Financial services company The Bancorp (NASDAQ: TBBK) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 8% year on year to $161.3 million. Its GAAP profit of $1.41 per share was 5.5% above analysts’ consensus estimates.

Is now the time to buy The Bancorp? Find out by accessing our full research report, it’s free.

The Bancorp (TBBK) Q1 CY2026 Highlights:

- Net Interest Income: $88.81 million vs analyst estimates of $91.51 million (3.2% year-on-year decline, 2.9% miss)

- Net Interest Margin: 3.9% vs analyst estimates of 4.2% (32.3 basis point miss)

- Revenue: $161.3 million vs analyst estimates of $195.3 million (8% year-on-year decline, 17.4% miss)

- Efficiency Ratio: 41.5% vs analyst estimates of 37.7% (380 basis point miss)

- EPS (GAAP): $1.41 vs analyst estimates of $1.34 (5.5% beat)

- Tangible Book Value per Share: $16.65 vs analyst estimates of $16.87 (5.6% year-on-year decline, 1.3% miss)

- Market Capitalization: $2.52 billion

Company Overview

Operating behind the scenes of many popular fintech apps and prepaid cards you might use daily, The Bancorp (NASDAQ: TBBK) is a bank holding company that specializes in providing banking services to fintech companies and offering specialty lending products.

