Let’s dig into the relative performance of Dillard's (NYSE: DDS) and its peers as we unravel the now-completed Q1 general merchandise retail earnings season.

General merchandise retailers–also called broadline retailers–know you’re busy and don’t want to drive around wasting time and gas, so they offer a one-stop shop. Convenience is the name of the game, so these stores may sell clothing in one section, toys in another, and home decor in a third. This concept has evolved over time from department stores to more niche concepts targeting bargain hunters or young adults, and e-commerce has forced these retailers to be extra sharp in their value propositions to consumers, whether that’s unique product or competitive prices.

The 8 general merchandise retail stocks we track reported a very strong Q1. As a group, revenues beat analysts’ consensus estimates by 2.5% while next quarter’s revenue guidance was 0.8% below.

In light of this news, share prices of the companies have held steady as they are up 4.2% on average since the latest earnings results.

Dillard's (NYSE: DDS)

With stores located largely in the Southern and Western US, Dillard’s (NYSE: DDS) is a department store chain that sells clothing, cosmetics, accessories, and home goods.

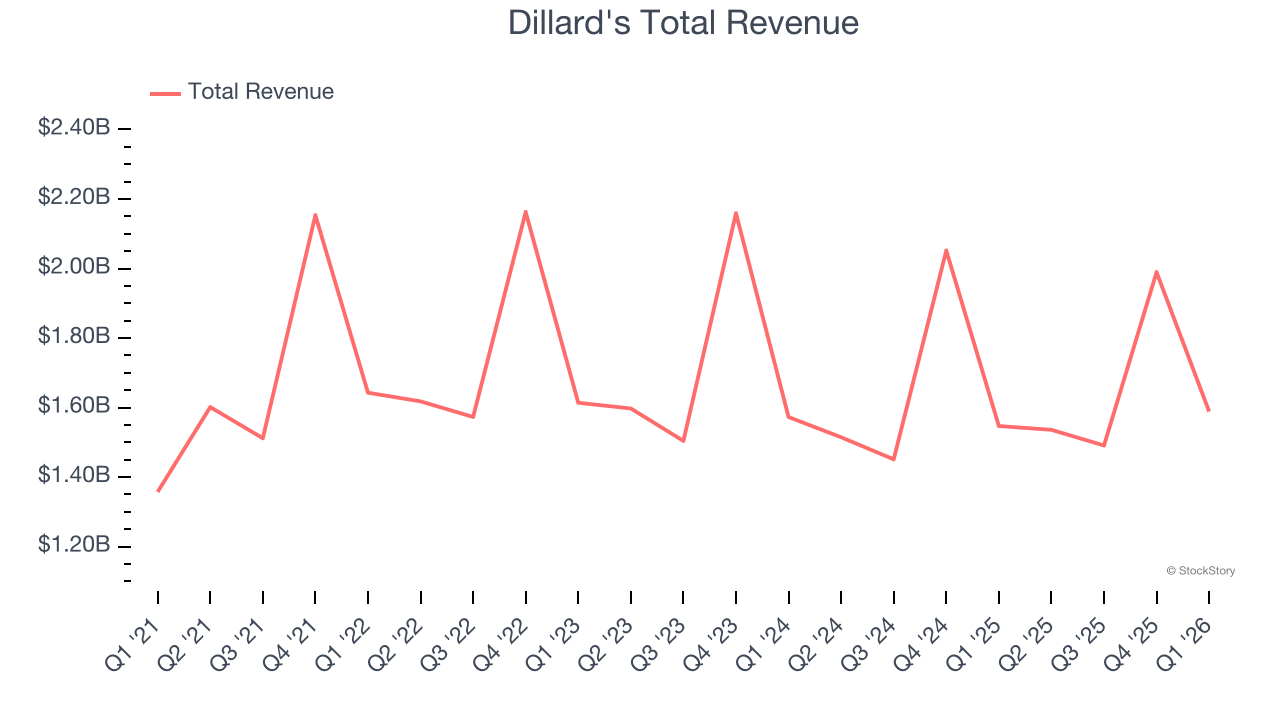

Dillard's reported revenues of $1.59 billion, up 2.7% year on year. This print exceeded analysts’ expectations by 1.3%. Overall, it was a very strong quarter for the company with a solid beat of analysts’ EBITDA and EPS estimates.

Dillard’s Chief Executive Officer William T. Dillard, II commented, “We are pleased to report a good start to 2026 with a profitable 3% sales growth supported by an increased 45.8% retail gross margin. We continue to focus on motivating our customer with newness in our merchandise assortment.”

Interestingly, the stock is up 14.8% since reporting and currently trades at $611.87.

Is now the time to buy Dillard's? Access our full analysis of the earnings results here, it’s free.

Best Q1: Ross Stores (NASDAQ: ROST)

Selling excess inventory or overstocked items from other retailers, Ross Stores (NASDAQ: ROST) is an off-price concept that sells apparel and other goods at prices much lower than department stores.

