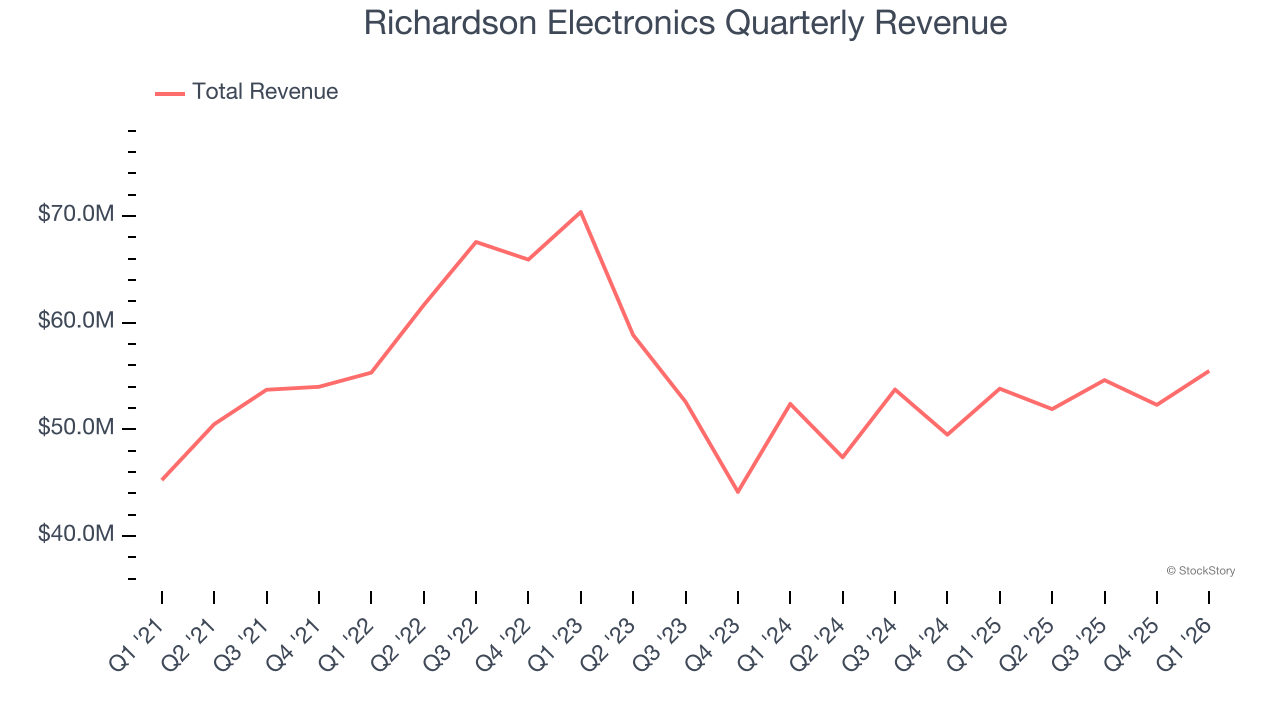

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Richardson Electronics’s sales grew at a tepid 5.5% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Richardson Electronics’s recent performance shows its demand has slowed as its annualized revenue growth of 1.5% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