Sales Growth

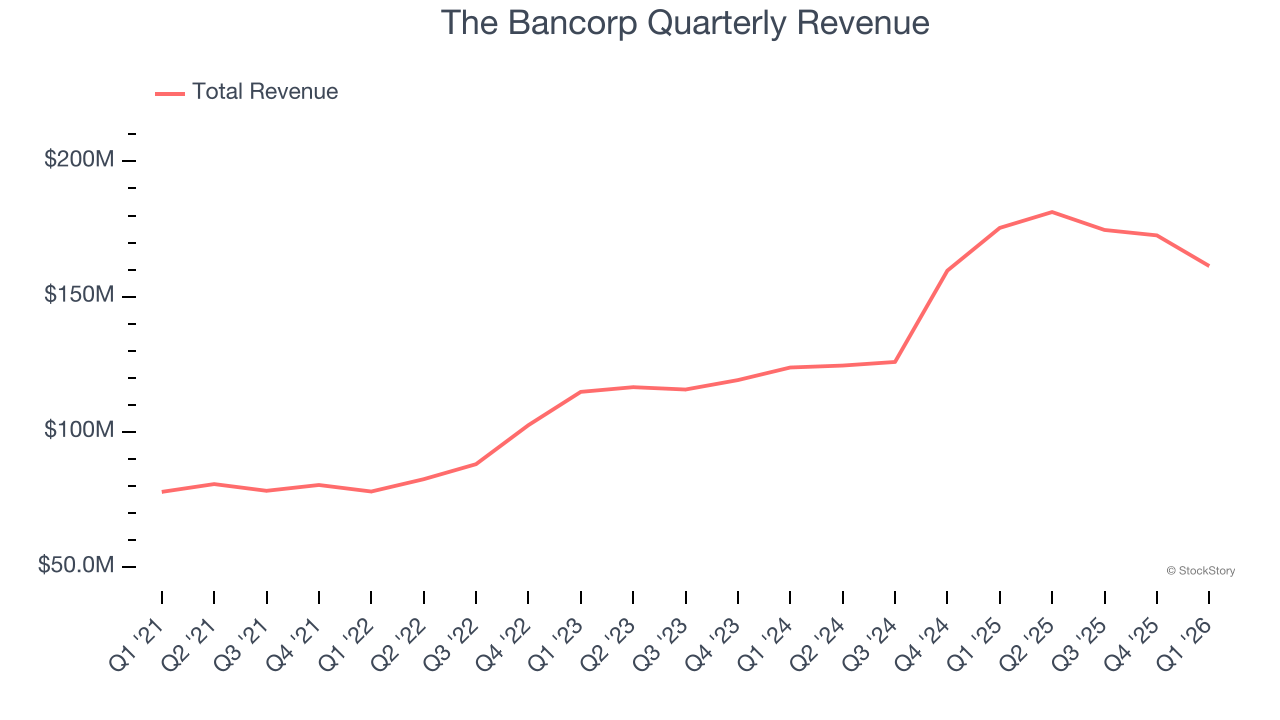

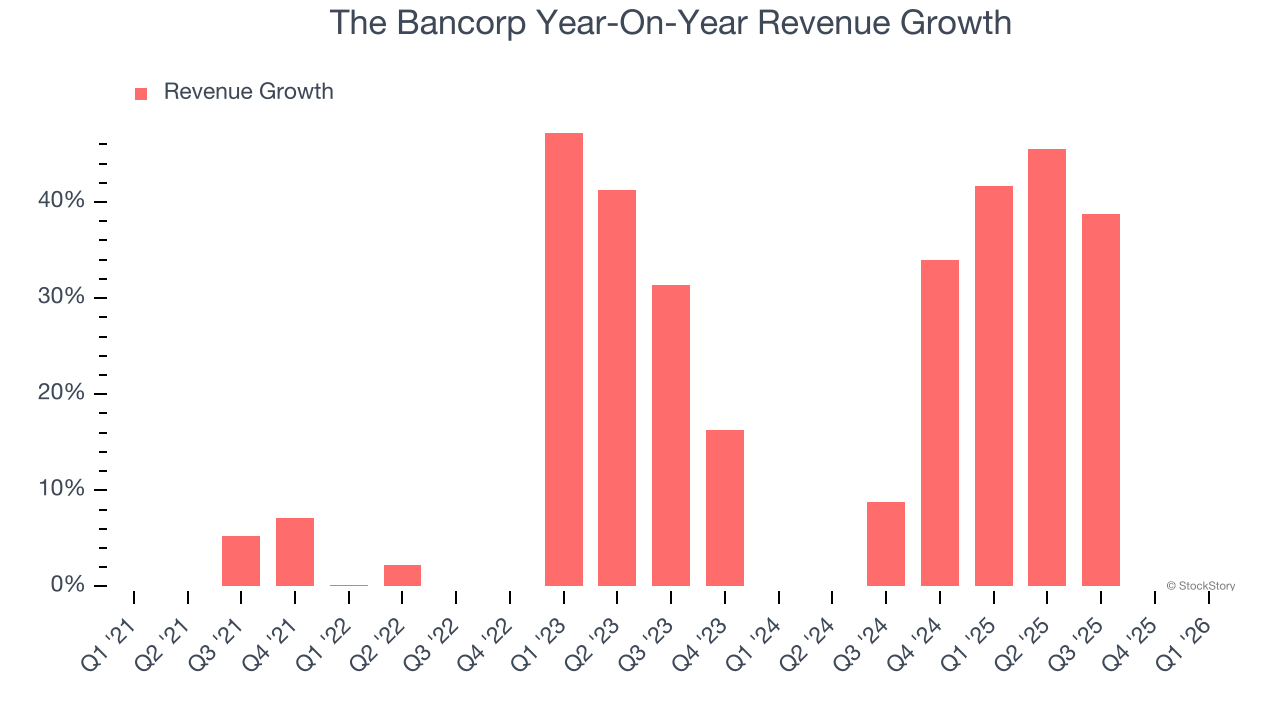

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income. Thankfully, The Bancorp’s 18.3% annualized revenue growth over the last five years was exceptional. Its growth surpassed the average banking company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. The Bancorp’s annualized revenue growth of 20.5% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, The Bancorp missed Wall Street’s estimates and reported a rather uninspiring 8% year-on-year revenue decline, generating $161.3 million of revenue.

