ACV Auctions’s stock price has taken a beating over the past six months, shedding 57% of its value and falling to $4.36 per share. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy ACV Auctions, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is ACV Auctions Not Exciting?

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons there are better opportunities than ACVA and a stock we'd rather own.

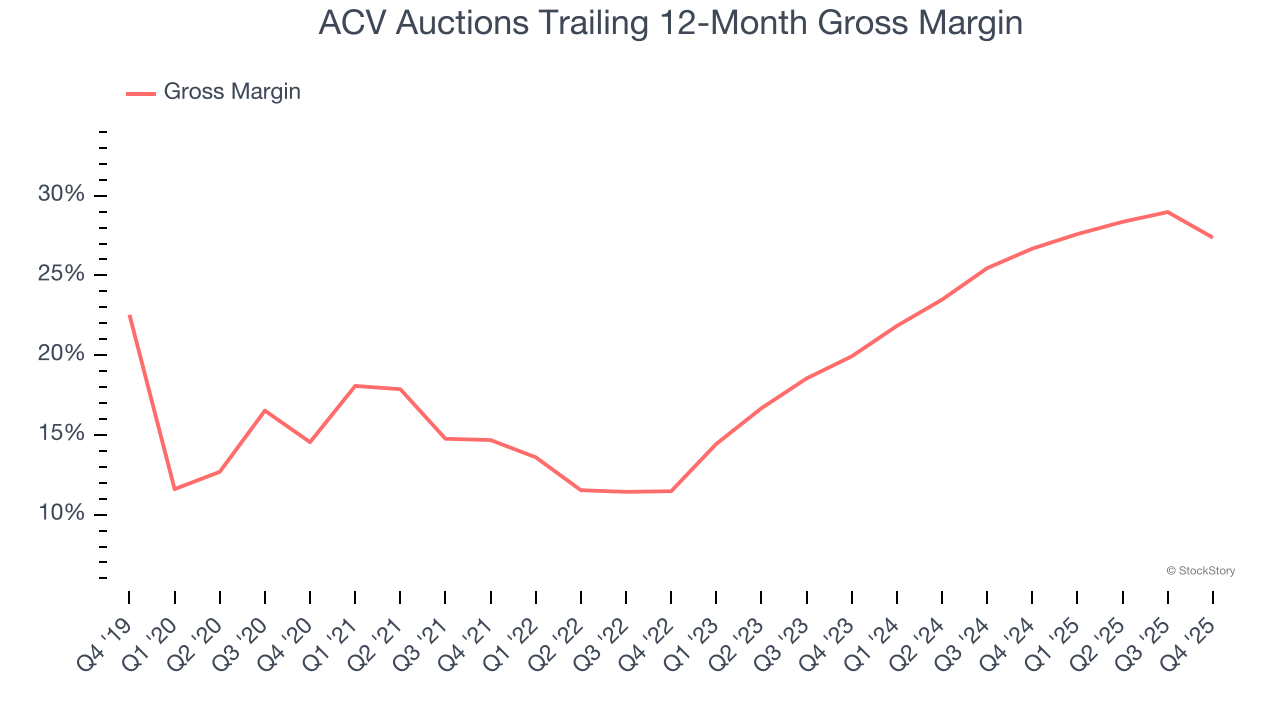

1. Low Gross Margin Reveals Weak Structural Profitability

For online marketplaces like ACV Auctions, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification.

ACV Auctions’s unit economics are far below other consumer internet companies, signaling it operates in a competitive market and must pay many third parties a slice of its sales to distribute its products and services. As you can see below, it averaged a 27.1% gross margin over the last two years. That means ACV Auctions paid its providers a lot of money ($72.94 for every $100 in revenue) to run its business.

