Student loan provider Sallie Mae (NASDAQ: SLM) announced better-than-expected revenue in Q1 CY2026, but sales fell by 3.6% year on year to $560 million. Its GAAP profit of $1.54 per share was 26.1% above analysts’ consensus estimates.

Is now the time to buy Sallie Mae? Find out by accessing our full research report, it’s free.

Sallie Mae (SLM) Q1 CY2026 Highlights:

- Net Interest Income: $375.4 million vs analyst estimates of $356.9 million

- Revenue: $560 million vs analyst estimates of $538.7 million (3.6% year-on-year decline, 3.9% beat)

- Pre-tax Profit: $400.4 million (71.5% margin)

- EPS (GAAP): $1.54 vs analyst estimates of $1.22 (26.1% beat)

- EPS (GAAP) guidance for the full year is $3.15 at the midpoint, beating analyst estimates by 13.4%

- Market Capitalization: $4.58 billion

Company Overview

Originally created as a government-sponsored enterprise before privatizing in 2004, Sallie Mae (NASDAQ: SLM) is a financial services company that provides private education loans, savings products, and educational resources to help students and families pay for college.

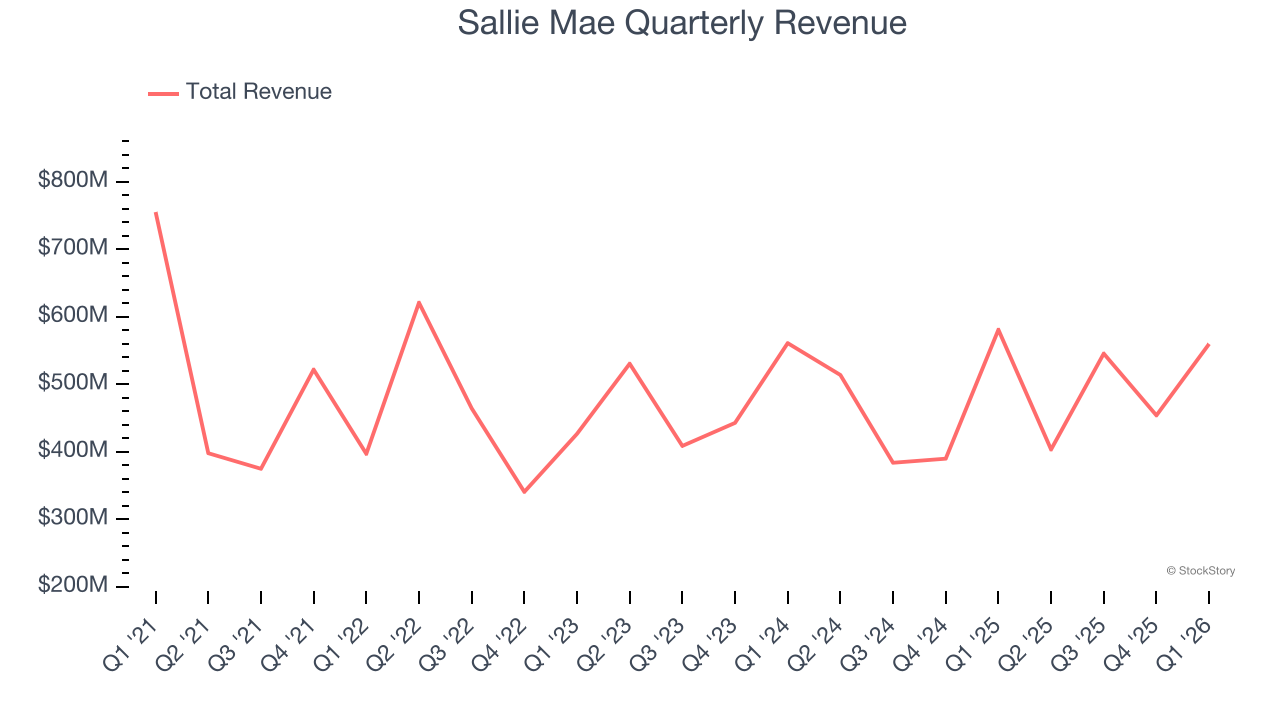

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Sallie Mae struggled to consistently increase demand as its $1.96 billion of revenue for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of lacking business quality.