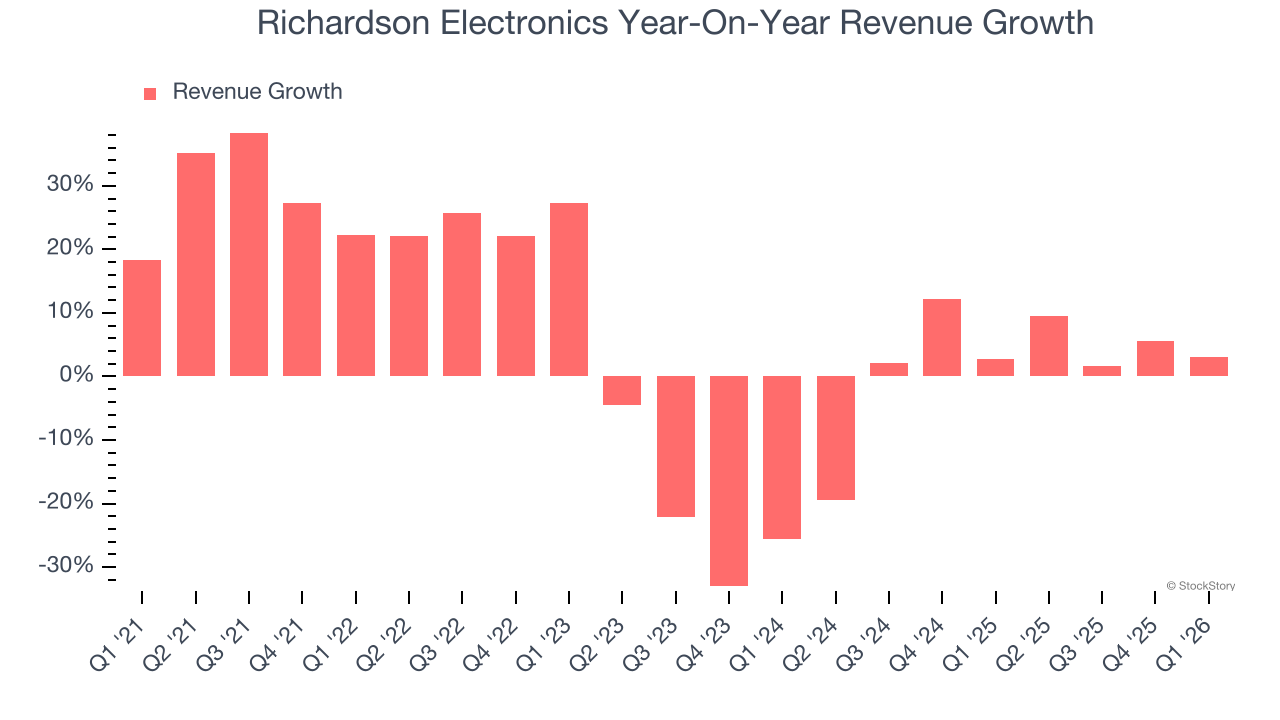

This quarter, Richardson Electronics reported modest year-on-year revenue growth of 3.1% but beat Wall Street’s estimates by 4.4%.

Looking ahead, sell-side analysts expect revenue to grow 11.7% over the next 12 months, an improvement versus the last two years. This projection is commendable and implies its newer products and services will catalyze better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Richardson Electronics was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.3% was weak for an industrials business.

Looking at the trend in its profitability, Richardson Electronics’s operating margin decreased by 5.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Richardson Electronics’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q1, Richardson Electronics generated an operating margin profit margin of 2.7%, down 1.3 percentage points year on year. Since Richardson Electronics’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

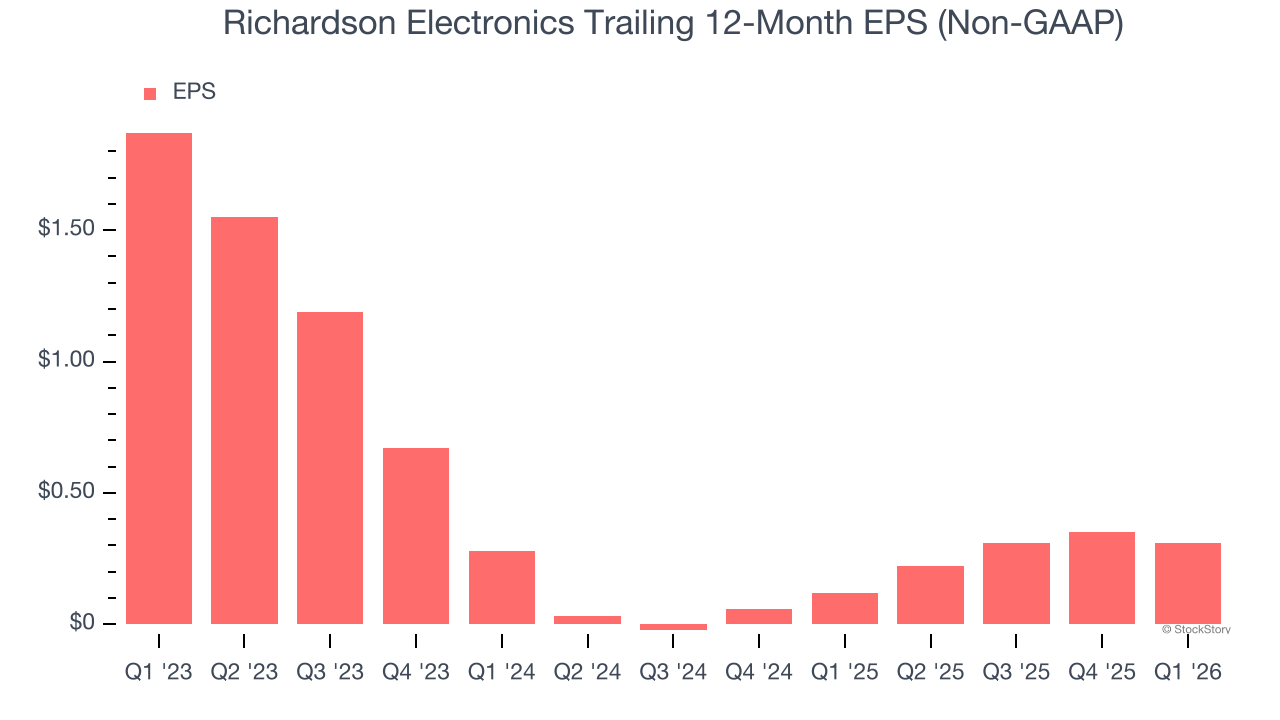

Richardson Electronics’s full-year EPS dropped 162%, or 37.8% annually, over the last three years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Richardson Electronics’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Richardson Electronics, its two-year annual EPS growth of 5.2% was higher than its three-year trend. Accelerating earnings growth is almost always an encouraging data point.

In Q1, Richardson Electronics reported adjusted EPS of $0.07, down from $0.11 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Richardson Electronics’s full-year EPS of $0.31 to grow 48.4%.

Key Takeaways from Richardson Electronics’s Q1 Results

It was good to see Richardson Electronics beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 7.6% to $12.71 immediately following the results.

Richardson Electronics put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).