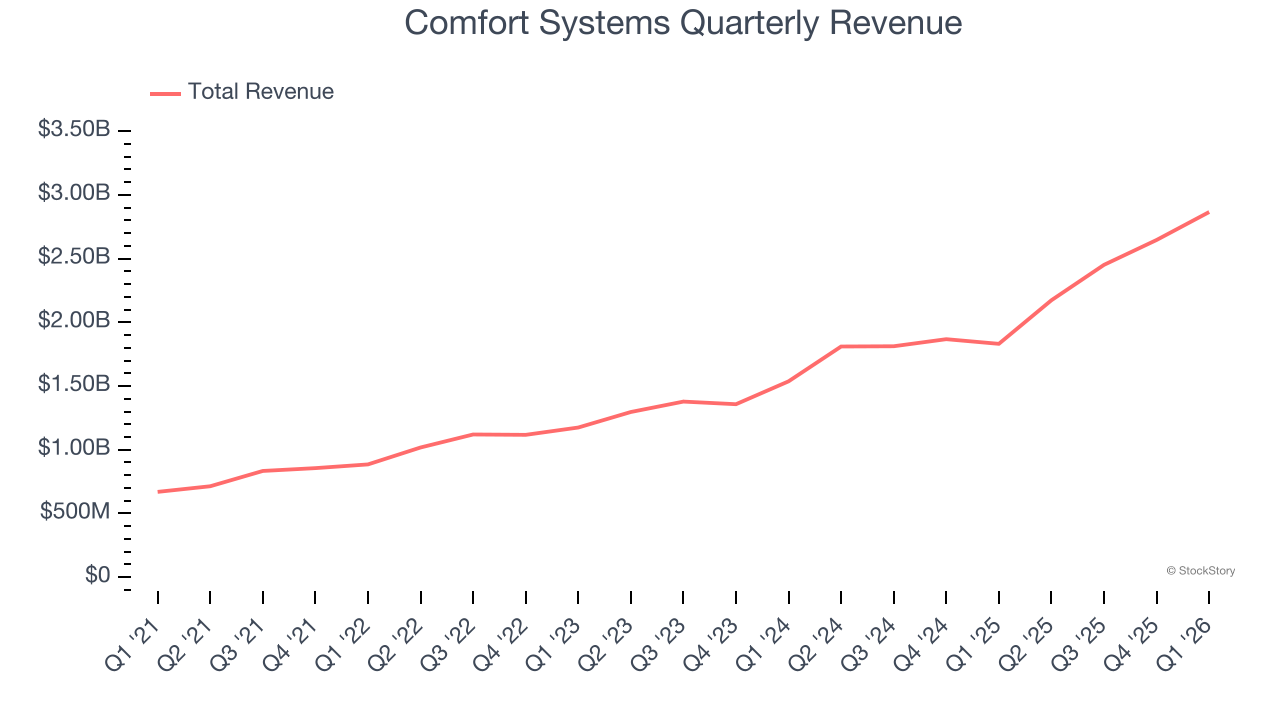

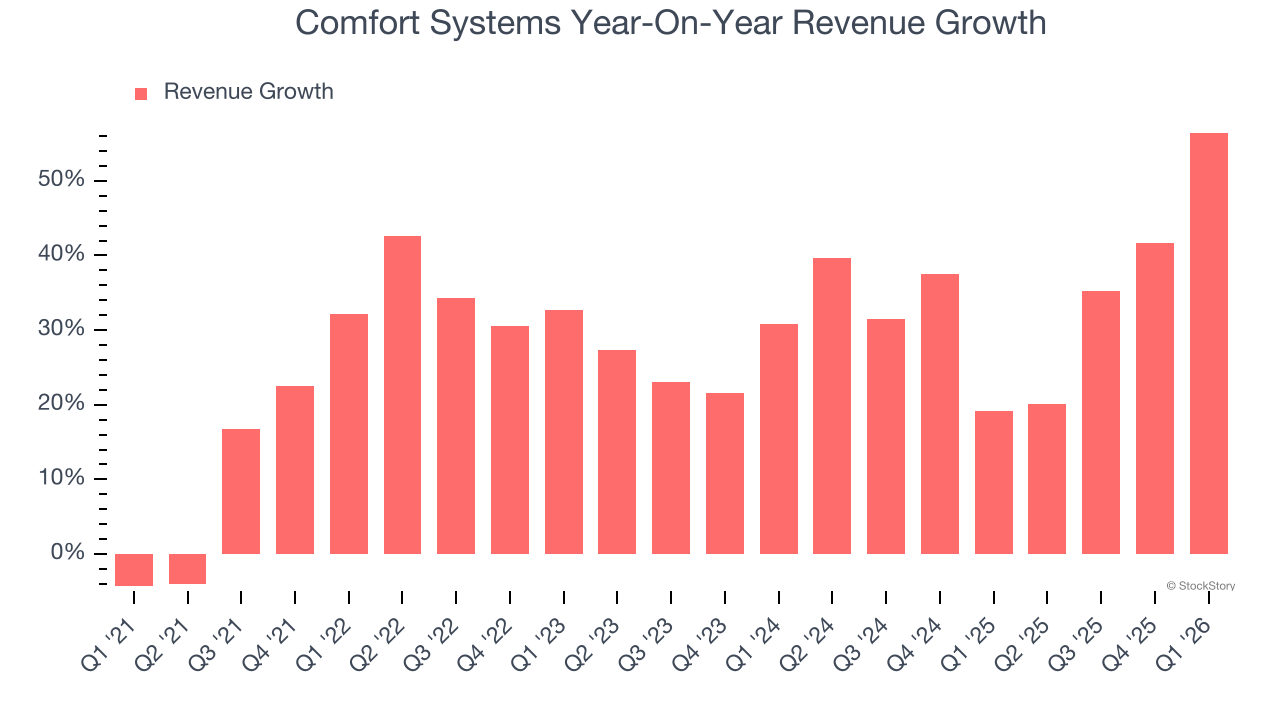

HVAC and electrical contractor Comfort Systems (NYSE: FIX) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 56.5% year on year to $2.87 billion. Its GAAP profit of $10.51 per share was 54.4% above analysts’ consensus estimates.

Is now the time to buy Comfort Systems? Find out by accessing our full research report, it’s free.

Comfort Systems (FIX) Q1 CY2026 Highlights:

- Revenue: $2.87 billion vs analyst estimates of $2.40 billion (56.5% year-on-year growth, 19.5% beat)

- EPS (GAAP): $10.51 vs analyst estimates of $6.81 (54.4% beat)

- Adjusted EBITDA: $524.4 million vs analyst estimates of $349.6 million (18.3% margin, 50% beat)

