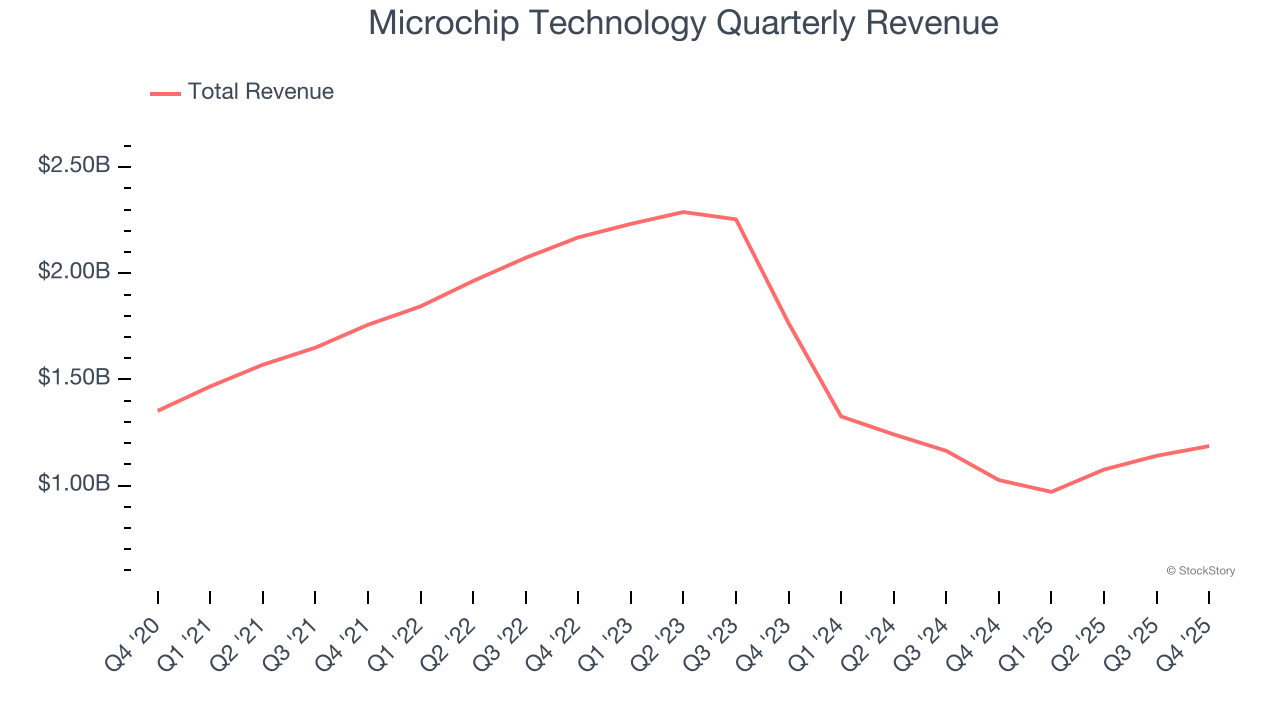

Analog chipmaker Microchip Technology (NASDAQ: MCHP) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 15.6% year on year to $1.19 billion. Guidance for next quarter’s revenue was optimistic at $1.26 billion at the midpoint, 2.4% above analysts’ estimates. Its non-GAAP profit of $0.44 per share was 2.7% above analysts’ consensus estimates.

Is now the time to buy Microchip Technology? Find out by accessing our full research report, it’s free.

Microchip Technology (MCHP) Q4 CY2025 Highlights:

- Revenue: $1.19 billion vs analyst estimates of $1.18 billion (15.6% year-on-year growth, 0.6% beat)

- Adjusted EPS: $0.44 vs analyst estimates of $0.43 (2.7% beat)

- Adjusted Operating Income: $337.8 million vs analyst estimates of $324.7 million (28.5% margin, 4% beat)

- Revenue Guidance for Q1 CY2026 is $1.26 billion at the midpoint, above analyst estimates of $1.23 billion

- Adjusted EPS guidance for Q1 CY2026 is $0.50 at the midpoint, above analyst estimates of $0.49

