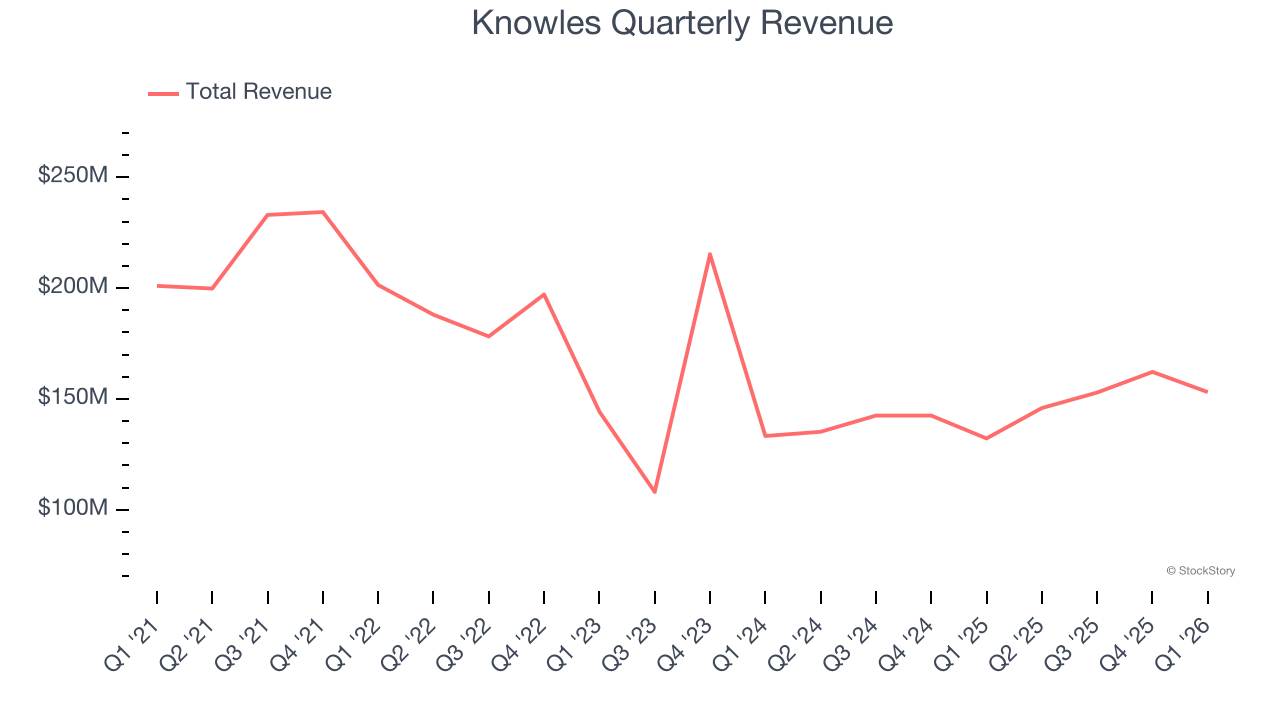

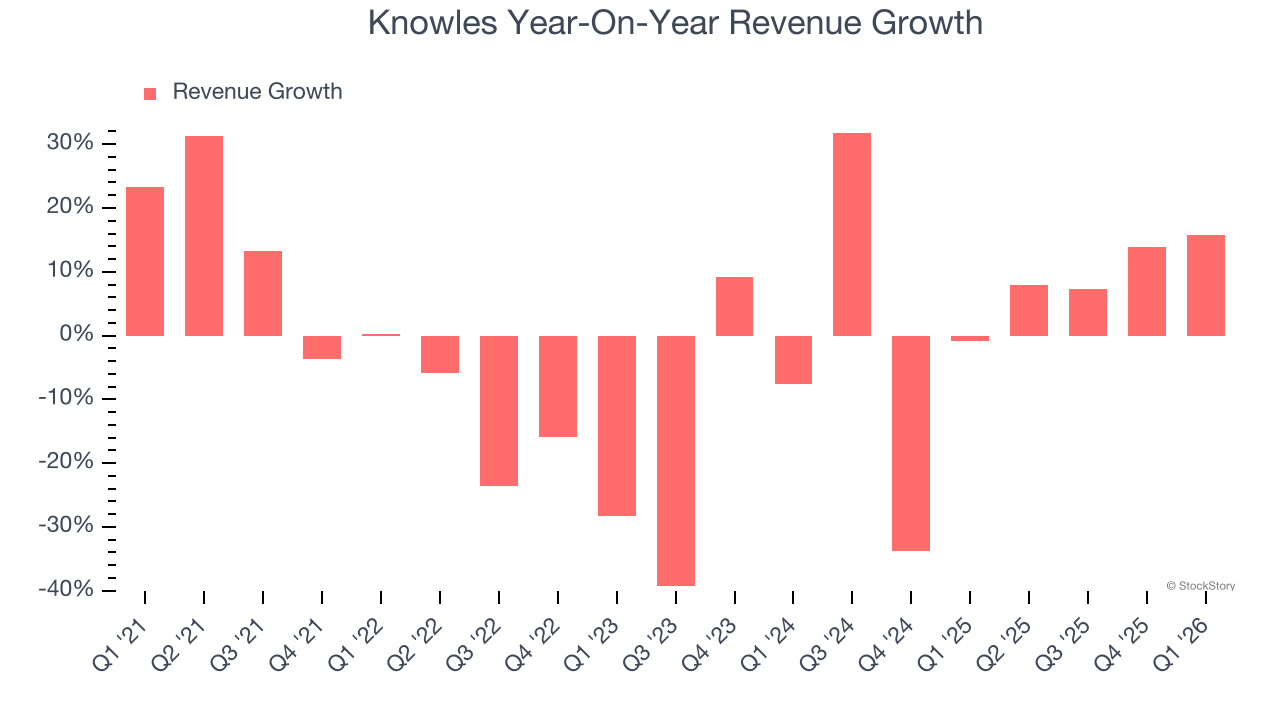

Electronic components manufacturer Knowles (NYSE: KN) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 15.8% year on year to $153.1 million. Guidance for next quarter’s revenue was optimistic at $157 million at the midpoint, 2.3% above analysts’ estimates. Its non-GAAP profit of $0.27 per share was 13.7% above analysts’ consensus estimates.

Is now the time to buy Knowles? Find out by accessing our full research report, it’s free.

Knowles (KN) Q1 CY2026 Highlights:

- Revenue: $153.1 million vs analyst estimates of $147.4 million (15.8% year-on-year growth, 3.9% beat)

- Adjusted EPS: $0.27 vs analyst estimates of $0.24 (13.7% beat)

