Collaboration software company Atlassian (NASDAQ: TEAM) announced better-than-expected revenue in Q3 CY2025, with sales up 20.6% year on year to $1.43 billion. On the other hand, the company’s full-year revenue guidance of $1.54 billion at the midpoint came in 75.1% below analysts’ estimates. Its non-GAAP profit of $1.04 per share was 24.1% above analysts’ consensus estimates.

Is now the time to buy Atlassian? Find out by accessing our full research report, it’s free for active Edge members.

Atlassian (TEAM) Q3 CY2025 Highlights:

- Revenue: $1.43 billion vs analyst estimates of $1.40 billion (20.6% year-on-year growth, 2.2% beat)

- Adjusted EPS: $1.04 vs analyst estimates of $0.84 (24.1% beat)

- Adjusted Operating Income: $322.7 million vs analyst estimates of $288.9 million (22.5% margin, 11.7% beat)

- Operating Margin: -6.7%, down from -2.7% in the same quarter last year

- Free Cash Flow Margin: 8%, down from 26% in the previous quarter

- Billings: $1.23 billion at quarter end, up 13.5% year on year

- Market Capitalization: $41.93 billion

“Our relentless pace of AI innovation is driving results as we grew Cloud revenue in Q1 to $998 million, up 26% year-over-year, and surpassed 3.5 million monthly active users of our AI capabilities, up 50% quarter-over-quarter,” said Mike Cannon-Brookes, Atlassian’s CEO and co-Founder.

Company Overview

Started by two Australian university friends who funded their startup with credit cards, Atlassian (NASDAQ: TEAM) provides software tools that help teams plan, track, collaborate, and share knowledge across organizations.

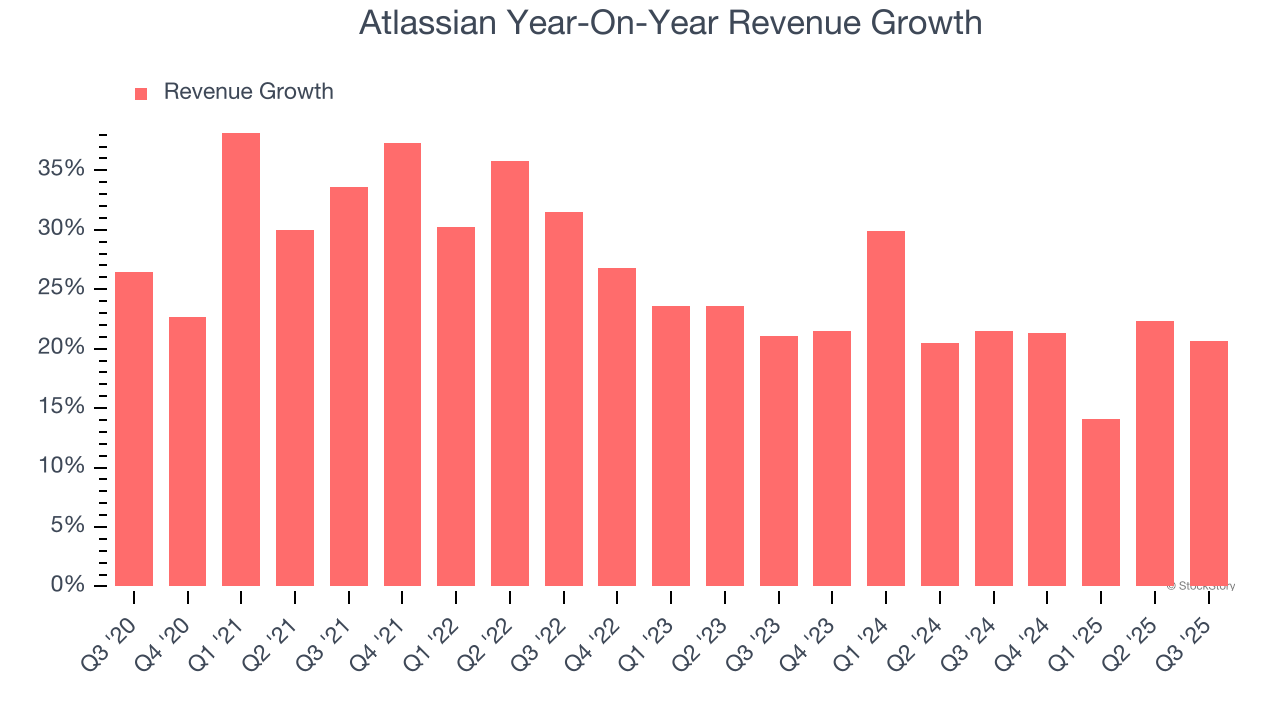

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Atlassian’s 26.1% annualized revenue growth over the last five years was solid. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Atlassian’s annualized revenue growth of 21.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Atlassian reported robust year-on-year revenue growth of 20.6%, and its $1.43 billion of revenue topped Wall Street estimates by 2.2%.