- Operating Margin: 12.8%, up from 3% in the same quarter last year

- Free Cash Flow Margin: 26.9%, up from 24.7% in the same quarter last year

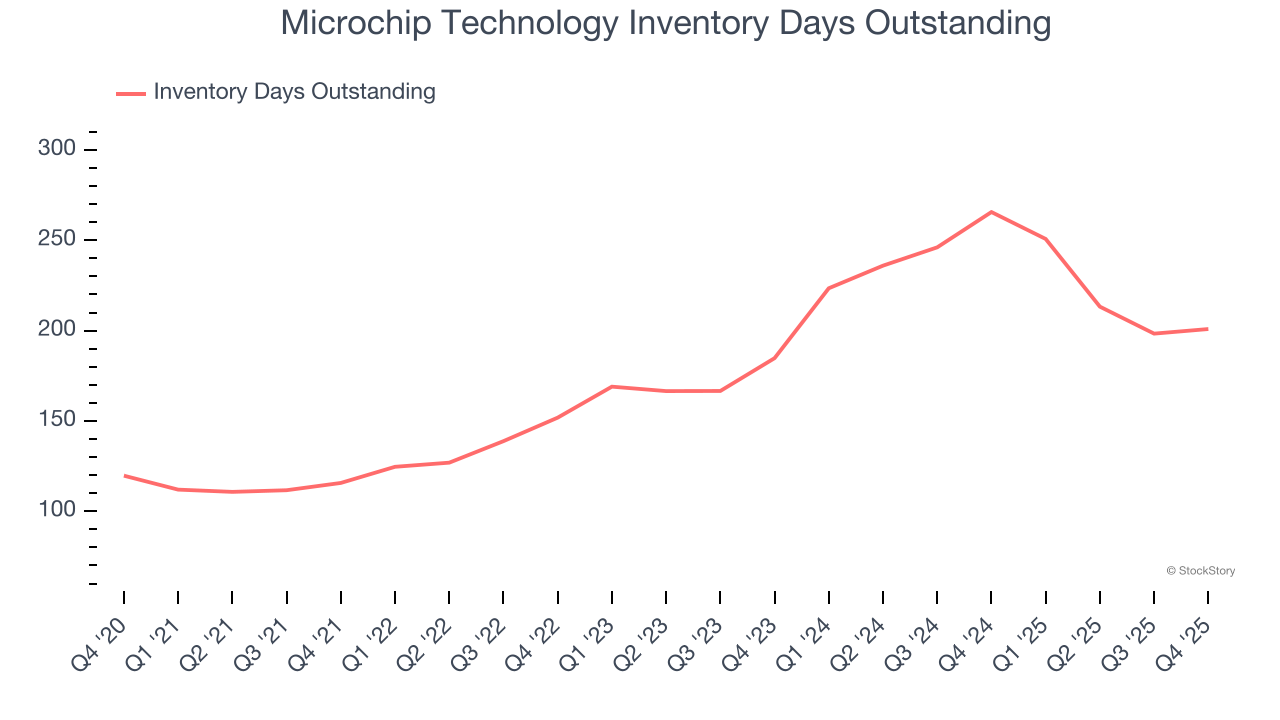

- Inventory Days Outstanding: 201, up from 198 in the previous quarter

- Market Capitalization: $42.28 billion

Steve Sanghi, Microchip’s CEO and President commented that, “Our fiscal third quarter results exceeded our expectations, with net sales of $1.186 billion growing 4% sequentially, and 15.6% year-over-year, well above our original guidance. We believe the broad-based recovery across our end markets, combined with significant margin expansion, demonstrates the tangible impact of our nine-point recovery plan execution. Our non-GAAP operating profit grew sequentially more than our net sales did in the December quarter, highlighting the operational momentum we have in our business.”

Company Overview

Spun out from General Instrument in 1987, Microchip Technology (NASDAQ: MCHP) is a leading provider of microcontrollers and integrated circuits used mainly in the automotive world, especially in electric vehicles and their charging devices.

