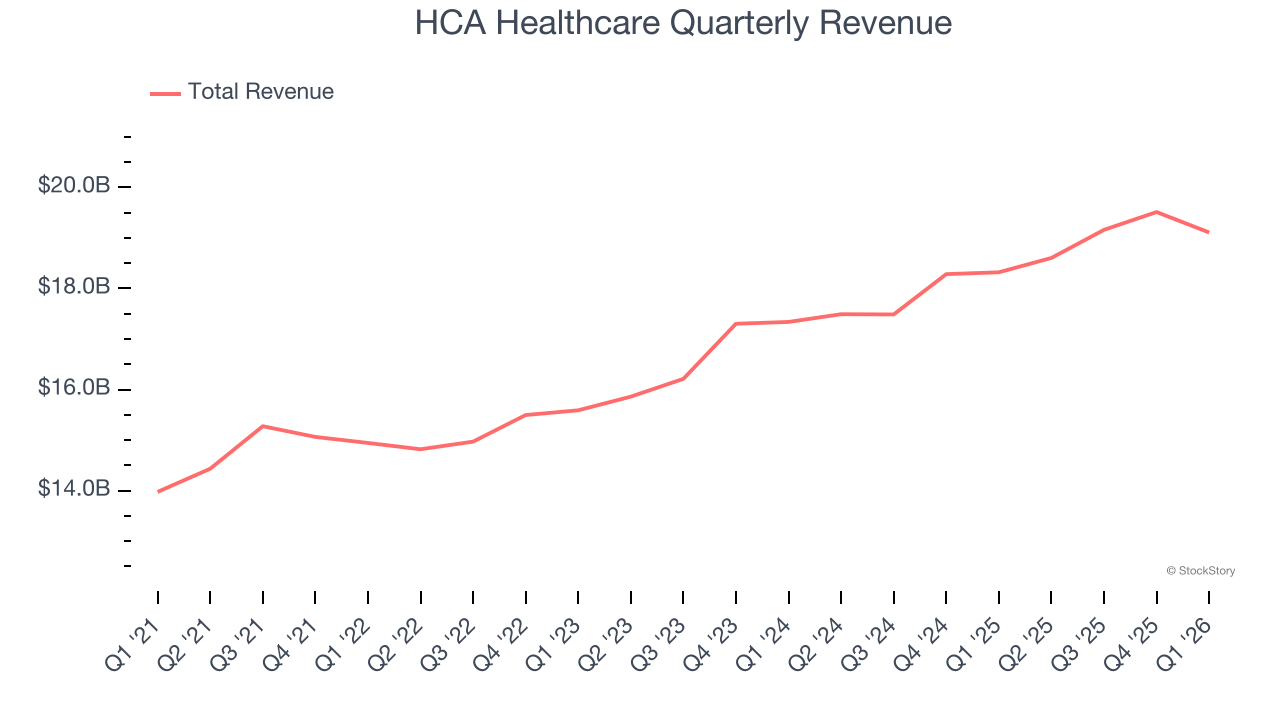

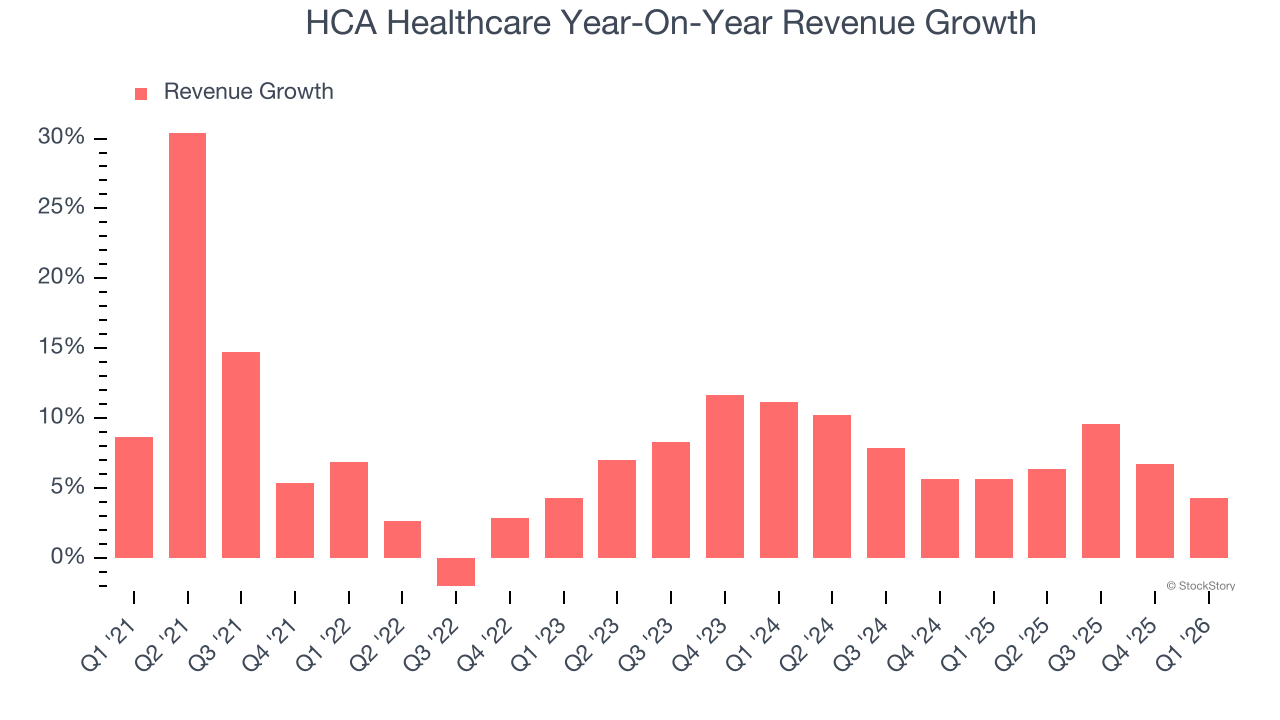

Hospital operator HCA Healthcare (NYSE: HCA) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 4.3% year on year to $19.11 billion. Its non-GAAP profit of $7.15 per share was in line with analysts’ consensus estimates.

Is now the time to buy HCA Healthcare? Find out by accessing our full research report, it’s free.

HCA Healthcare (HCA) Q1 CY2026 Highlights:

- Revenue: $19.11 billion vs analyst estimates of $19.08 billion (4.3% year-on-year growth, in line)

- Adjusted EPS: $7.15 vs analyst estimates of $7.15 (in line)

- Adjusted EBITDA: $3.8 billion vs analyst estimates of $3.85 billion (19.9% margin, 1.4% miss)

- Operating Margin: 19.8%, up from 15.7% in the same quarter last year

- Free Cash Flow Margin: 4.7%, up from 3.6% in the same quarter last year

- Market Capitalization: $106 billion

"The start of the year presented a dynamic environment for HCA Healthcare. I want to recognize our colleagues for continuing to demonstrate a remarkable ability to adapt to changing conditions and deliver for our patients, communities, and stakeholders,” said Sam Hazen, Chief Executive Officer of HCA Healthcare.

Company Overview

With roots dating back to 1968 and a network spanning 20 states, HCA Healthcare (NYSE: HCA) operates a network of 190 hospitals and 150+ outpatient facilities providing a full range of medical services across the US and England.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, HCA Healthcare’s 7.7% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. HCA Healthcare’s annualized revenue growth of 7% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, HCA Healthcare grew its revenue by 4.3% year on year, and its $19.11 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

