Atlassian has gotten torched over the last six months - since October 2025, its stock price has dropped 57.4% to $70.27 per share. This might have investors contemplating their next move.

Given the weaker price action, is this a buying opportunity for TEAM? Find out in our full research report, it’s free.

Why Does TEAM Stock Spark Debate?

Started by two Australian university friends who funded their startup with credit cards, Atlassian (NASDAQ: TEAM) provides software tools that help teams plan, track, collaborate, and share knowledge across organizations.

Two Positive Attributes:

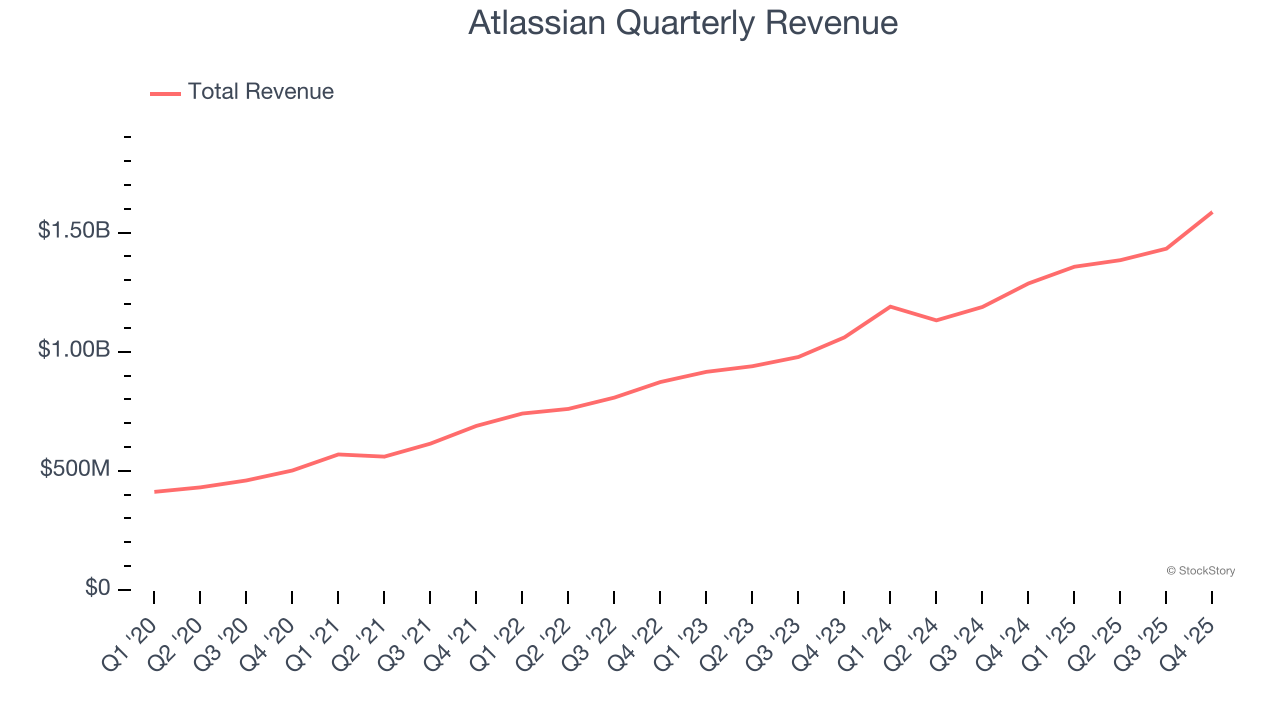

1. Long-Term Revenue Growth Shows Strong Momentum

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Atlassian’s 26.1% annualized revenue growth over the last five years was solid. Its growth beat the average software company and shows its offerings resonate with customers.

