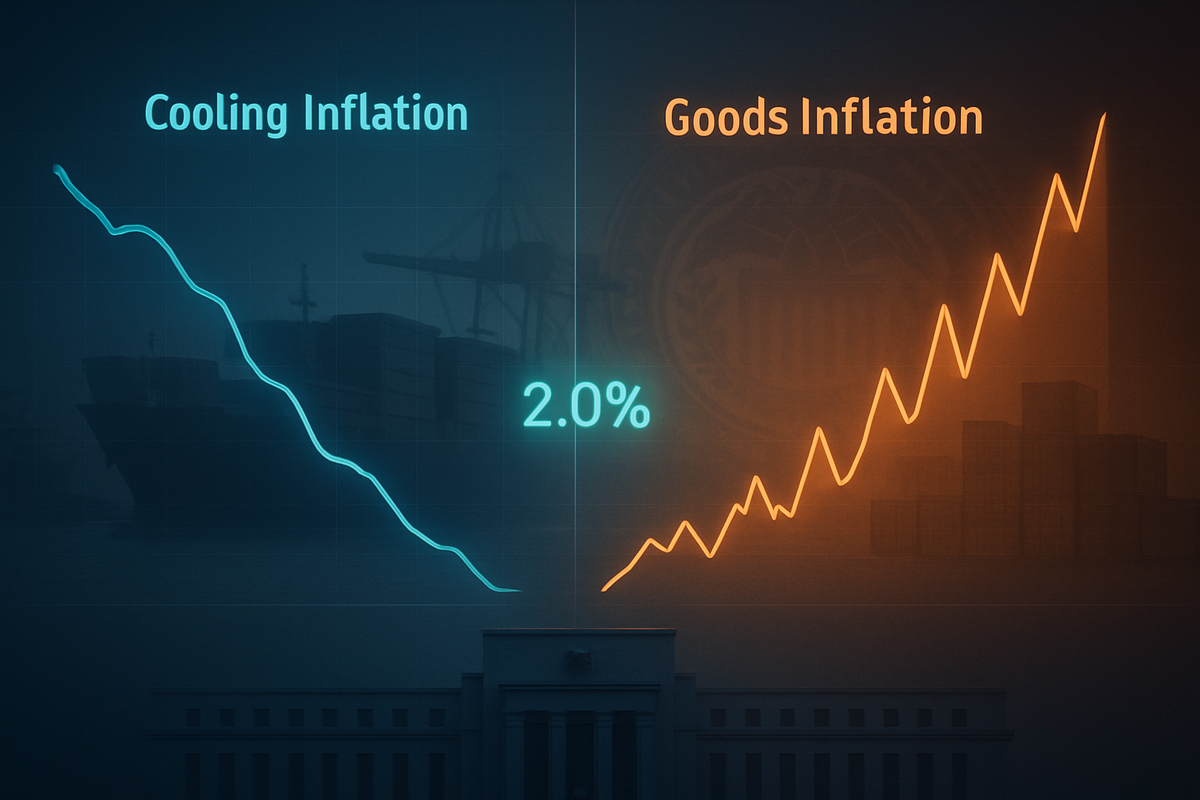

The latest Personal Consumption Expenditures (PCE) price index data has revealed a significant shift in the U.S. inflationary landscape, presenting a complex puzzle for the Federal Reserve. As of early February 2026, the data shows a stark divergence: while the services sector—the primary engine of post-pandemic inflation—is finally showing signs of cooling, a sharp resurgence in goods inflation driven by aggressive trade tariffs is threatening to keep the headline rate well above the central bank’s 2% target.

Investors and policymakers are now grappling with what many are calling the "last mile" challenge. With core PCE estimated to have reached 2.9% in December 2025, up from 2.8% in November, the Federal Reserve’s "strategic pause" in its January meeting has signaled a cautious approach. The market's reaction has been mixed, with the S&P 500 briefly touching the historic 7,000 mark before retreating as the reality of a "higher-for-longer" interest rate environment settles in.

Inflation’s New Face: Goods Volatility and Service Stability

The path to early 2026 has been marked by a dramatic "reversal" of historical trends. Throughout much of 2024 and early 2025, goods were largely deflationary, helping to offset the "sticky" services inflation that plagued the economy. However, the implementation of broad import tariffs in 2025 has upended this dynamic. Core goods prices rose by 1.4% year-over-year in late 2025—the highest non-pandemic increase since 2011. Corporate reports indicate that as companies exhausted their "pre-tariff" inventories, they were forced to pass these higher costs directly to consumers, ending the period of cheaper manufactured goods.

Conversely, the services sector is finally moderating. This shift is driven primarily by a deceleration in shelter prices and home values, which have historically been the most stubborn components of the index. Federal Reserve Governor Michelle Bowman noted in recent commentary that, when adjusting for one-time tariff effects, core services inflation is now roughly consistent with the 2% long-term goal. Nevertheless, specific services like hotel rates (+7.3%) and airline fares (+2.9%) remain outliers, preventing a more rapid decline in the headline number.

