Two very different commodities. Two very different risk profiles. One thing in common — both are creating genuine opportunities for investors who understand what is actually driving prices right now.

Energy markets in 2026 are not behaving the way textbooks say they should. WTI crude oil is swinging between $72 and $107 per barrel in the same quarter — driven by a combination of Strait of Hormuz supply disruptions, OPEC+ production pivots, and US domestic output running near record highs. Uranium briefly broke $101 per pound in January before pulling back, all while long-term contracting demand keeps climbing and mine supply stubbornly refuses to keep pace.

For investors paying attention, both of these energy commodities are presenting well-defined, fundamentally grounded opportunities right now. They are not interchangeable — they serve different portfolio roles, respond to different catalysts, and suit different time horizons. But together, they represent the two most interesting energy investment stories of this year.

Here are seven reasons why — and what you need to understand before entering either market.

Quick reference: The comparison table at the end of this article shows how WTI crude oil and uranium stack up across six key investment dimensions at a glance.

1. WTI Oil Is Living and Dying by Geopolitical Risk — and That Creates Tradeable Moments

The Strait of Hormuz closure in early 2026 was the kind of supply shock that turns theoretical risk scenarios into very real market events. Roughly 20% of global oil consumption transits this 21-mile chokepoint daily. When commercial shipping through the strait was effectively halted in late February, Brent crude rebounded from early-year lows near $60 to above $100 — a move that caught many passive oil investors flat-footed and rewarded those who had been watching the setup.

WTI’s current trading range of $71 to $107 per barrel for June 2026 (per LiteFinance forecasts) reflects this geopolitical premium sitting directly on top of a baseline supply-demand picture that is actually more balanced than previous cycles. The EIA’s latest Short-Term Energy Outlook assumes the Strait will remain largely closed into early summer, with flows slowly resuming in Q3 2026.

For traders, this environment creates two distinct types of opportunity: event-driven momentum trades around geopolitical escalations and de-escalations, and mean-reversion setups when the risk premium becomes overdone relative to actual supply disruption data.

When you invest in oil.WTI through a CFD instrument, you can position for moves in both directions — going long on escalation signals and short when ceasefire developments or Hormuz reopening news hits the wires. The key is having a platform with real-time news integration so you are not reacting to headlines after the move has already happened.

2. Uranium Has a Structural Deficit That Has Run for Five Consecutive Years

Most commodity supply deficits last a year or two before higher prices incentivize new production. Uranium’s deficit has now stretched across five consecutive years, and the World Nuclear Association’s reference scenario shows global installed nuclear capacity nearly doubling from 398 gigawatts in mid-2025 to 746 gigawatts by 2040. Mine supply is not on a trajectory to match that demand.

In 2025, utilities contracted for approximately 82 to 85 million pounds of uranium annually, while actual replacement requirements ran between 150 and 180 million pounds per year. That gap — met by drawing down above-ground inventories — is the central structural story of this commodity cycle. And unlike oil, where shale producers can ramp output within six to twelve months of higher prices, uranium mines take a decade or more from exploration to production.

The uranium spot price started 2026 at just over $80 per pound, surged to $101.41 on January 29, and has since consolidated in the $84 to $92 range as geopolitical instability triggered a sentiment rotation toward safe-haven assets. The structural bull case, however, has not changed — if anything, the policy backdrop has strengthened it significantly.

The US Department of Energy committed $2.7 billion over the next decade to expand domestic uranium enrichment in 2026, explicitly designating uranium as a critical national security resource under the Section 232 framework. This is long-term institutional demand that does not reverse with quarterly sentiment shifts.

3. AI Data Centers Are Creating a Demand Driver Neither Commodity Has Seen Before

Artificial intelligence is not just an equity market story. It is an energy story, and it is reshaping the demand outlook for both oil-adjacent energy sectors and nuclear power simultaneously.

The EIA projects US power demand to reach 4,256 billion kilowatt-hours in 2026, rising to 4,364 billion in 2027, driven primarily by AI infrastructure and cryptocurrency data centers ramping up at scale. Nuclear power is uniquely positioned to meet this demand — it provides baseload power 24 hours a day, 365 days a year, without the intermittency issues of solar and wind. This is exactly what hyperscale data centers need.

A global investor survey commissioned by Uranium.io found that the rapid expansion of AI systems is already reshaping long-term expectations for nuclear generation and uranium procurement — and that this demand is increasingly viewed as structural rather than cyclical. Tech companies are signing long-term power purchase agreements directly with nuclear operators, creating a new and highly predictable demand stream that was simply not part of the uranium market equation three years ago.

For WTI oil, the AI connection is more indirect but still real: the construction boom in data center infrastructure requires enormous amounts of diesel for generators, construction equipment, and logistics — adding a meaningful secondary demand layer to an already tight transportation fuel market.

4. OPEC+ Strategy Has Made WTI More Volatile — Not Less

OPEC+ accelerated its production quota increases at the April 2026 meeting, just as demand signals from China were softening and US domestic output remained near record levels from the Permian Basin. The result was a sharp price correction — then a rebound as Hormuz disruptions reminded the market why supply management matters.

This push-and-pull dynamic is not going away. Saudi Arabia and Russia have conflicting revenue pressures and market share concerns that make OPEC+ decisions genuinely unpredictable from quarter to quarter. Each scheduled meeting is a potential catalyst — for a 5 to 8% single-session move in WTI in either direction.

For active traders, this predictable unpredictability is actually an asset. OPEC+ meeting dates, EIA Weekly Petroleum Status reports (released every Wednesday), and Chinese manufacturing PMI data are all on the calendar in advance. Building a trading plan around these recurring catalysts — rather than reacting to them blindly — is one of the most reliable ways to approach WTI crude as a short-to-medium-term position.

