Wrapping up Q4 earnings, we look at the numbers and key takeaways for the digital media & content platforms stocks, including IAC (NASDAQ: IAC) and its peers.

AI-driven content creation, personalized media experiences, and digital advertising are evolving, which could benefit companies investing in these themes. For example, companies with a portfolio of licensed visual content or platforms facilitating direct monetization models could see increased demand for years. On the other hand, headwinds include growing regulatory scrutiny on AI-generated content, with many publishers balking at anything that gets no human oversight. Additional areas to navigate include the phasing out of third-party cookies, which could make traditional ways of tracking the online behavior of consumers (a secret sauce in digital marketing) much less effective.

The 6 digital media & content platforms stocks we track reported a softer Q4. As a group, revenues beat analysts’ consensus estimates by 1.6% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 9% on average since the latest earnings results.

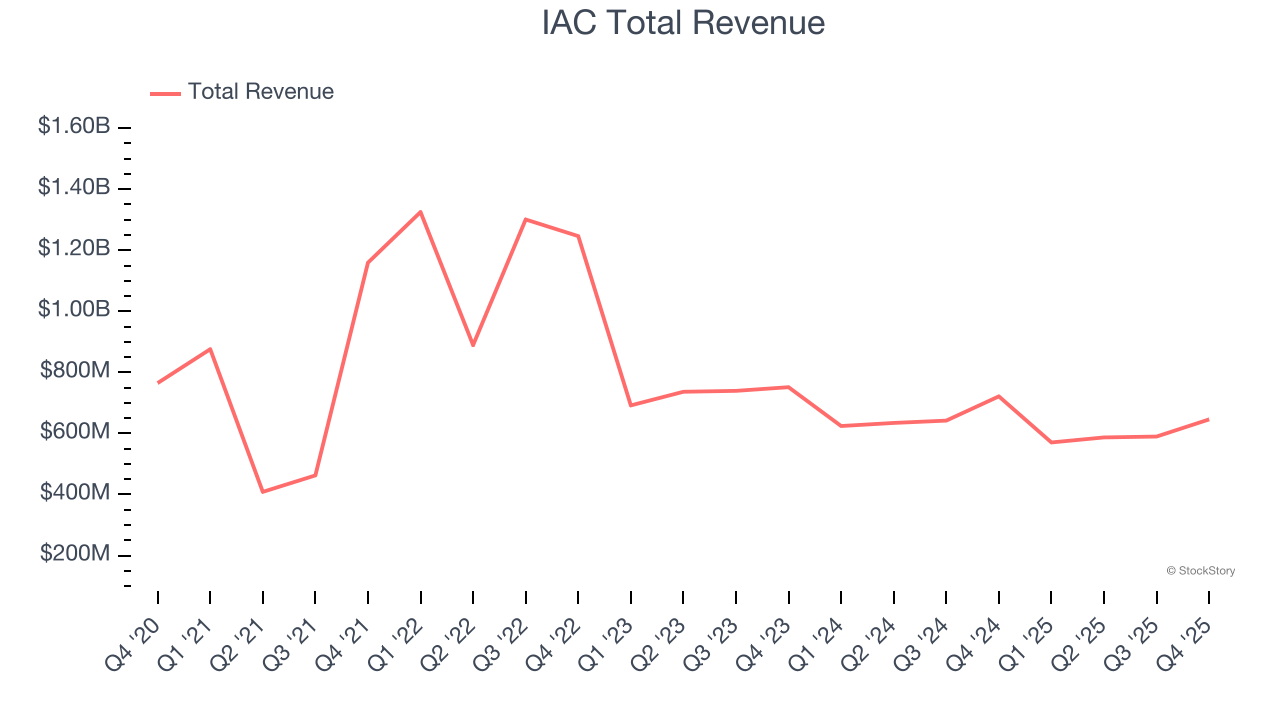

IAC (NASDAQ: IAC)

Originally known as InterActiveCorp and built through Barry Diller's strategic acquisitions since the 1990s, IAC (NASDAQ: IAC) operates a portfolio of category-leading digital businesses including Dotdash Meredith, Angi, and Care.com, focusing on digital publishing, home services, and caregiving platforms.

IAC reported revenues of $646 million, down 10.5% year on year. This print exceeded analysts’ expectations by 0.8%. Despite the top-line beat, it was still a softer quarter for the company with a significant miss of analysts’ EPS estimates.

IAC delivered the slowest revenue growth of the whole group. Interestingly, the stock is up 8.2% since reporting and currently trades at $39.81.

Read our full report on IAC here, it’s free.

