Fortive’s 17.8% return over the past six months has outpaced the S&P 500 by 10.5%, and its stock price has climbed to $57.15 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Fortive, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Fortive Will Underperform?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons we avoid FTV and a stock we'd rather own.

1. Slow Organic Growth Suggests Waning Demand In Core Business

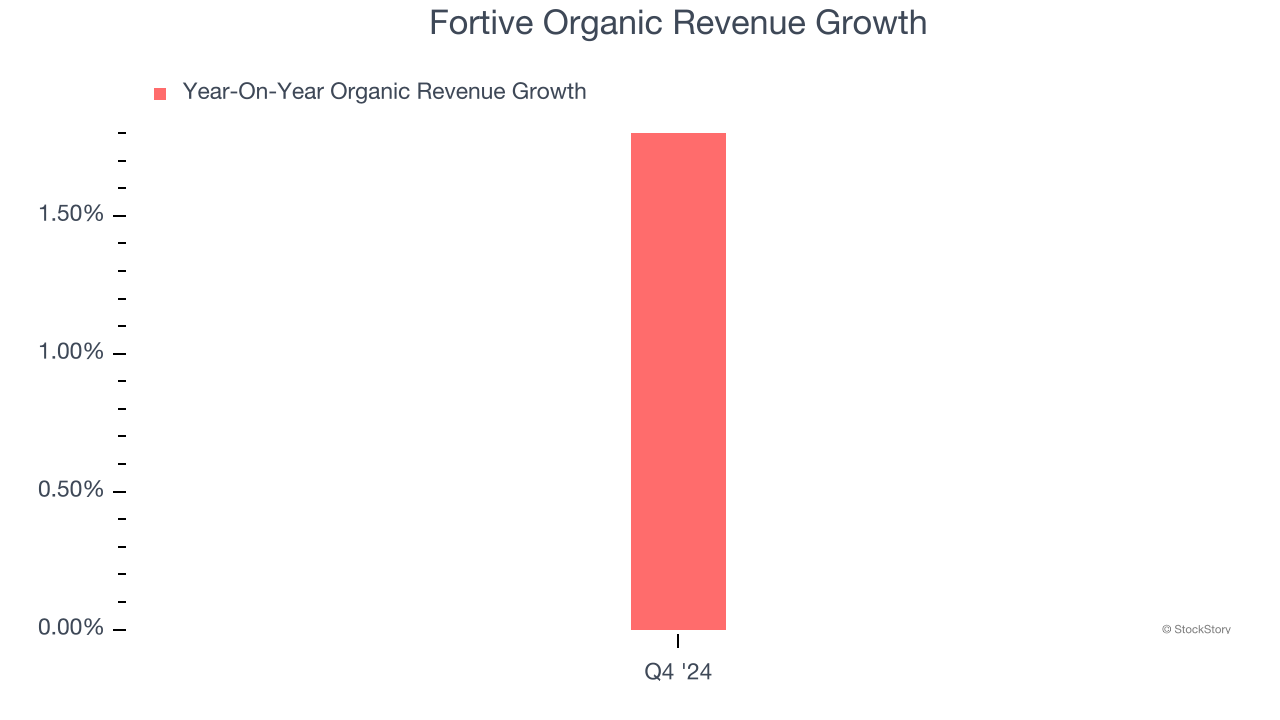

We can better understand Professional Tools and Equipment companies by analyzing their organic revenue. This metric gives visibility into Fortive’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Fortive’s organic revenue averaged 1.8% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Fortive’s revenue to drop by 3.8%, a decrease from its 2.1% annualized declines for the past five years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

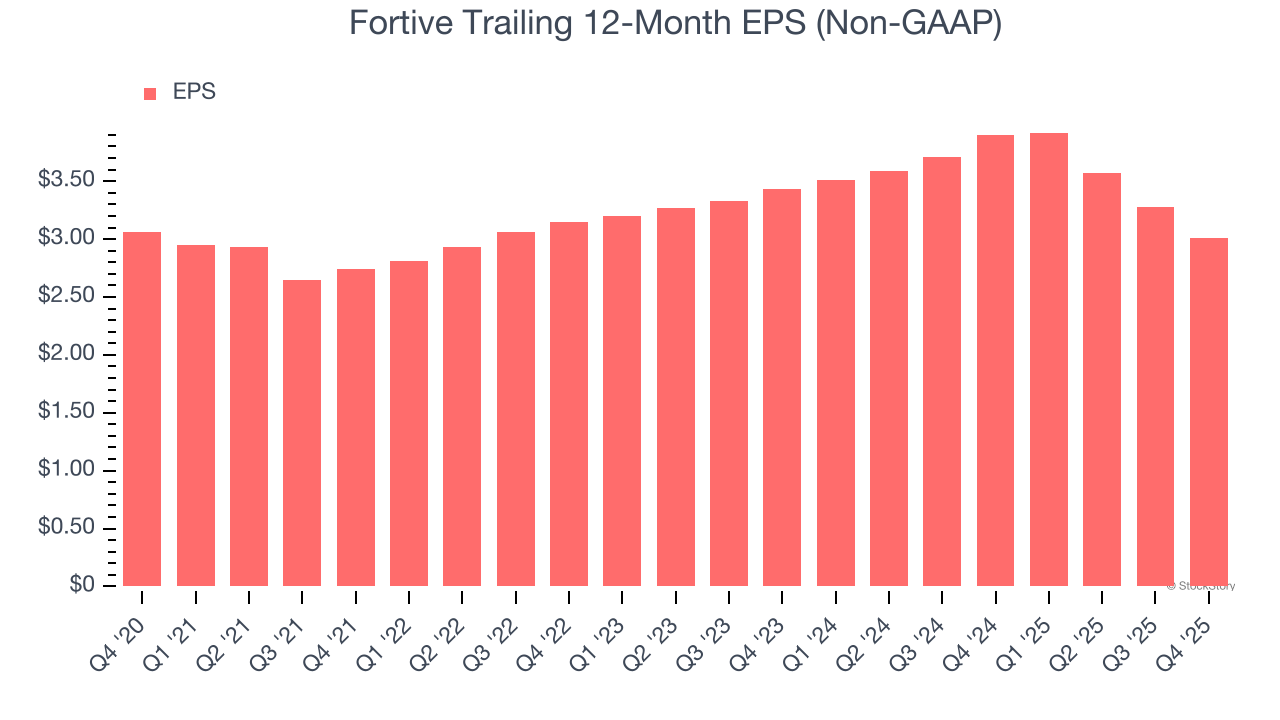

3. EPS Growth Has Stalled

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Fortive’s flat EPS over the last five years was weak. On the bright side, this performance was better than its 2.1% annualized revenue declines.

Final Judgment

We see the value of companies helping their customers, but in the case of Fortive, we’re out. With its shares beating the market recently, the stock trades at 19.7× forward P/E (or $57.15 per share). At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.