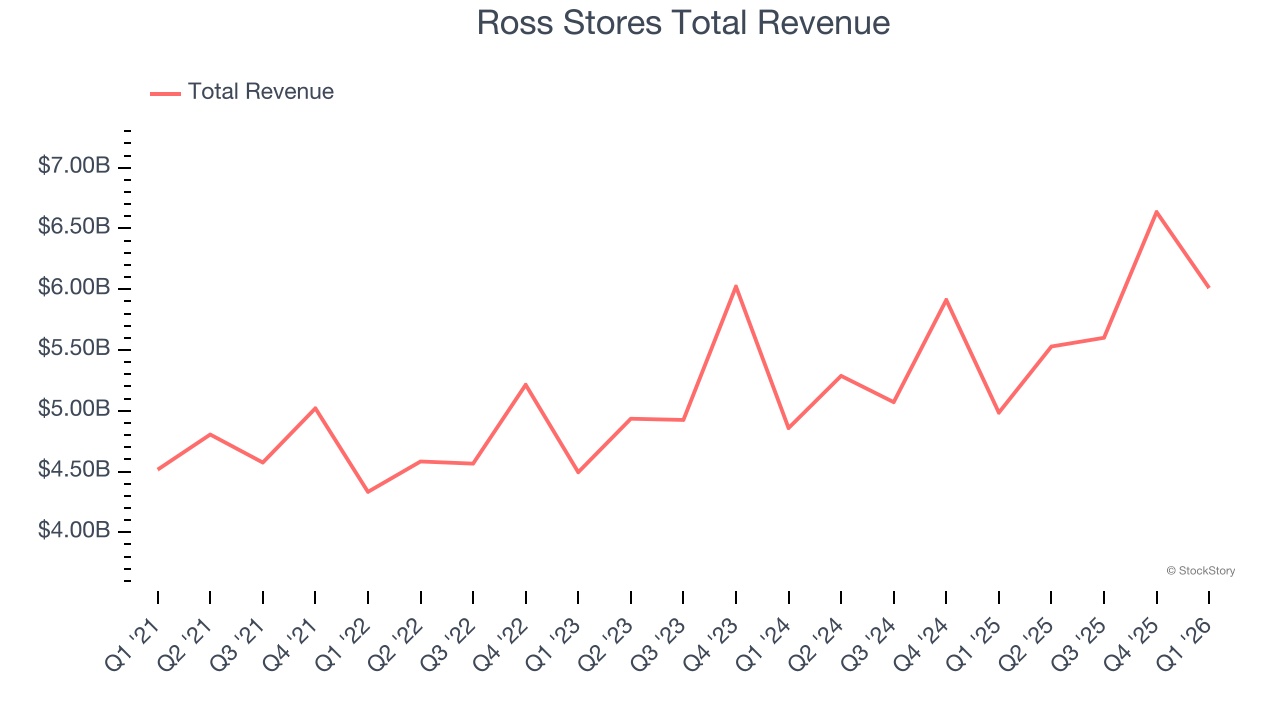

Ross Stores reported revenues of $6.01 billion, up 20.6% year on year, outperforming analysts’ expectations by 6.6%. The business had a stunning quarter with EPS guidance for next quarter exceeding analysts’ expectations and a solid beat of analysts’ EBITDA estimates.

Ross Stores scored the biggest analyst estimate beat among its peers. The market seems happy with the results as the stock is up 5.1% since reporting. It currently trades at $228.30.

Is now the time to buy Ross Stores? Access our full analysis of the earnings results here, it’s free.

Slowest Q1: Kohl's (NYSE: KSS)

Founded as a corner grocery store in Milwaukee, Wisconsin, Kohl’s (NYSE: KSS) is a department store chain that sells clothing, cosmetics, electronics, and home goods.

Kohl's reported revenues of $3.17 billion, down 2% year on year, in line with analysts’ expectations. Still, it was a satisfactory quarter as it posted a beat of analysts’ EPS estimates.

Kohl's delivered the slowest revenue growth in the group. Interestingly, the stock is up 25.3% since the results and currently trades at $16.21.

Read our full analysis of Kohl’s results here.

Ollie's (NASDAQ: OLLI)

Often located in suburban or semi-rural shopping centers, Ollie’s Bargain Outlet (NASDAQ: OLLI) is a discount retailer that acquires excess inventory then sells at meaningful discounts.

Ollie's reported revenues of $658.9 million, up 14.2% year on year. This result missed analysts’ expectations by 0.7%. Aside from that, it was a strong quarter as it put up an impressive beat of analysts’ EBITDA and gross margin estimates.

Ollie's achieved the highest full-year guidance raise but had the weakest performance against analyst estimates among its peers. The stock is down 1% since reporting and currently trades at $78.42.

Read our full, actionable report on Ollie's here, it’s free.

TJX (NYSE: TJX)

Initially based on a strategy of buying excess inventory from manufacturers or other retailers, TJX (NYSE: TJX) is an off-price retailer that sells brand-name apparel and other goods at prices much lower than department stores.

TJX reported revenues of $14.32 billion, up 9.2% year on year. This print beat analysts’ expectations by 2.4%. It was a very strong quarter as it also put up an impressive beat of analysts’ EBITDA and gross margin estimates.

The stock is up 6.2% since reporting and currently trades at $160.00.

Read our full, actionable report on TJX here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.