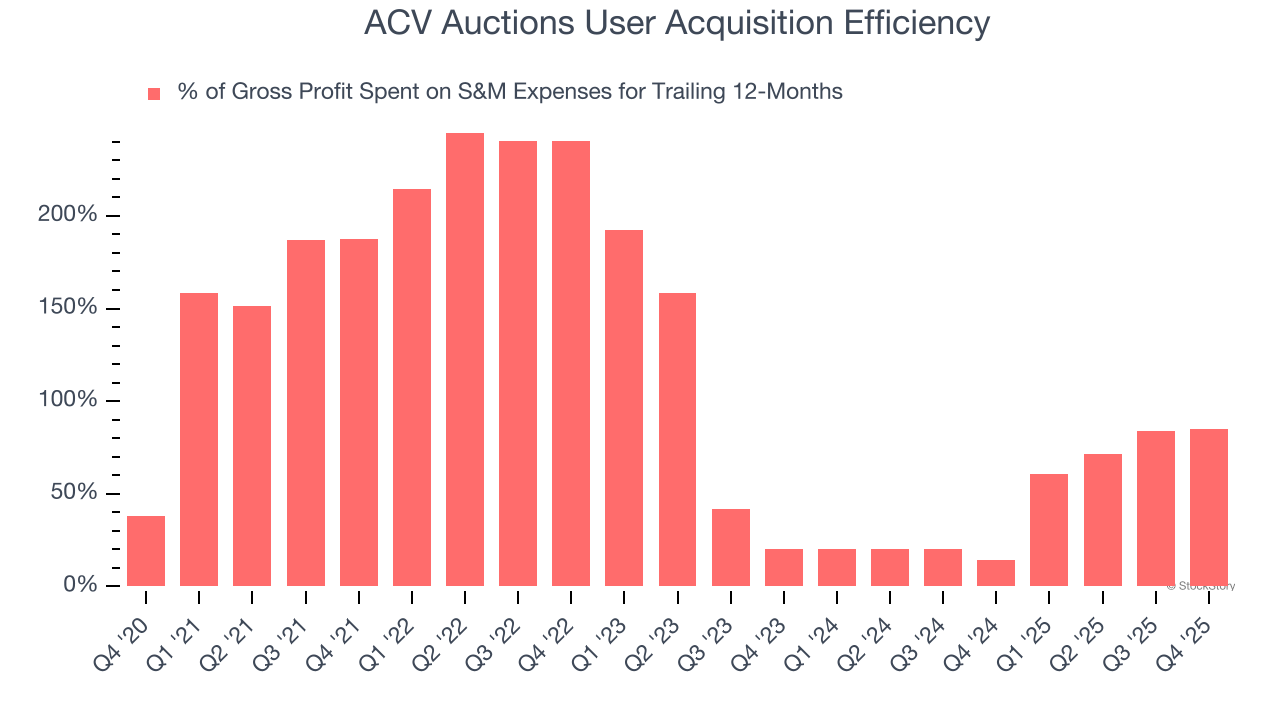

2. Poor Marketing Efficiency Drains Profits

Consumer internet businesses like ACV Auctions grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

It’s very expensive for ACV Auctions to acquire new users as the company has spent 84.7% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates a highly competitive environment with little differentiation between ACV Auctions and its peers.

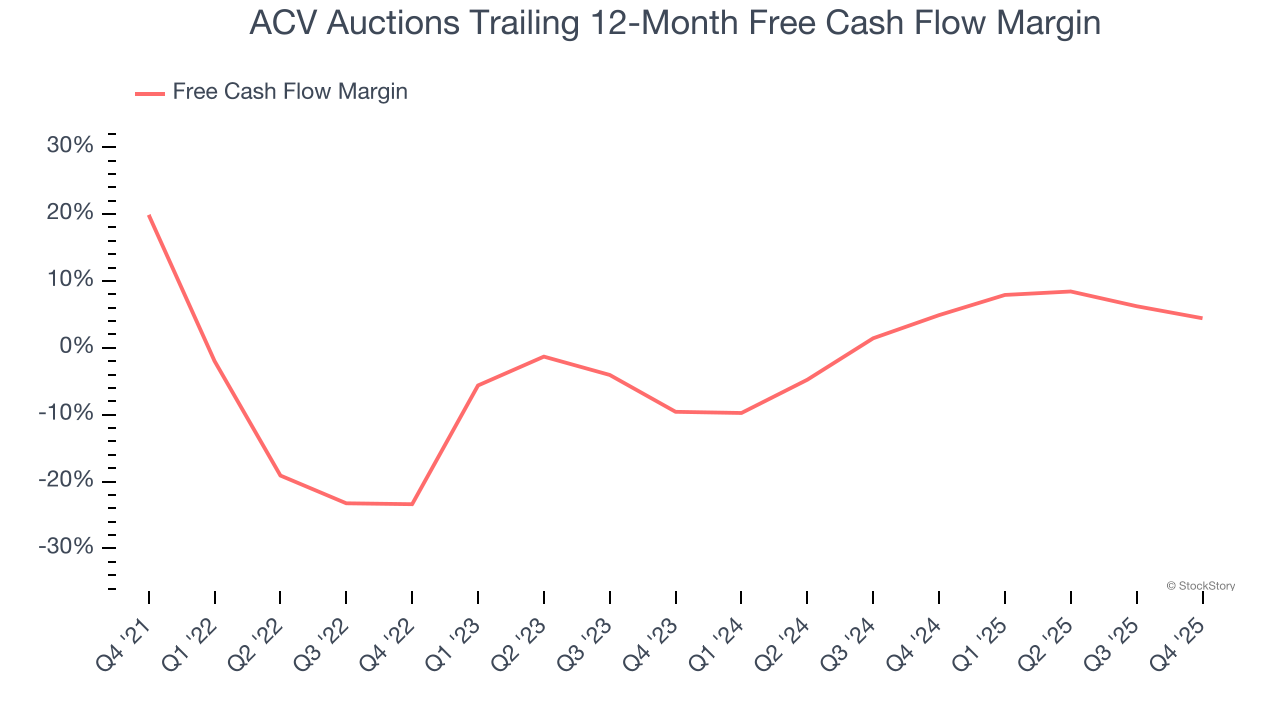

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

ACV Auctions has shown mediocre cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 4.6%, below what we’d expect for a consumer internet business.

Final Judgment

ACV Auctions isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 8.9× forward EV/EBITDA (or $4.36 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of ACV Auctions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.