Lake Success, New York-based Broadridge Financial Solutions, Inc. (BR) is a financial technology company that provides critical investor communications and technology-driven solutions for the financial services industry. It is valued at a market cap of $17.4 billion.

This financial company has notably underperformed the broader market over the past 52 weeks. Shares of BR have declined 38% over this time frame, while the broader S&P 500 Index ($SPX) has gained 27.4%. Moreover, on a YTD basis, the stock is down 34.1%, compared to SPX’s 8.8% rise.

Zooming in further, BR has also significantly lagged the State Street Technology Select Sector SPDR ETF’s (XLK) 63.3% rise over the past 52 weeks and 28.6% YTD uptick.

On Apr. 30, shares of BR plunged 4.2% after its Q3 earnings release, despite posting better-than-expected performance. The company delivered revenue of $1.95 billion, up 7.8% from the year-ago quarter and 2.1% ahead of analyst estimates. Its adjusted EPS of $2.72 topped consensus expectations of $2.63. However, investor sentiment turned negative as concerns emerged during the earnings call. Management pointed to extended sales cycles and delays in closing larger, more complex transactions as factors weighing on closed sales performance, even as the company continued to report strong pipeline growth and healthy client renewal rates.

For the current fiscal year, ending in June, analysts expect BR’s EPS to grow 11.7% year over year to $9.55. The company’s earnings surprise history is promising. It exceeded the consensus estimates in each of the last four quarters.

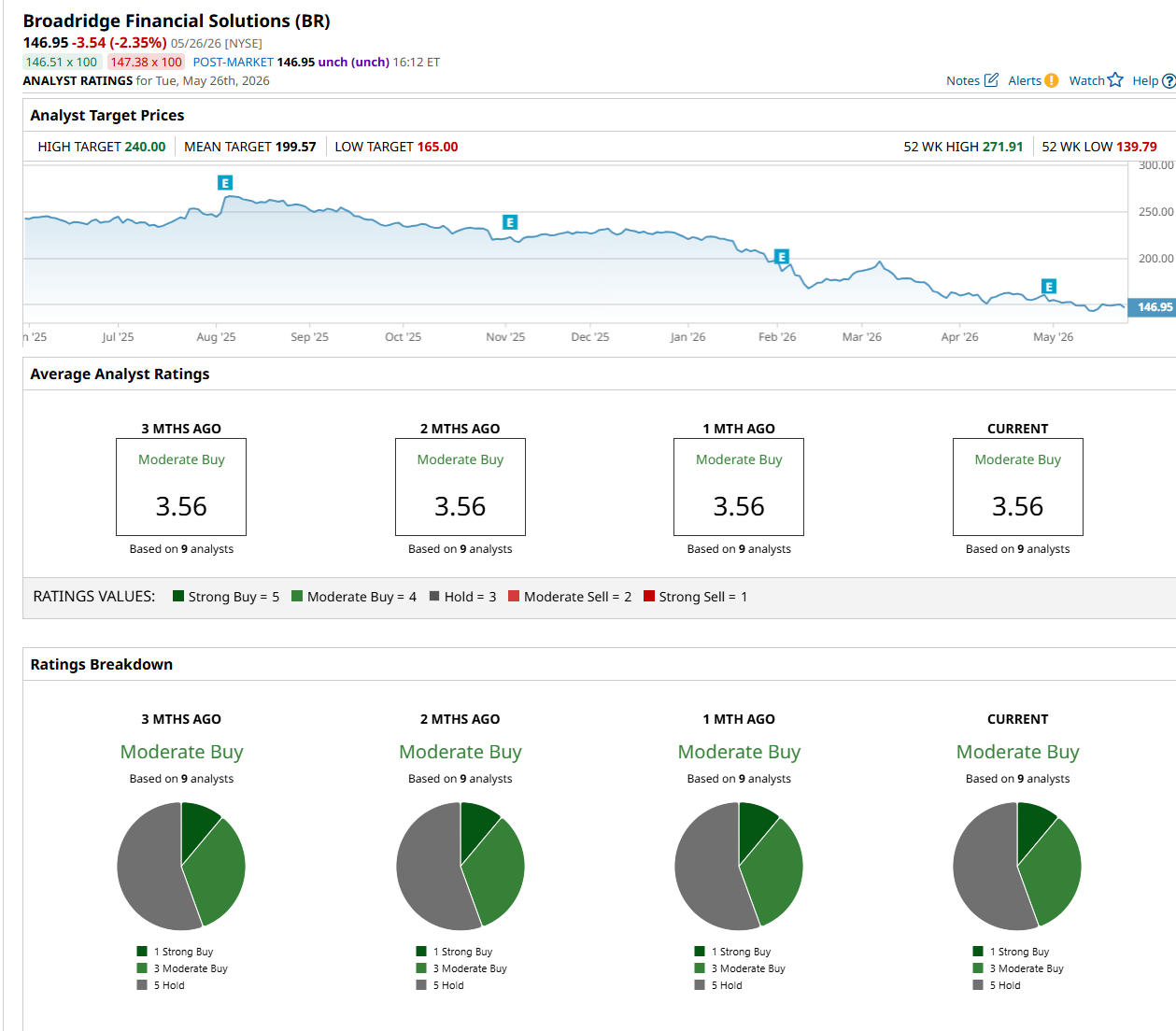

Among the nine analysts covering the stock, the consensus rating is a "Moderate Buy," which is based on one “Strong Buy,” three "Moderate Buy,” and five “Hold” ratings.

The configuration has remained consistent over the past three months.

On May 10, Morgan Stanley analyst James Faucette maintained an “Equal Weight” rating on BR and lowered its price target to $169, indicating a 15% potential upside from the current levels.

The mean price target of $199.57 suggests a 35.8% premium to its current price levels, while its Street-high price target of $240 implies a 63.3% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart