As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q4. Today, we are looking at U.S. shale E&P stocks, starting with Matador Resources (NYSE: MTDR).

US shale oil producers extract crude from tight rock formations using horizontal drilling and hydraulic fracturing (fracking) techniques, primarily in basins like the Permian, Bakken, and Eagle Ford. Tailwinds include short-cycle investment flexibility allowing rapid production adjustments, technological improvements enhancing well productivity, and proximity to refining and export infrastructure. Capital discipline has improved financial returns. Headwinds include commodity price sensitivity affecting drilling economics, accelerating well decline rates requiring continuous capital investment, and increasing regulatory and ESG scrutiny. Water usage, induced seismicity concerns, and evolving environmental regulations present ongoing operational challenges.

The 11 U.S. shale E&P stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 2.2%.

Luckily, u.s. shale e&p stocks have performed well with share prices up 12.9% on average since the latest earnings results.

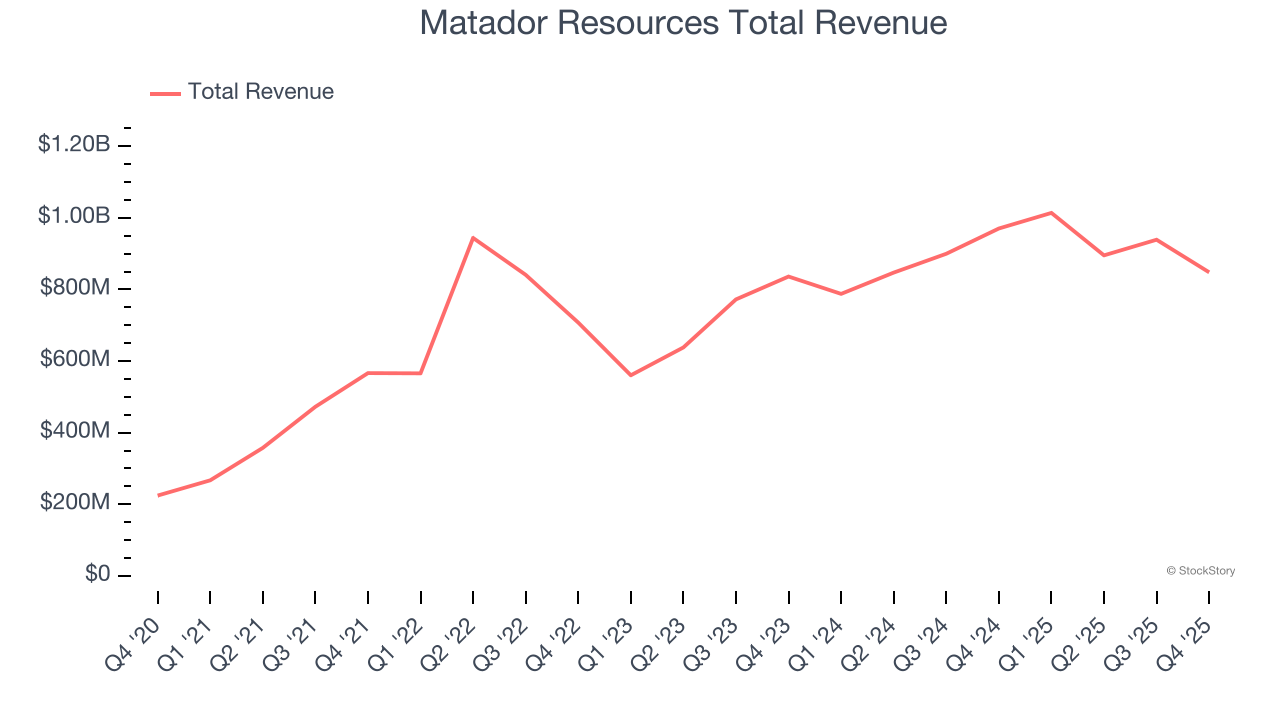

Best Q4: Matador Resources (NYSE: MTDR)

Operating primarily in the Delaware Basin where multiple oil-bearing layers lie stacked thousands of feet deep, Matador Resources (NYSE: MTDR) explores for, drills, and produces oil and natural gas from underground rock formations in New Mexico and Texas.

Matador Resources reported revenues of $848 million, down 12.6% year on year. This print exceeded analysts’ expectations by 4.7%. Overall, it was a stunning quarter for the company with an impressive beat of analysts’ EBITDA and EPS estimates.

Interestingly, the stock is up 21.3% since reporting and currently trades at $61.30.