5. Uranium Demand Is Price-Inelastic — Which Means Supply Shocks Hit Harder

One characteristic that makes uranium unlike virtually every other commodity is that nuclear reactor operators cannot substitute away from it. When a reactor is running, it needs a specific quantity of uranium fuel, regardless of the spot price. This price inelasticity means that when supply tightens, utilities do not cut back on procurement — they compete aggressively for available material, which is why spot price spikes in uranium can be both sudden and sustained.

Kazakhstan is the world’s largest uranium producer, supplying roughly 45% of global output through state-owned Kazatomprom. Production guidance revisions from Kazakhstan — whether upward or downward — are some of the most market-moving events in the uranium calendar. Canada’s Cigar Lake mine is another critical single point of supply concentration. Any production disruption at either location echoes immediately through the spot market.

Understanding these supply dynamics is fundamental before taking a position. For investors exploring how to invest in uranium, the most practical entry points are through uranium-linked equities, ETFs such as the Sprott Physical Uranium Trust, or commodity-linked instruments offered through regulated CFD platforms — rather than attempting to access the physical spot market, which operates through long-term utility contracts rather than retail channels.

6. The Institutional Money Has Already Made Its Decision on Both Commodities

Retail investors often look at commodity prices and ask where they are headed. Institutional investors look at where capital is already positioned — because large money moves before prices do, and the footprints are visible if you know where to look.

In uranium, the evidence is unambiguous. Sprott Asset Management has been actively accumulating physical uranium through its trust structure. Long-term contracting prices — the three-year and five-year forward uranium prices — spent most of 2025 moving incrementally higher even while spot prices were flat. That divergence signals utility companies locking in future supply at above-spot prices, which only makes sense if they believe spot prices are heading higher.

In WTI oil, institutional positioning has been consistently bullish on geopolitical risk premium through the first half of 2026, with Brent trading roughly $10 per barrel above what J.P. Morgan’s fundamental model suggests fair value to be. That premium exists because funds are paying for insurance against a Hormuz disruption scenario that has not fully materialized — and will rapidly unwind when a ceasefire is confirmed, creating a sharp short-side opportunity.

Reading institutional positioning through the CFTC Commitments of Traders report for oil, and through ETF flow data for uranium, gives retail investors access to the same directional signals that professional desks use — with a one-week lag. In slow-moving commodity cycles, that lag is rarely fatal.

7. These Two Commodities Work Together in a Portfolio — Not Against Each Other

The most sophisticated energy investors in 2026 are not choosing between WTI oil and uranium. They are holding both with different position sizes, different time horizons, and different exit triggers — because the two commodities respond to different catalysts and provide genuine diversification within a single energy sector allocation.

WTI oil is the short-to-medium-term tactical position: highly liquid, event-driven, responsive to geopolitical news flow and weekly EIA data. It is a trader’s market right now, and the $35-per-barrel range between the June lows and highs tells you exactly how much opportunity there is for active participants.

Uranium is the medium-to-long-term structural position: less liquid in spot form, driven by decade-long demand cycles rather than weekly news, and increasingly backed by government policy decisions that create multi-year demand floors. It requires patience and conviction, but the structural bull case — five consecutive supply deficits, nuclear capacity nearly doubling by 2040, AI-driven electricity demand accelerating — is as strong as any commodity investment thesis on the board right now.

Together, they give an energy-focused investor both a tactical trading instrument and a long-term holding position, with genuine fundamental diversification between the two.

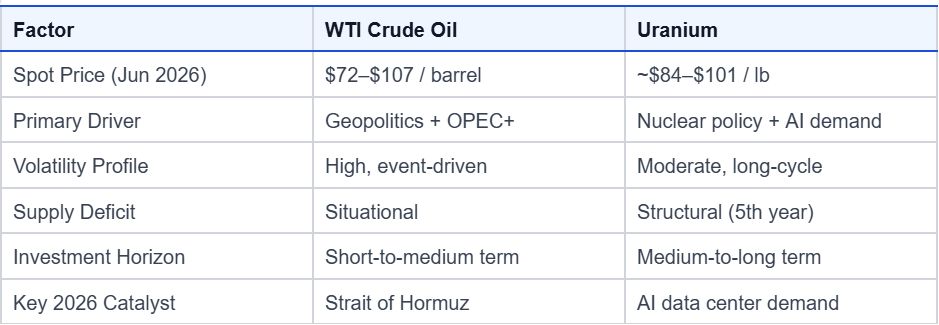

Quick Comparison: WTI Crude Oil vs. Uranium in 2026

Final Thought

Energy investing in 2026 rewards those who understand that different commodities require different strategies. WTI oil is a market for active, informed traders who can respond quickly to scheduled catalysts and geopolitical headlines. Uranium is a market for investors with the patience to hold a structural thesis across a multi-year cycle.

Neither is a set-and-forget trade. Both require continuous attention, disciplined risk management, and the right platform infrastructure to execute cleanly. But for investors willing to put in the work, the fundamental setups in both markets are as compelling as anything the energy sector has offered in years.

The question is not whether opportunity exists here. It clearly does. The question is whether you are prepared to approach it with the depth and discipline it deserves.

Risk Disclaimer: CFDs and commodity instruments are complex financial products that carry a high risk of losing money rapidly due to leverage. This article is for informational and educational purposes only and does not constitute investment or financial advice. Always conduct your own research and consider your personal financial circumstances before making any investment decisions.