Looking ahead, sell-side analysts expect revenue to grow 17.9% over the next 12 months, a deceleration versus the last two years. Still, this projection is healthy and suggests the market is baking in success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

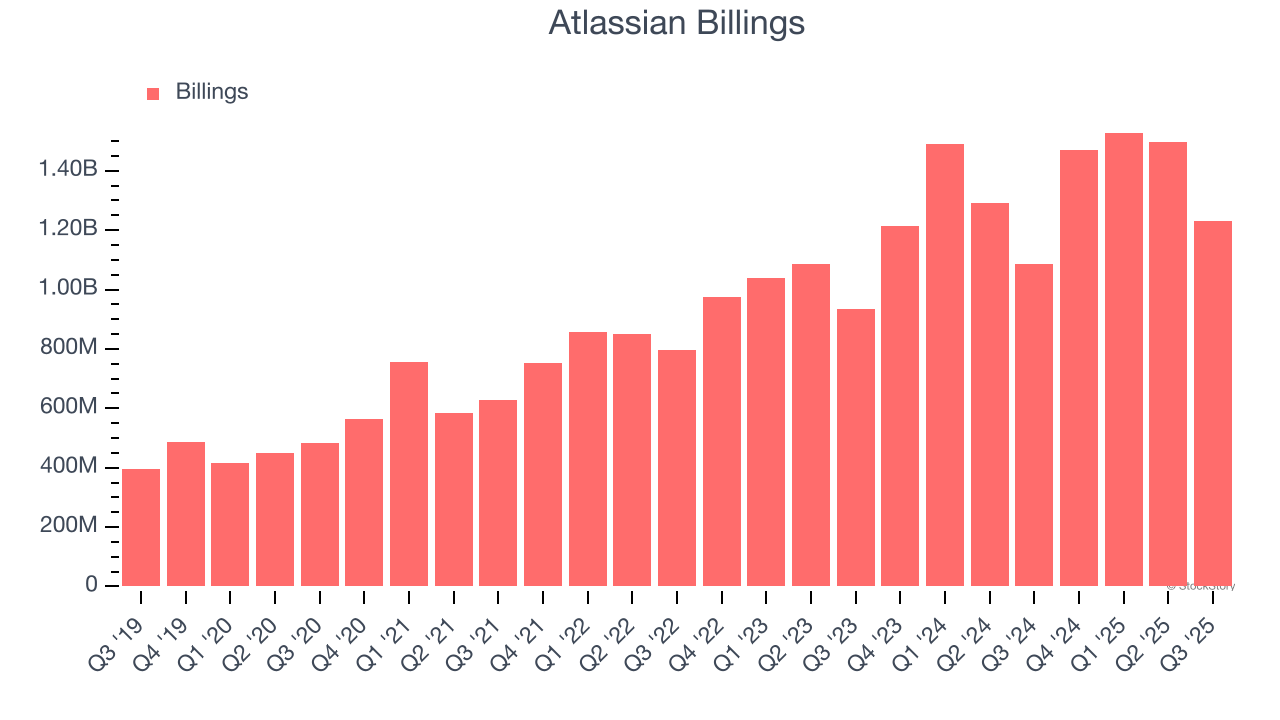

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Atlassian’s billings came in at $1.23 billion in Q3, and over the last four quarters, its growth slightly lagged the sector as it averaged 13.3% year-on-year increases. This alternate topline metric grew slower than total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Atlassian is extremely efficient at acquiring new customers, and its CAC payback period checked in at 21.4 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

Key Takeaways from Atlassian’s Q3 Results

It was encouraging to see Atlassian beat analysts’ revenue and adjusted operating profit expectations this quarter. Overall, this was a solid quarter. The stock traded up 5.7% to $170 immediately after reporting.

Is Atlassian an attractive investment opportunity at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.