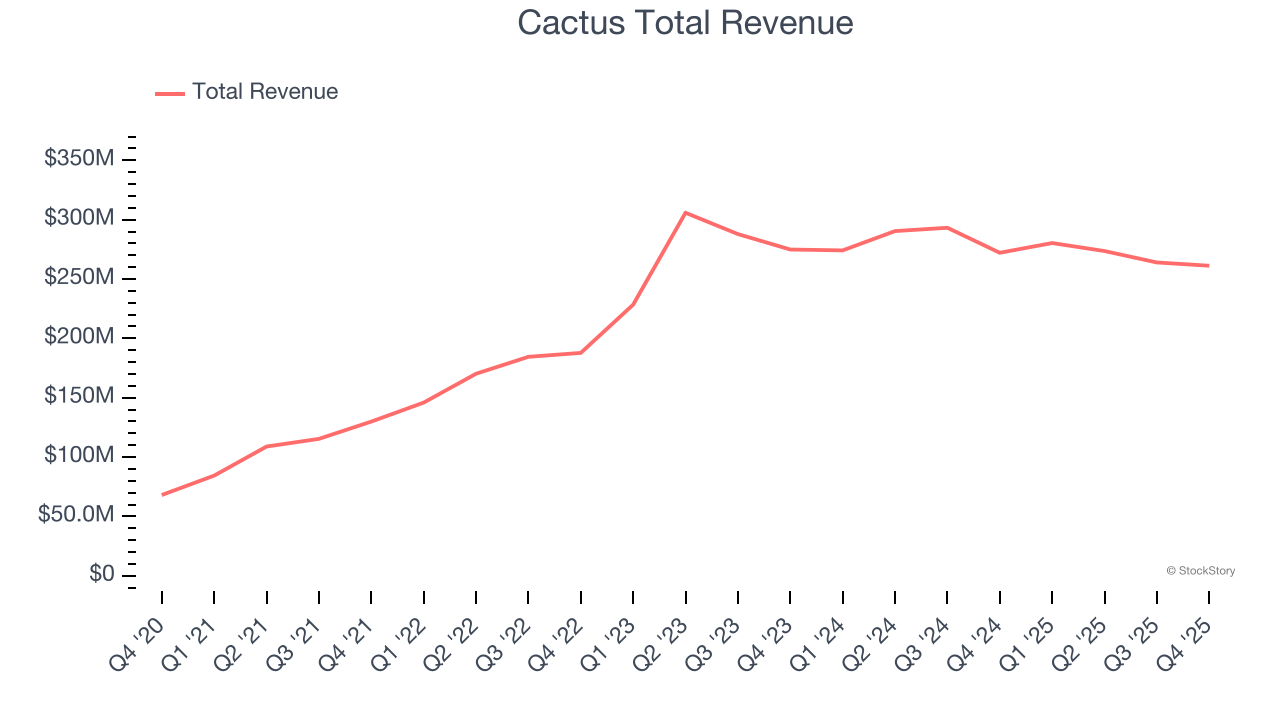

Cactus (NYSE: WHD)

Named for the spiky wellhead equipment that reminded founders of desert cacti, Cactus (NYSE: WHD) manufactures wellheads, valves, and spoolable pipes used in drilling and producing oil and gas wells.

Cactus reported revenues of $261.2 million, down 4% year on year, outperforming analysts’ expectations by 3.4%. The business had an exceptional quarter with a beat of analysts’ EPS and EBITDA estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 4.5% since reporting. It currently trades at $55.39.

Is now the time to buy Cactus? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: HighPeak Energy (NASDAQ: HPK)

Operating in the oil-rich northeastern corner of the Midland Basin where Howard and Borden counties meet, HighPeak Energy (NASDAQ: HPK) explores for, develops, and produces crude oil, natural gas liquids, and natural gas.

HighPeak Energy reported revenues of $216.6 million, down 23.3% year on year, exceeding analysts’ expectations by 13.7%. Still, it was a softer quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

HighPeak Energy delivered the biggest analyst estimates beat but had the slowest revenue growth in the group. Interestingly, the stock is up 8.8% since the results and currently trades at $6.37.

Read our full analysis of HighPeak Energy’s results here.

Texas Pacific Land (NYSE: TPL)

One of America's largest private landowners with roughly 868,000 acres in the Permian Basin, Texas Pacific Land (NYSE: TPL) owns land in West Texas and earns revenue from oil and gas royalties, water services, and land leases.

Texas Pacific Land reported revenues of $211.6 million, up 13.9% year on year. This print surpassed analysts’ expectations by 2.4%. Zooming out, it was a mixed quarter as it also produced a decent beat of analysts’ EBITDA estimates but a significant miss of analysts’ EPS estimates.

The stock is flat since reporting and currently trades at $437.50.

Read our full, actionable report on Texas Pacific Land here, it’s free.

Chord Energy (NASDAQ: CHRD)

Holding the largest acreage position in the Williston Basin, Chord Energy (NASDAQ: CHRD) drills for and produces crude oil, natural gas liquids, and natural gas in North Dakota's Williston Basin.

Chord Energy reported revenues of $1.17 billion, down 19.6% year on year. This result topped analysts’ expectations by 7%. It was a strong quarter as it also produced a decent beat of analysts’ EBITDA and EPS estimates.

The stock is up 32.5% since reporting and currently trades at $137.41.

Read our full, actionable report on Chord Energy here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.