- Adjusted EBITDA: $35.3 million vs analyst estimates of $30.7 million (23.1% margin, 15% beat)

- Revenue Guidance for Q2 CY2026 is $157 million at the midpoint, above analyst estimates of $153.5 million

- Adjusted EPS guidance for Q2 CY2026 is $0.30 at the midpoint, above analyst estimates of $0.30

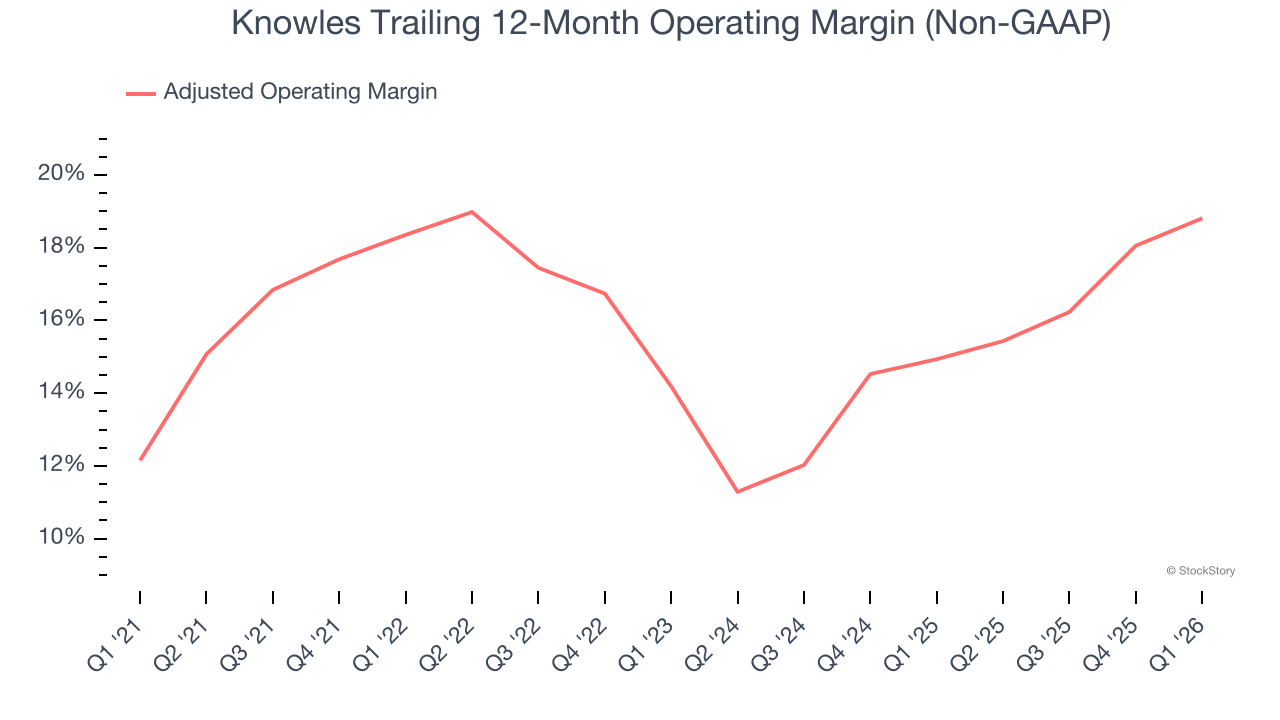

- Operating Margin: 10.4%, up from 5.8% in the same quarter last year

- Free Cash Flow was -$3.1 million, down from $18.3 million in the same quarter last year

- Market Capitalization: $2.61 billion

“We started 2026 delivering strong first quarter revenues and non-GAAP diluted EPS which was at or above the high-end of our guided ranges,” commented Jeffrey Niew, President and CEO of Knowles.

