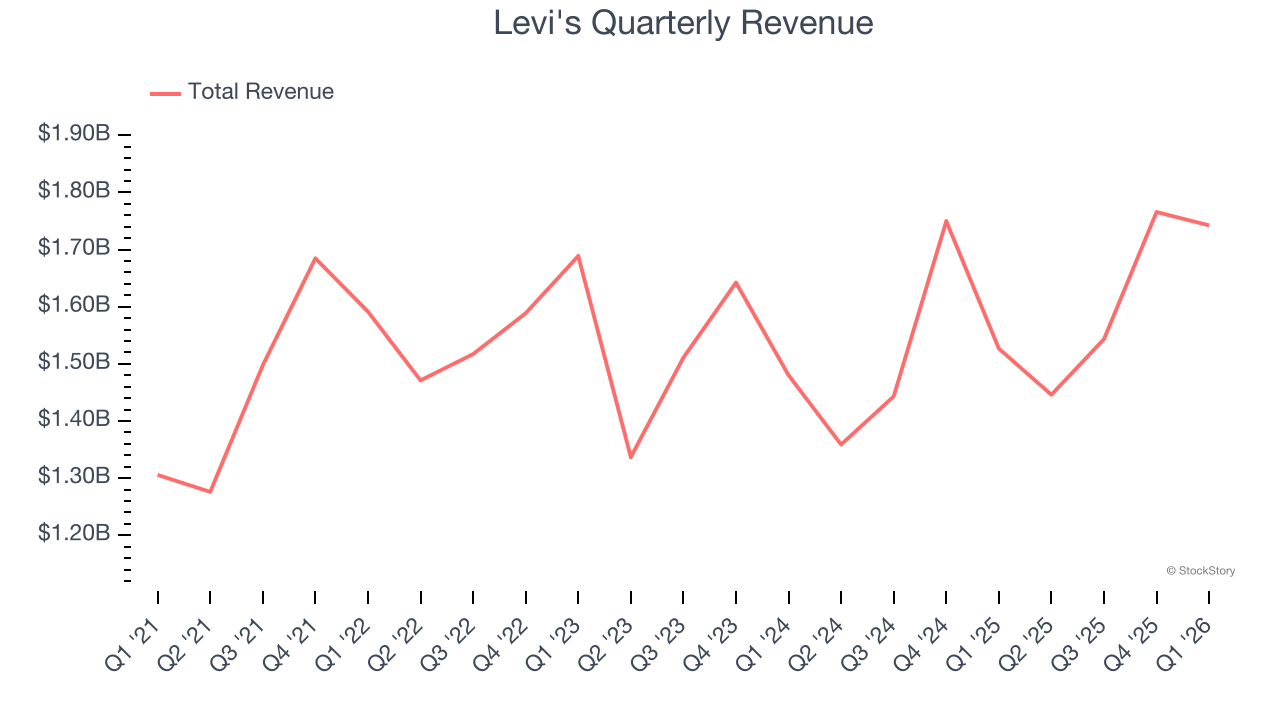

Denim clothing company Levi's (NYSE: LEVI) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 14.1% year on year to $1.74 billion. Its non-GAAP profit of $0.42 per share was 14.4% above analysts’ consensus estimates.

Is now the time to buy Levi's? Find out by accessing our full research report, it’s free.

Levi's (LEVI) Q1 CY2026 Highlights:

- Revenue: $1.74 billion vs analyst estimates of $1.65 billion (14.1% year-on-year growth, 5.6% beat)

- Adjusted EPS: $0.42 vs analyst estimates of $0.37 (14.4% beat)

- Adjusted EBITDA: $273.1 million vs analyst estimates of $249.7 million (15.7% margin, 9.4% beat)

- Management raised its full-year Adjusted EPS guidance to $1.45 at the midpoint, a 1.4% increase