Revenue Growth

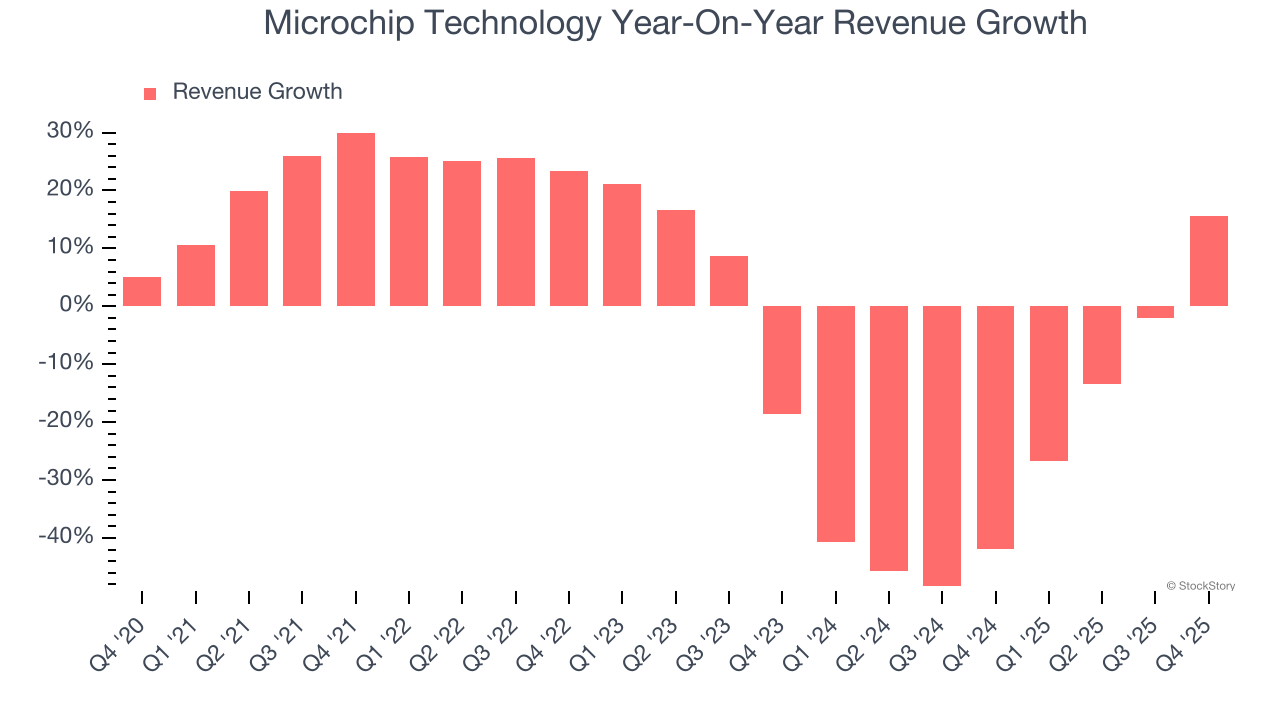

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Microchip Technology’s demand was weak and its revenue declined by 3.8% per year. This wasn’t a great result and suggests it’s a low quality business. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Microchip Technology’s recent performance shows its demand remained suppressed as its revenue has declined by 28.5% annually over the last two years.

This quarter, Microchip Technology reported year-on-year revenue growth of 15.6%, and its $1.19 billion of revenue exceeded Wall Street’s estimates by 0.6%. Adding to the positive news, Microchip Technology’s growth inflected positively this quarter, news that will likely give some shareholders hope. Company management is currently guiding for a 29.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 21.9% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and indicates its newer products and services will fuel better top-line performance.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Microchip Technology’s DIO came in at 201, which is 25 days above its five-year average, suggesting that the company’s inventory has grown to higher levels than we’ve seen in the past.

Key Takeaways from Microchip Technology’s Q4 Results

We enjoyed seeing Microchip Technology beat analysts’ adjusted operating income expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 4% to $75.03 immediately after reporting.

So should you invest in Microchip Technology right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).