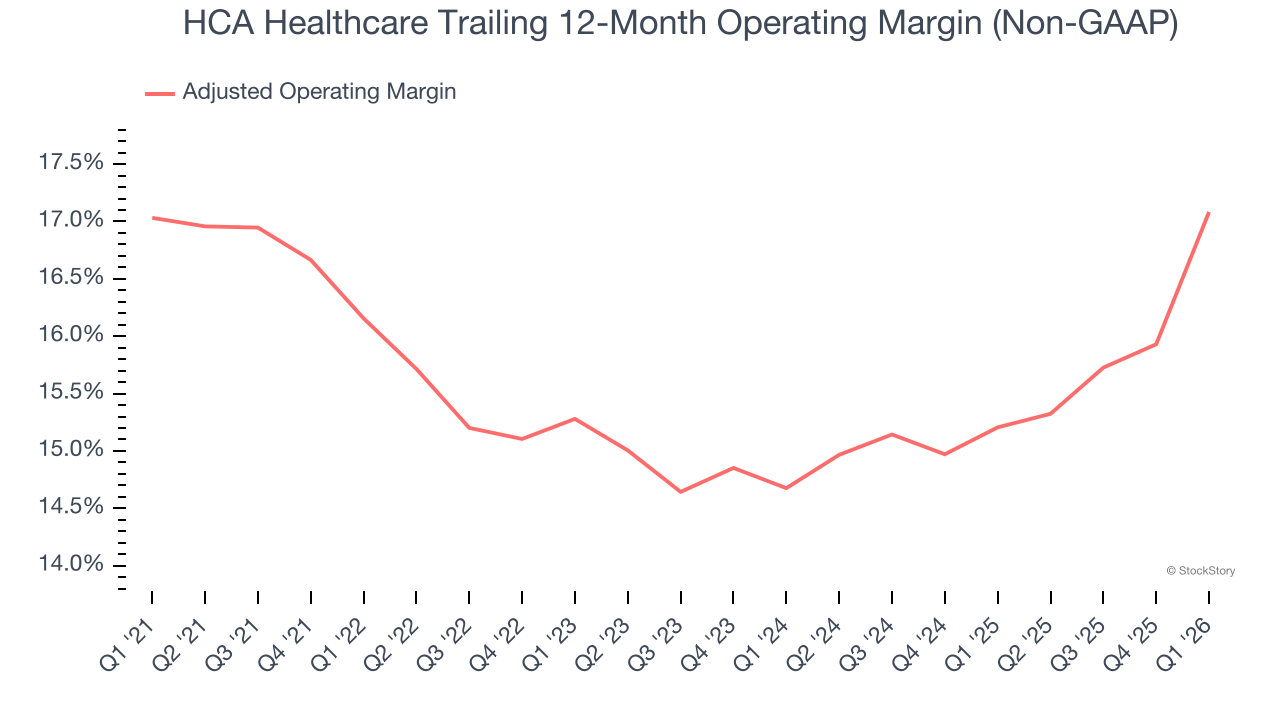

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

HCA Healthcare’s adjusted operating margin has risen over the last 12 months and averaged 15.7% over the last five years. Its solid profitability for a healthcare business shows it’s an efficient company that manages its expenses effectively.

Analyzing the trend in its profitability, HCA Healthcare’s adjusted operating margin of 17.1% for the trailing 12 months may be around the same as five years ago, but it has increased by 2.4 percentage points over the last two years. This dynamic unfolded because its sales growth gave it operating leverage and shows it has some momentum on its side.

This quarter, HCA Healthcare generated an adjusted operating margin profit margin of 20.3%, up 4.6 percentage points year on year. This increase was a welcome development and shows it was more efficient.