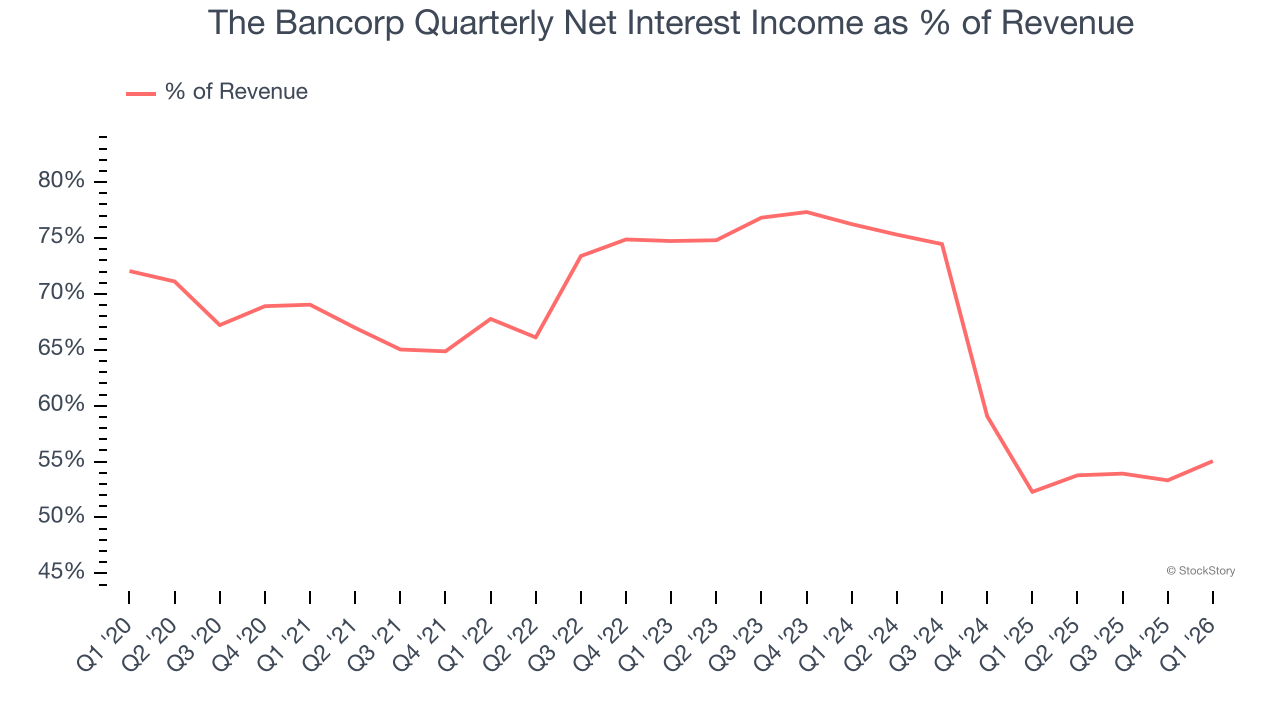

Net interest income made up 66.8% of the company’s total revenue during the last five years, meaning lending operations are The Bancorp’s largest source of revenue.

While banks generate revenue from multiple sources, investors view net interest income as the cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of non-interest income.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

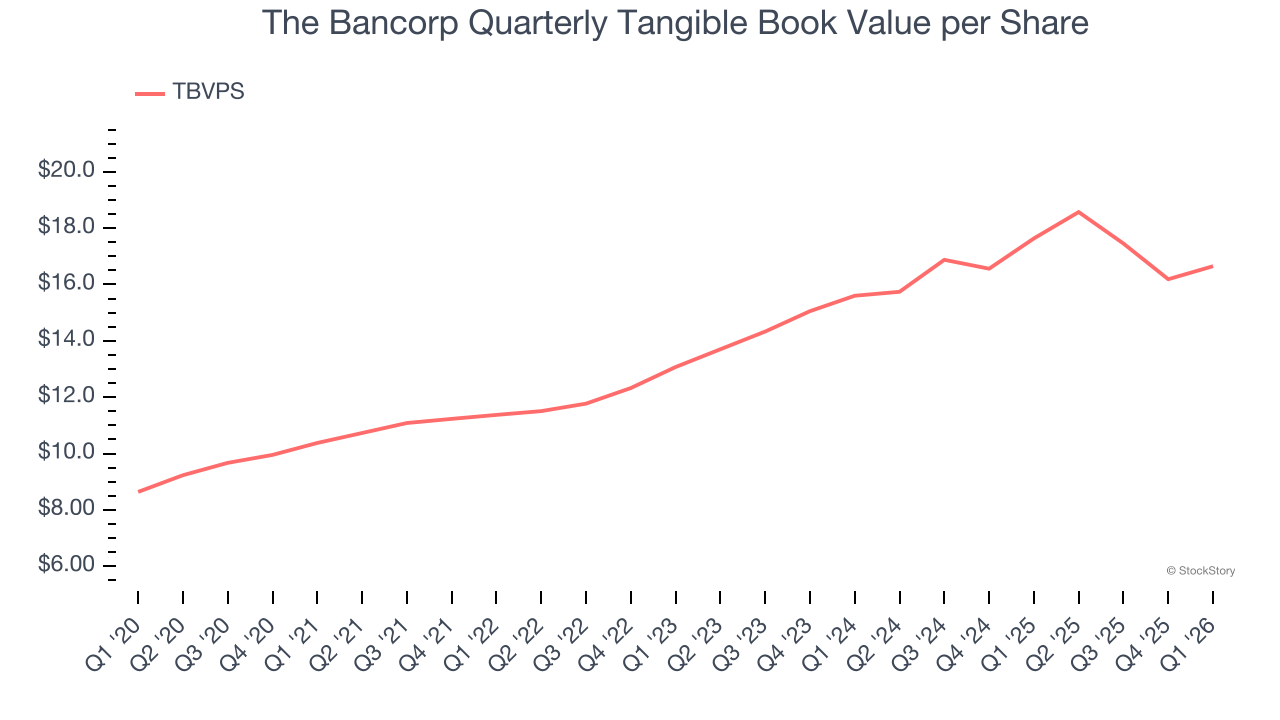

Tangible Book Value Per Share (TBVPS)

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

This explains why tangible book value per share (TBVPS) stands as the premier banking metric. TBVPS strips away questionable intangible assets, revealing concrete per-share net worth that investors can trust. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

The Bancorp’s TBVPS grew at an exceptional 9.9% annual clip over the last five years. However, TBVPS growth has recently decelerated to 3.3% annual growth over the last two years (from $15.60 to $16.65 per share).

Over the next 12 months, Consensus estimates call for The Bancorp’s TBVPS to grow by 17% to $19.47, solid growth rate.

Key Takeaways from The Bancorp’s Q1 Results

The Bancorp's revenue missed and its net interest income fell short of Wall Street’s estimates. On the other hand, EPS beat. Overall, this was a mixed quarter. The stock remained flat at $60.46 immediately following the results.

The Bancorp may have had a tough quarter, but does that actually create an opportunity to invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).