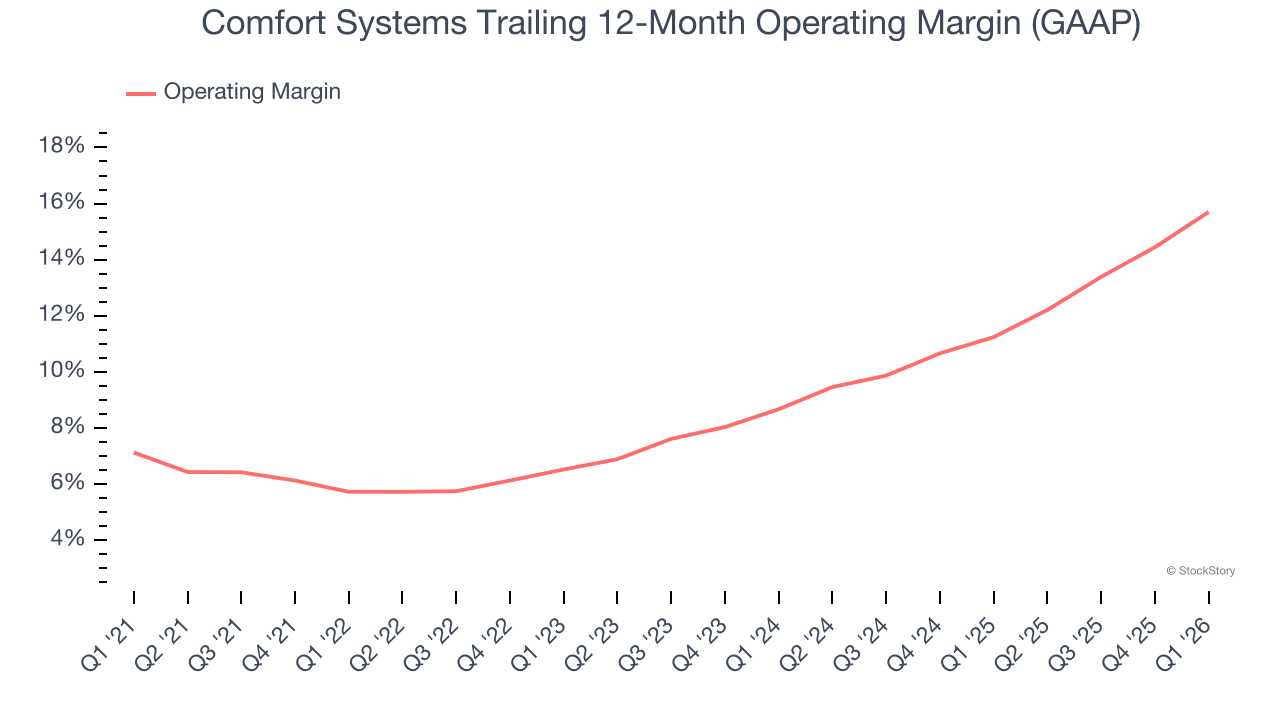

- Operating Margin: 17%, up from 11.4% in the same quarter last year

- Free Cash Flow was $242.2 million, up from -$109.1 million in the same quarter last year