The Federal Reserve's response to this data was a strategic hold on interest rates at 3.50%–3.75% during the January 2026 meeting. The decision was not unanimous, featuring a rare 10-2 split vote. Dissenting voices, including Governors Miran and Waller, have expressed concerns that a cooling labor market might require immediate cuts, while the majority remains fixated on preventing inflation from stabilizing at a permanent 3% level.

Winners and Losers in a Tariff-Adjusted Economy

The current inflationary environment has created distinct winners and losers across the corporate landscape. Companies heavily dependent on international supply chains are feeling the brunt of the tariff-driven spike in goods prices. The Estée Lauder Companies Inc. (NYSE: EL) saw its stock plunge 19% after warning that import duties on luxury goods could reach as high as 39%, severely compressing margins. Similarly, Amazon.com Inc. (NASDAQ: AMZN) CEO Andy Jassy highlighted a challenging outlook for 2026, as consumers become more price-conscious in the face of tariff-related retail hikes.

Manufacturing and heavy industry are also under pressure. Lockheed Martin Corporation (NYSE: LMT) reported an estimated $350 million in tariff-related costs, while Deere & Company (NYSE: DE) cited a staggering $600 million impact in recent financial filings. Energizer Holdings, Inc. (NYSE: ENR) noted that tariffs have created a 300-basis-point headwind to its gross margins, forcing a shift in its 2026 earnings guidance. Even the fast-casual giant Chipotle Mexican Grill, Inc. (NYSE: CMG) has been forced to raise menu prices as the costs of beef, poultry, and packaging soar due to trade duties.

On the other hand, companies that have successfully localized production or operate in less trade-sensitive sectors are showing resilience. Stellantis N.V. (NYSE: STLA) has proactively announced a $13 billion investment to move production onshore in the United States to mitigate trade risks. Meanwhile, the healthcare and technology sectors continue to provide shelter for investors. Regeneron Pharmaceuticals, Inc. (NASDAQ: REGN) emerged as a top performer, beating earnings expectations despite the macroeconomic volatility, as demand for specialized healthcare remains less sensitive to the tariff-driven goods inflation cycle.

Policy Implications and Historical Context

The current situation bears a striking resemblance to the "reflationary" periods of the late 20th century, though with a modern twist. The Fed’s dilemma—balancing a cooling labor market against a tariff-induced spike in prices—has led to a debate over "tariff-adjusted" inflation metrics. If the Fed chooses to "look through" the temporary price increases caused by trade policy, they might risk losing their credibility on the 2% target. However, staying too restrictive could trigger an unnecessary recession.

The broader market narrative is currently split. There is a "reflation narrative" fueled by productivity gains from widespread artificial intelligence adoption, which some analysts believe will allow the economy to maintain growth even with inflation slightly above target. This optimism is what pushed the S&P 500 toward the 7,000 milestone. Yet, historical precedents suggest that when goods inflation turns positive after a long period of deflation, it can be difficult to rein in without a significantly cooled labor market.

Regulatory and trade policies remain the wild cards. The 2025 tariffs were intended to bolster domestic manufacturing, but the immediate ripple effect has been a tax on the American consumer. Partners and competitors abroad are watching closely, as any further escalation in trade tensions could solidify this "goods inflation" trend, making the Federal Reserve's 2% target a moving goalpost rather than a fixed destination.

The Road Ahead: What to Watch for in 2026

In the short term, all eyes are on the February 20, 2026, release of the December 2025 PCE data. If the figure matches or exceeds the 2.9% estimate, the Federal Reserve is likely to maintain its restrictive stance through the spring. Markets will also be watching for signs of a strategic pivot in corporate supply chains. As seen with Stellantis, a wave of "onshoring" could eventually lead to domestic price stability, but the transition period is likely to be characterized by continued volatility and margin compression for many S&P 500 firms.

For investors, the coming months will require a discerning eye for companies with "pricing power"—the ability to pass on costs without losing volume. American Express Company (NYSE: AXP), which recently reported earnings slightly below expectations, serves as a bellwether for whether the affluent consumer is finally beginning to pull back. If consumer spending patterns shift significantly, it may force the Fed's hand toward a rate cut, regardless of the inflation headline.

Summary of the Market Outlook

The latest PCE data underscores a pivotal moment for the U.S. economy. The successful cooling of services inflation is a hard-won victory for the Federal Reserve, but it is being overshadowed by the political and economic reality of new trade barriers. The divergence between goods and services means that "core" inflation is no longer a monolith, and investors must analyze company exposure to international trade more closely than ever.

Moving forward, the primary risk is that inflation becomes entrenched near the 3% mark, necessitating a longer period of high interest rates that could eventually weigh on corporate valuations. While the "AI productivity" story provides a bullish backdrop, the immediate reality is a tug-of-war between declining shelter costs and rising import duties. Investors should watch for the next round of retail earnings and the Fed’s March dot plot for clarity on whether the 2% target remains achievable in the "Tariff Era."

This content is intended for informational purposes only and is not financial advice