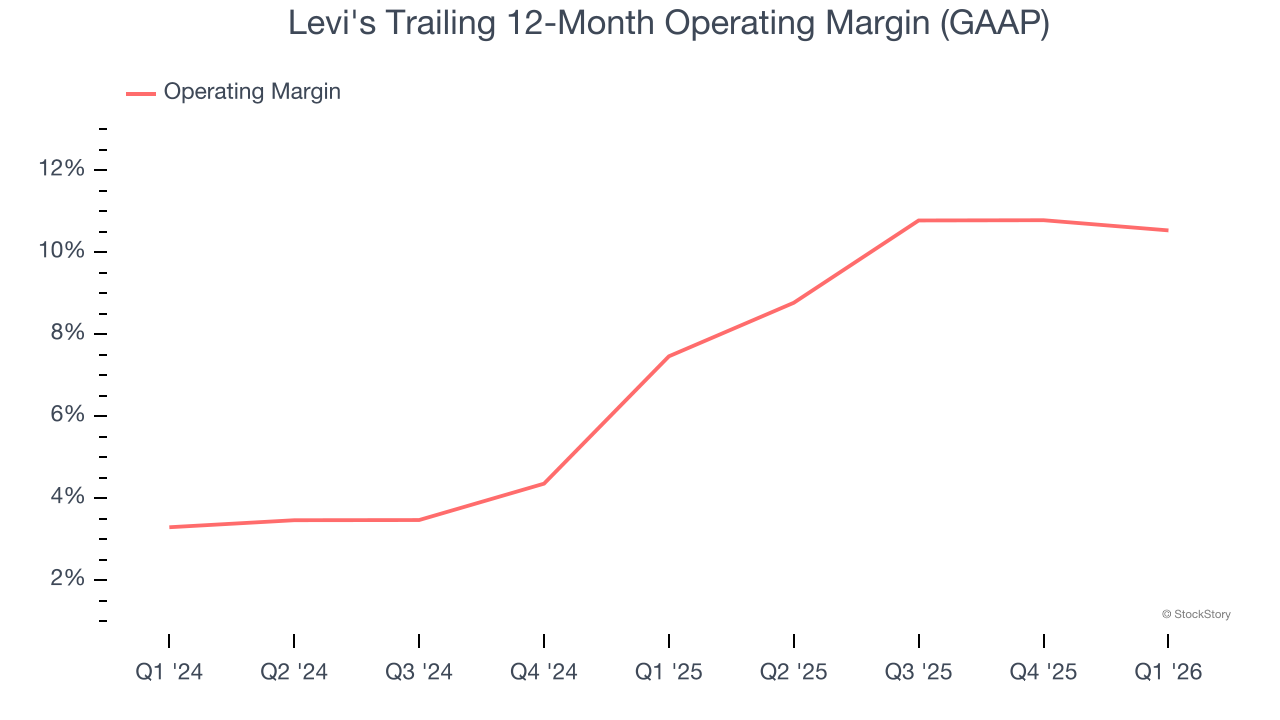

- Operating Margin: 11.4%, down from 12.5% in the same quarter last year

- Free Cash Flow was $152.1 million, up from -$14.1 million in the same quarter last year