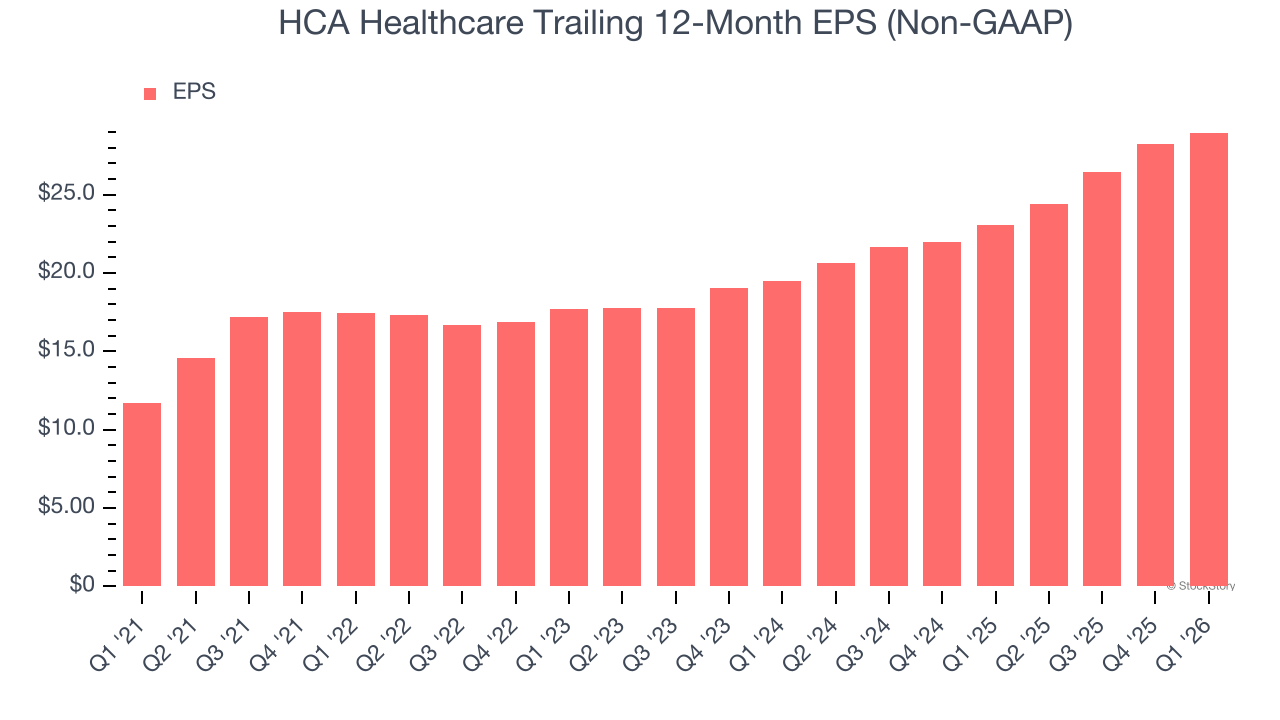

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

HCA Healthcare’s EPS grew at 19.9% compounded annual growth rate over the last five years, higher than its 7.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

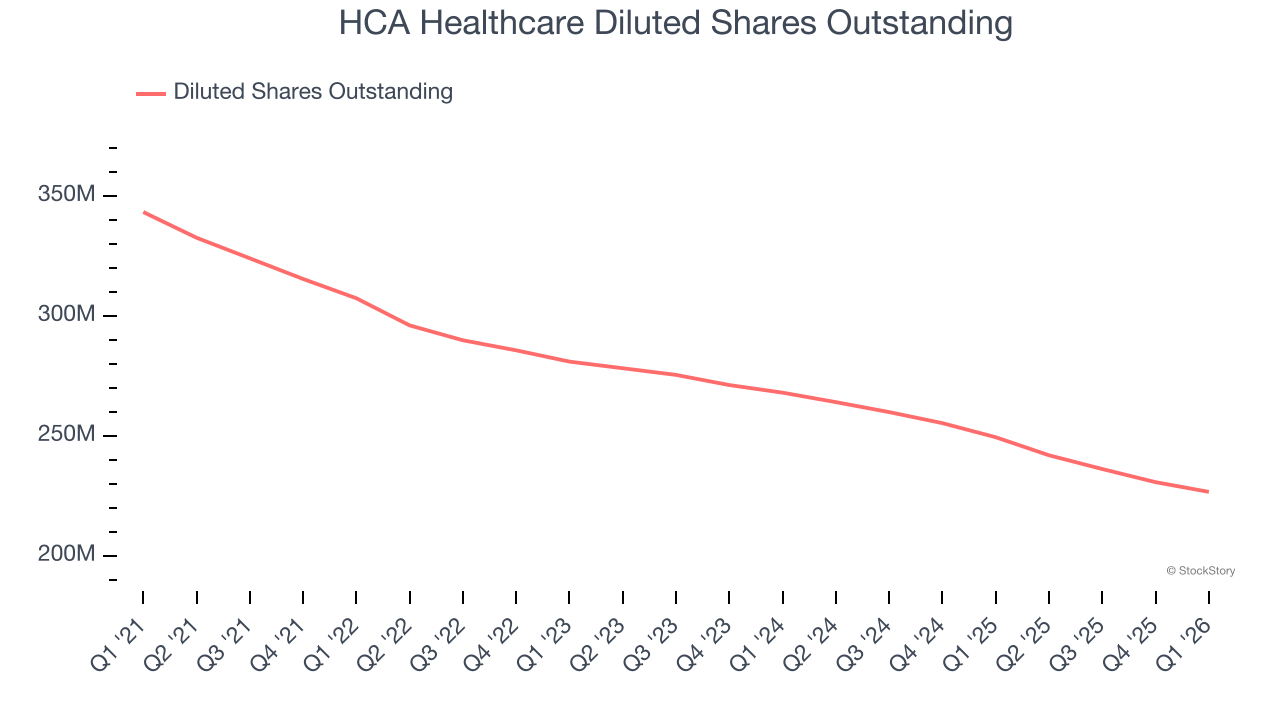

Diving into the nuances of HCA Healthcare’s earnings can give us a better understanding of its performance. A five-year view shows that HCA Healthcare has repurchased its stock, shrinking its share count by 34%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, HCA Healthcare reported adjusted EPS of $7.15, up from $6.45 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects HCA Healthcare’s full-year EPS of $28.96 to grow 7.2%.

Key Takeaways from HCA Healthcare’s Q1 Results

Revenue and EPS were just in line. On the negative side, adjusted EBITDA missed. The market seemed to be hoping for more, and the stock traded down 6.7% to $442.50 immediately following the results.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).