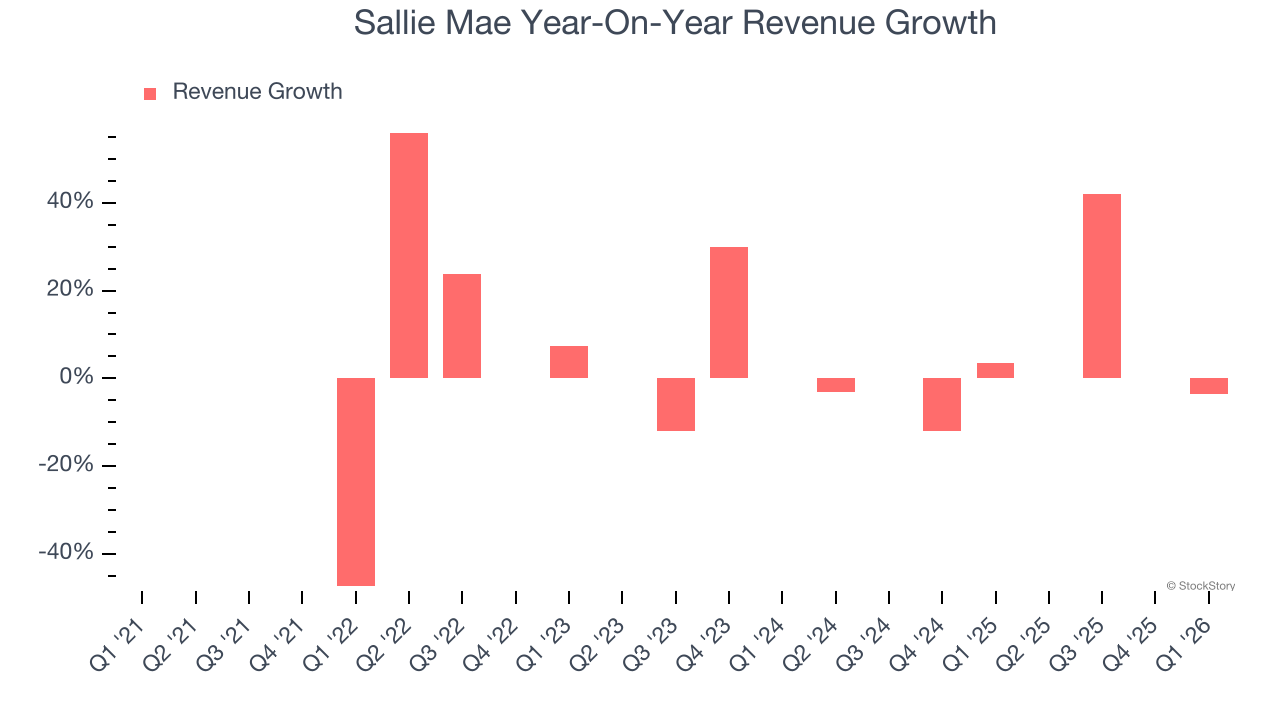

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Just like its five-year trend, Sallie Mae’s revenue over the last two years was flat, suggesting it is in a slump.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Sallie Mae’s revenue fell by 3.6% year on year to $560 million but beat Wall Street’s estimates by 3.9%.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Key Takeaways from Sallie Mae’s Q1 Results

It was good to see Sallie Mae beat analysts’ EPS expectations this quarter. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 1.8% to $23.85 immediately following the results.

Sure, Sallie Mae had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).