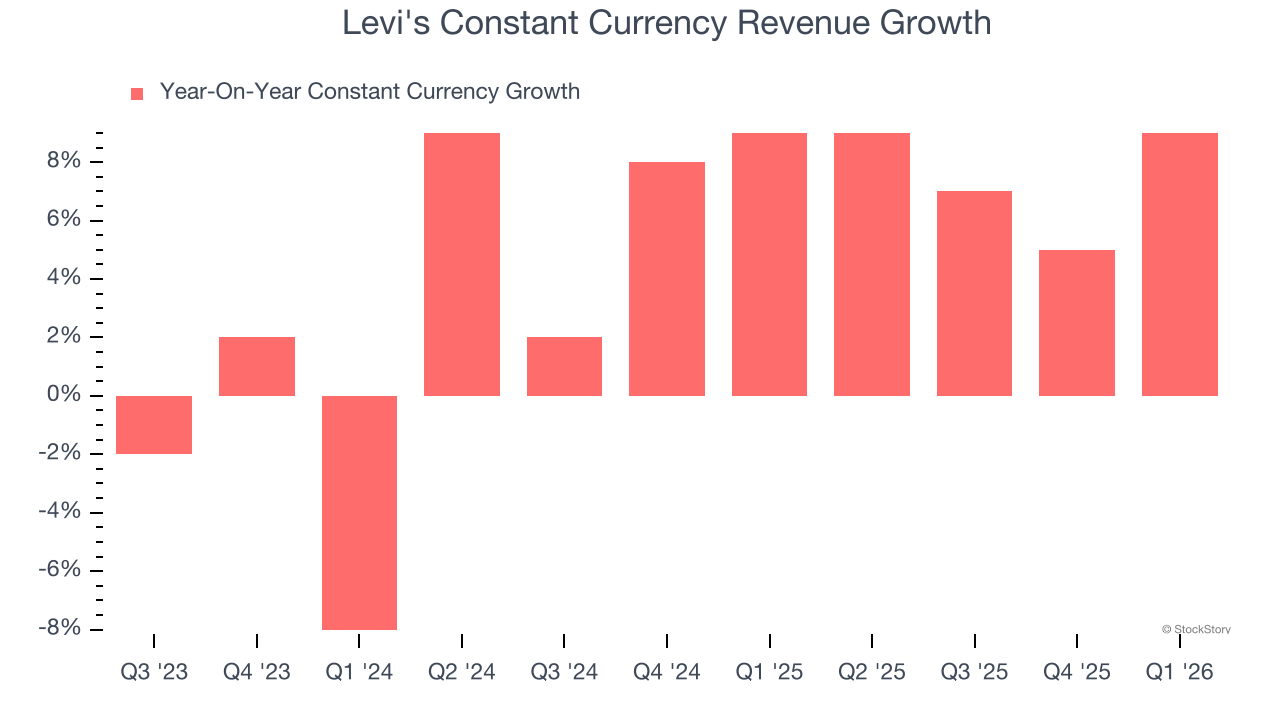

- Constant Currency Revenue rose 9% year on year, in line with the same quarter last year

- Market Capitalization: $7.56 billion

“We delivered very strong financial performance in the first quarter driven by broad-based growth across channels, regions and categories,” said Michelle Gass, President and CEO of Levi Strauss & Co.

Company Overview

Credited for inventing the first pair of blue jeans in 1873, Levi's (NYSE: LEVI) is an apparel company renowned for its iconic denim products and classic American style.

Revenue Growth

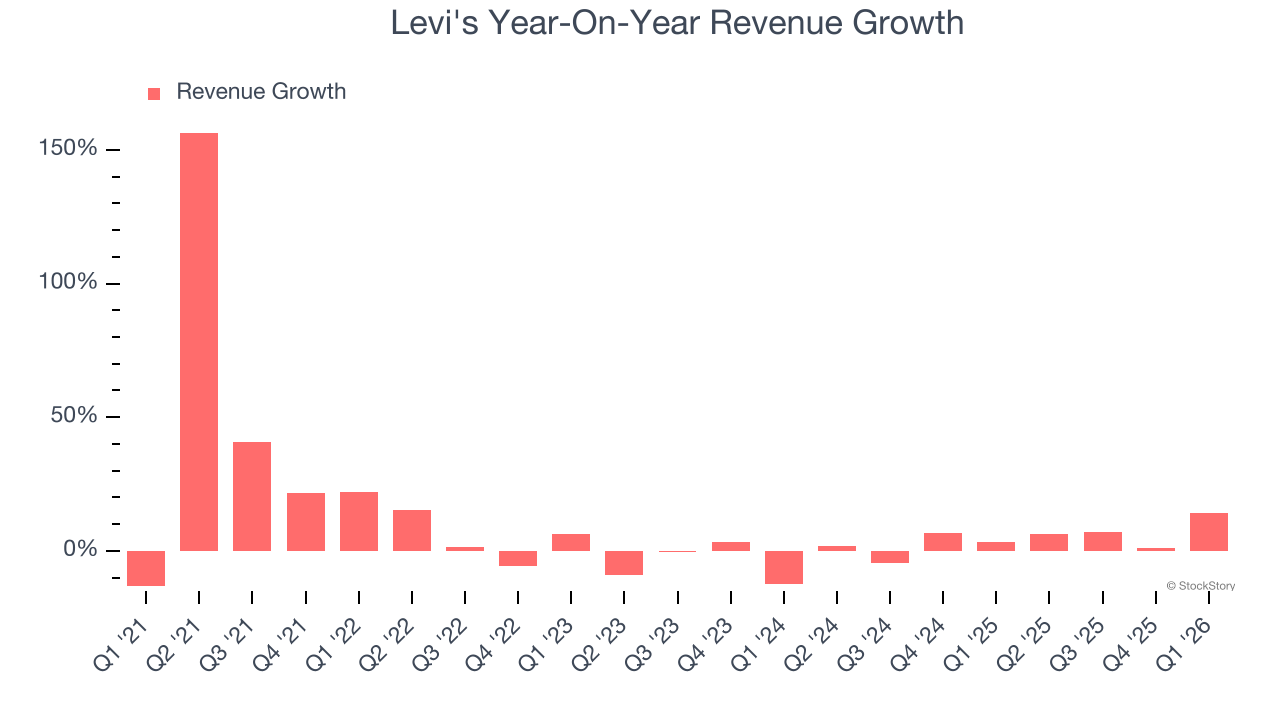

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Levi’s 8.9% annualized revenue growth over the last five years was weak. This fell short of our benchmark for the consumer discretionary sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Levi’s recent performance shows its demand has slowed as its annualized revenue growth of 4.3% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

Levi's also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 7.3% year-on-year growth. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for Levi's.