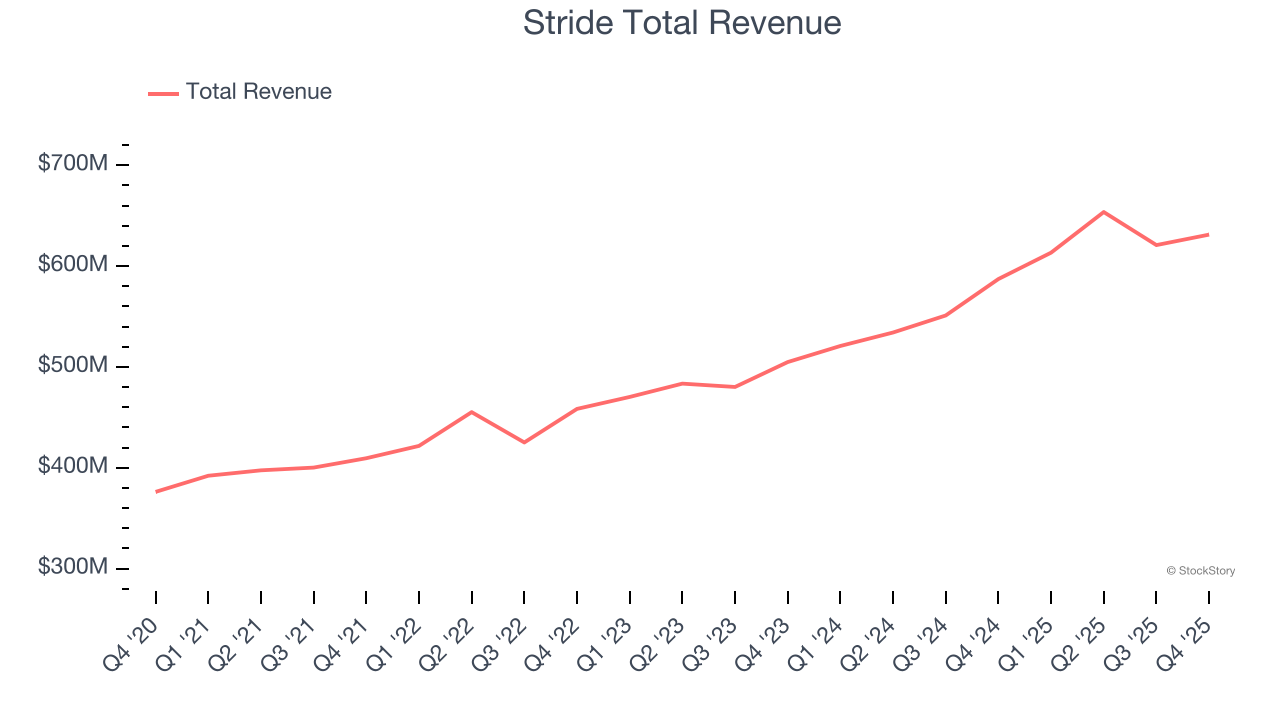

Best Q4: Stride (NYSE: LRN)

Formerly known as K12, Stride (NYSE: LRN) is an education technology company providing education solutions through digital platforms.

Stride reported revenues of $631.3 million, up 7.5% year on year, outperforming analysts’ expectations by 0.5%. The business had a very strong quarter with revenue guidance for next quarter exceeding analysts’ expectations and a beat of analysts’ EPS estimates.

The market seems happy with the results as the stock is up 23.6% since reporting. It currently trades at $89.54.

Is now the time to buy Stride? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: WEBTOON (NASDAQ: WBTN)

Pioneering a vertical-scrolling format optimized for mobile devices, WEBTOON Entertainment (NASDAQ: WBTN) operates a global platform where creators publish serialized web-comics and web-novels that users can read in bite-sized episodes.

WEBTOON reported revenues of $330.7 million, down 6.3% year on year, falling short of analysts’ expectations by 4.6%. It was a disappointing quarter as it posted revenue guidance for next quarter missing analysts’ expectations.

WEBTOON delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 15.5% since the results and currently trades at $9.74.

Read our full analysis of WEBTOON’s results here.

Ziff Davis (NASDAQ: ZD)

Originally a pioneering technology publisher founded in 1927 that became famous for PC Magazine, Ziff Davis (NASDAQ: ZD) operates a portfolio of digital media brands and subscription services across technology, shopping, gaming, healthcare, and cybersecurity markets.

Ziff Davis reported revenues of $406.7 million, down 1.5% year on year. This result missed analysts’ expectations by 1.9%. It was a disappointing quarter as it also produced a significant miss of analysts’ EPS and revenue estimates.

The stock is up 46.2% since reporting and currently trades at $43.19.

Read our full, actionable report on Ziff Davis here, it’s free.

Rumble (NASDAQ: RUM)

Founded in 2013 as a champion for content creator rights and free expression, Rumble (NASDAQ: RUM) is a video sharing platform that positions itself as a free speech alternative to mainstream platforms, offering creators more favorable revenue-sharing opportunities.

Rumble reported revenues of $27.07 million, down 10.5% year on year. This print met analysts’ expectations. However, it was a softer quarter as it logged a significant miss of analysts’ EPS estimates and revenue in line with analysts’ estimates.

The stock is down 11.5% since reporting and currently trades at $4.96.

Read our full, actionable report on Rumble here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.