Company Overview

With roots dating back to 1946 and a focus on components that must perform flawlessly in critical situations, Knowles (NYSE: KN) designs and manufactures specialized electronic components like high-performance capacitors, microphones, and speakers for medical technology, defense, and industrial applications.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $614.1 million in revenue over the past 12 months, Knowles is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels.

As you can see below, Knowles’s revenue declined by 5.2% per year over the last five years, a rough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Knowles’s annualized revenue growth of 1.3% over the last two years is above its five-year trend, which is encouraging.

This quarter, Knowles reported year-on-year revenue growth of 15.8%, and its $153.1 million of revenue exceeded Wall Street’s estimates by 3.9%. Company management is currently guiding for a 7.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Adjusted Operating Margin

Knowles’s adjusted operating margin has been trending up over the last 12 months and averaged 15.8% over the last five years. On top of that, its profitability was top-notch for a business services business, showing it’s an well-run company with an efficient cost structure.

Looking at the trend in its profitability, Knowles’s adjusted operating margin might fluctuated slightly but has generally stayed the same over the last five years, highlighting the consistency of its expense base.

This quarter, Knowles generated an adjusted operating margin profit margin of 17.2%, up 3.6 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

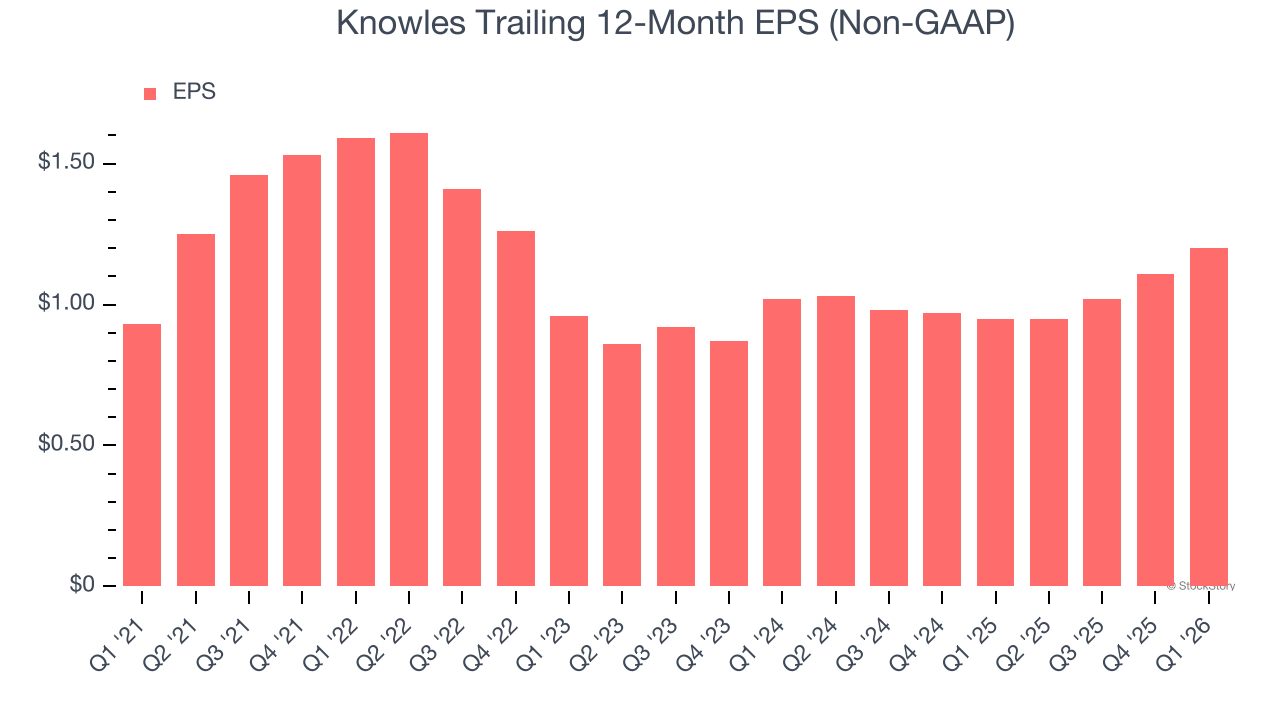

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Knowles’s EPS grew at 5.2% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 5.2% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Knowles, its two-year annual EPS growth of 8.5% was higher than its five-year trend. Accelerating earnings growth is almost always an encouraging data point.

In Q1, Knowles reported adjusted EPS of $0.27, up from $0.18 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Knowles’s full-year EPS of $1.20 to grow 10.6%.

Key Takeaways from Knowles’s Q1 Results

It was good to see Knowles beat analysts’ EPS expectations this quarter. We were also glad its revenue guidance for next quarter exceeded Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 3.8% to $32.45 immediately following the results.

Sure, Knowles had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).