This quarter, Levi's reported year-on-year revenue growth of 14.1%, and its $1.74 billion of revenue exceeded Wall Street’s estimates by 5.6%.

Looking ahead, sell-side analysts expect revenue to grow 3.4% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its newer products and services will not catalyze better top-line performance yet.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Levi’s operating margin has risen over the last 12 months and averaged 9.1% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q1, Levi's generated an operating margin profit margin of 11.4%, down 1.1 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

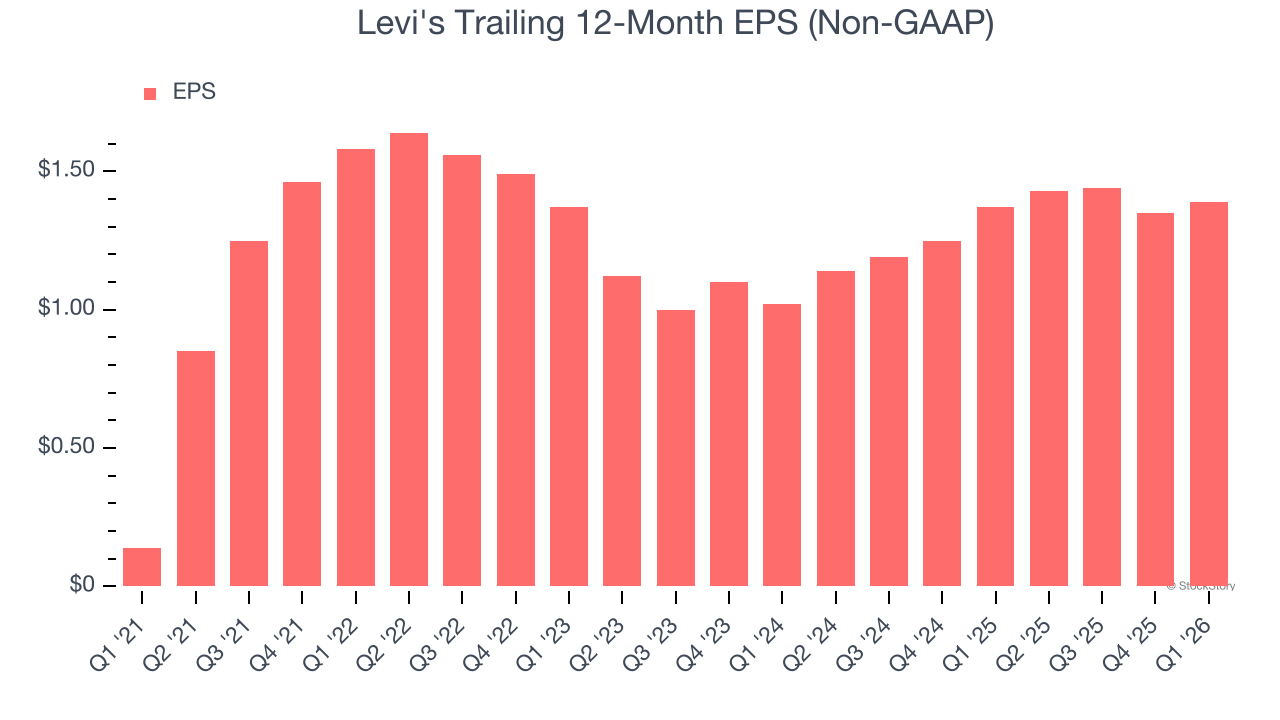

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Levi’s EPS grew at 58.3% compounded annual growth rate over the last five years, higher than its 8.9% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

In Q1, Levi's reported adjusted EPS of $0.42, up from $0.38 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Levi’s full-year EPS of $1.39 to grow 10.3%.

Key Takeaways from Levi’s Q1 Results

We enjoyed seeing Levi's beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance slightly missed. The market seems to be forgiving the minor guidance miss. Overall, this print had some key positives. The stock traded up 5.9% to $20.90 immediately after reporting.

Levi's had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).