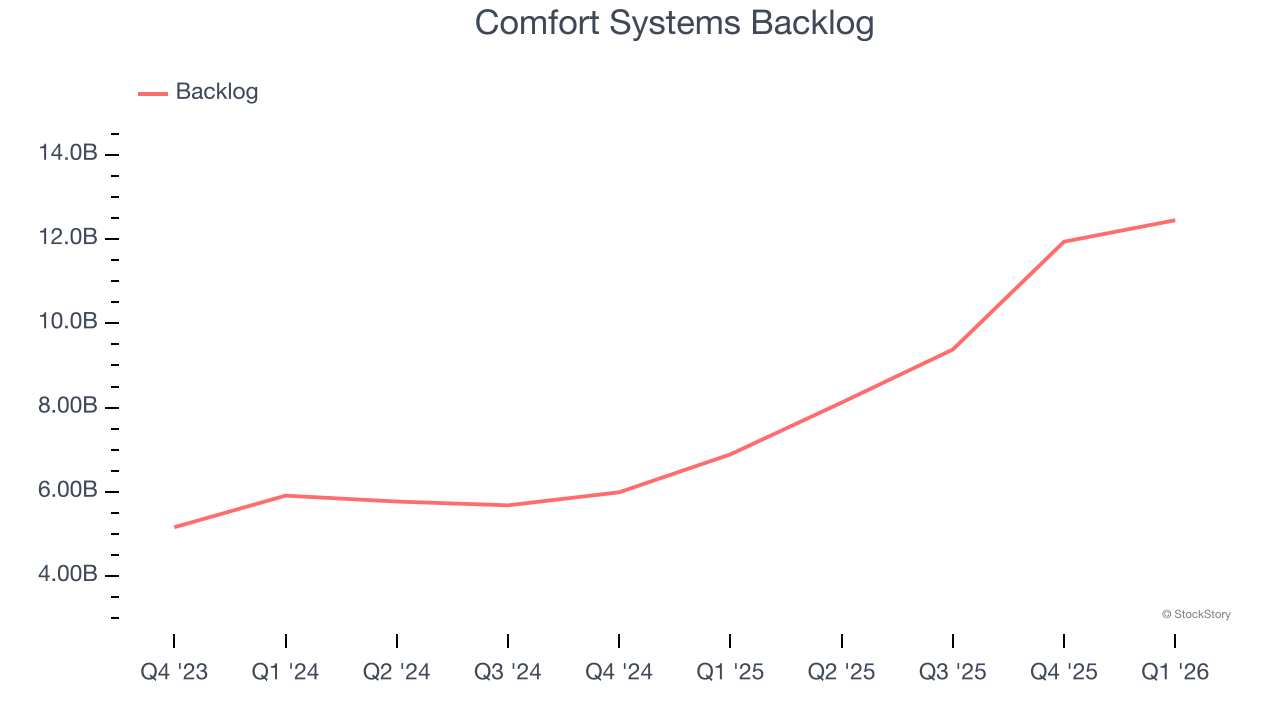

- Backlog: $12.45 billion at quarter end, up 80.7% year on year

- Market Capitalization: $60.57 billion

Brian Lane, Comfort Systems USA’s Chief Executive Officer, said, “Our growing teams continue to achieve masterful performance across the United States, and their excellence and dedication is delivering unmatched outcomes for our customers and communities. Thanks to these teams, Comfort Systems USA is achieving unprecedented results for our shareholders, including organic revenue growth this quarter of 51% compared to the same quarter of last year, and per share earnings that have more than doubled over the same period. In addition to our record growth and profitability, we achieved more than $375 million of quarterly cash flow.”

Company Overview

Formed through the merger of 12 companies, Comfort Systems (NYSE: FIX) provides mechanical and electrical contracting services.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Comfort Systems’s sales grew at an incredible 29.1% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Comfort Systems’s annualized revenue growth of 34.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Comfort Systems’s backlog reached $12.45 billion in the latest quarter and averaged 53.1% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Comfort Systems’s products and services but raises concerns about capacity constraints.

This quarter, Comfort Systems reported magnificent year-on-year revenue growth of 56.5%, and its $2.87 billion of revenue beat Wall Street’s estimates by 19.5%.

Looking ahead, sell-side analysts expect revenue to grow 11% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is attractive given its scale and implies the market is forecasting success for its products and services.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Comfort Systems has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 11%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Comfort Systems’s operating margin rose by 10 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q1, Comfort Systems generated an operating margin profit margin of 17%, up 5.5 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