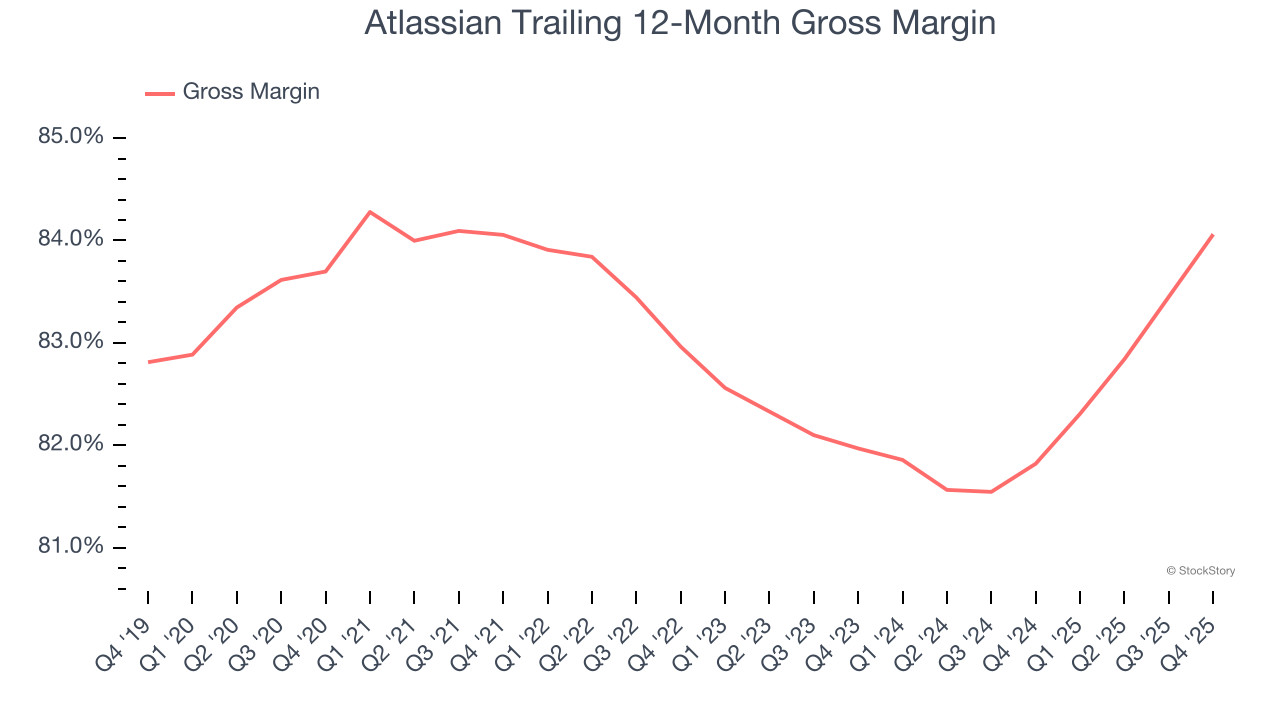

2. Elite Gross Margin Powers Best-In-Class Business Model

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Atlassian’s gross margin is one of the highest in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an elite 84.1% gross margin over the last year. Said differently, roughly $84.06 was left to spend on selling, marketing, and R&D for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Atlassian has seen gross margins improve by 2.1 percentage points over the last 2 year, which is solid in the software space.

One Reason to be Careful:

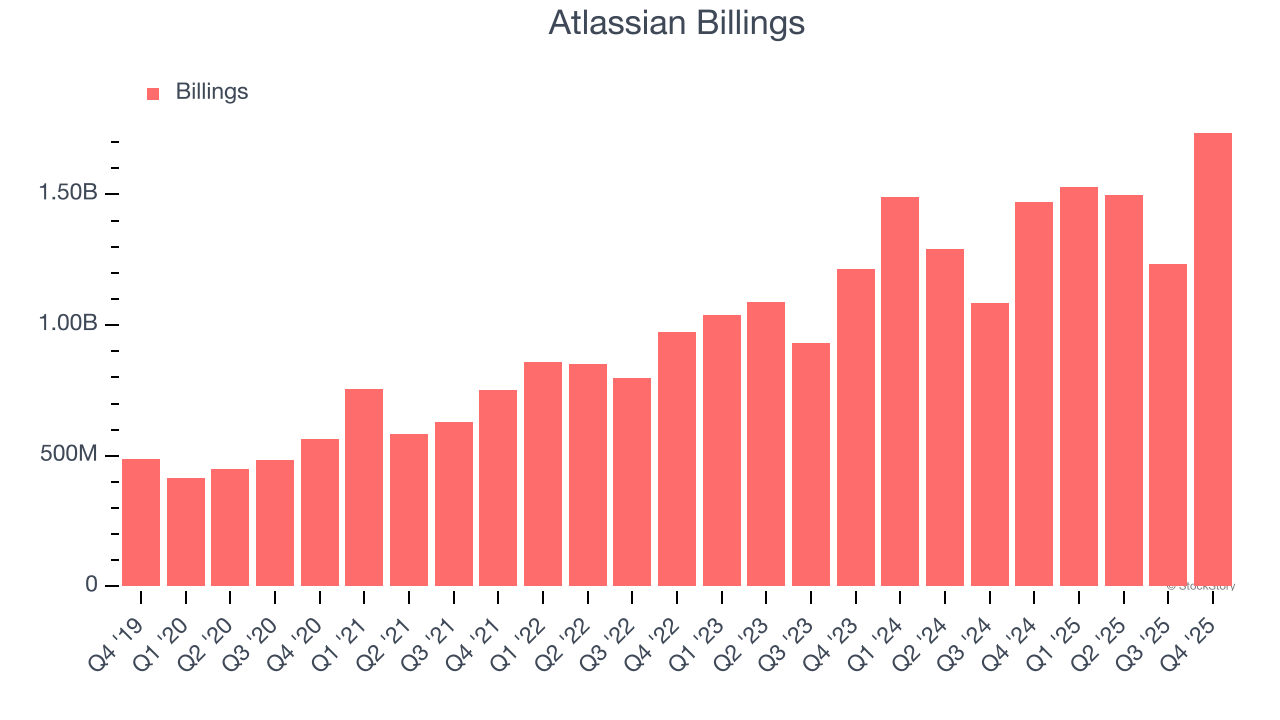

Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Atlassian’s billings came in at $1.74 billion in Q4, and over the last four quarters, its year-on-year growth averaged 12.5%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

Final Judgment

Atlassian’s positive characteristics outweigh the negatives. After the recent drawdown, the stock trades at 2.7× forward price-to-sales (or $70.27 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Atlassian

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.