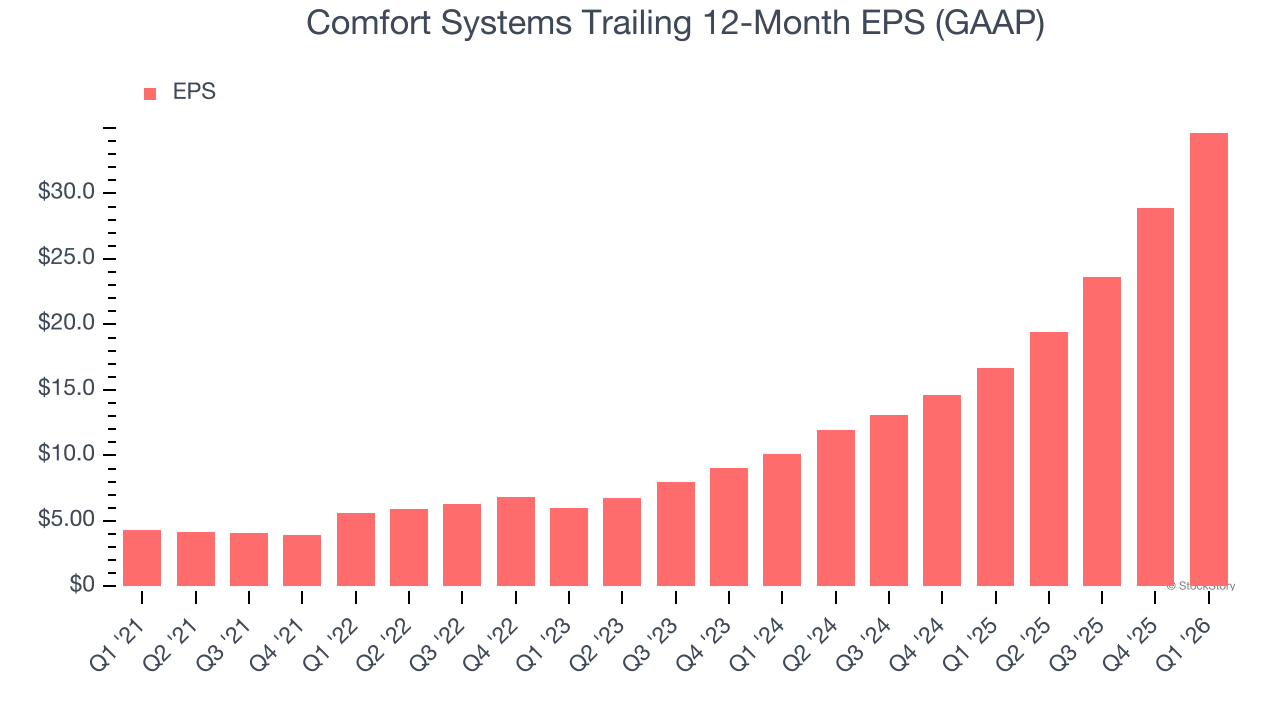

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Comfort Systems’s EPS grew at 51.5% compounded annual growth rate over the last five years, higher than its 29.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

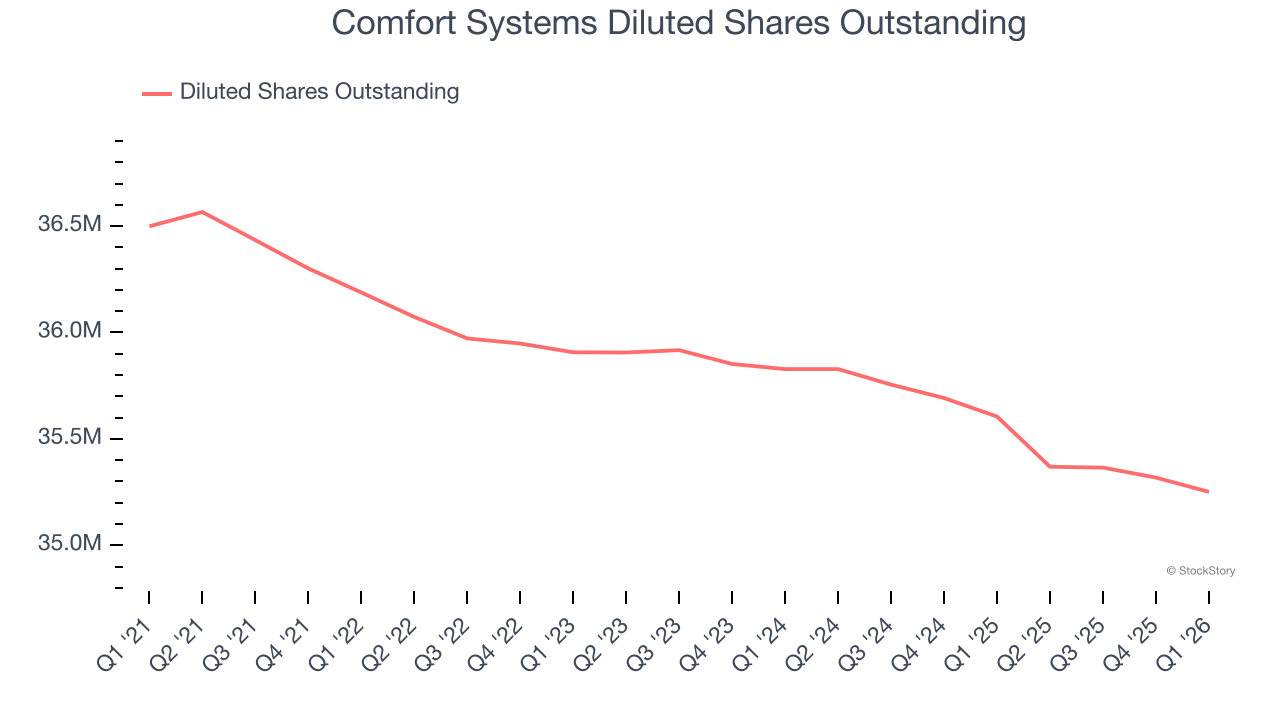

We can take a deeper look into Comfort Systems’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Comfort Systems’s operating margin expanded by 10 percentage points over the last five years. On top of that, its share count shrank by 3.4%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Comfort Systems, its two-year annual EPS growth of 85.2% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Comfort Systems reported EPS of $10.51, up from $4.75 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Comfort Systems’s full-year EPS of $34.65 to grow 8.3%.

Key Takeaways from Comfort Systems’s Q1 Results

It was good to see Comfort Systems beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 4.5% to $1,854 immediately after reporting.

Indeed, Comfort Systems had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).