Western Alliance Bancorporation’s stock price has taken a beating over the past six months, shedding 25.9% of its value and falling to $67.82 per share. This might have investors contemplating their next move.

Is there a buying opportunity in Western Alliance Bancorporation, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Western Alliance Bancorporation Not Exciting?

Even with the cheaper entry price, we're cautious about Western Alliance Bancorporation. Here are three reasons you should be careful with WAL and a stock we'd rather own.

1. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Western Alliance Bancorporation’s net interest income to drop by 2.5%, a decrease from its 19% annualized growth for the past two years. This projection is below its 19% annualized growth rate for the past two years.

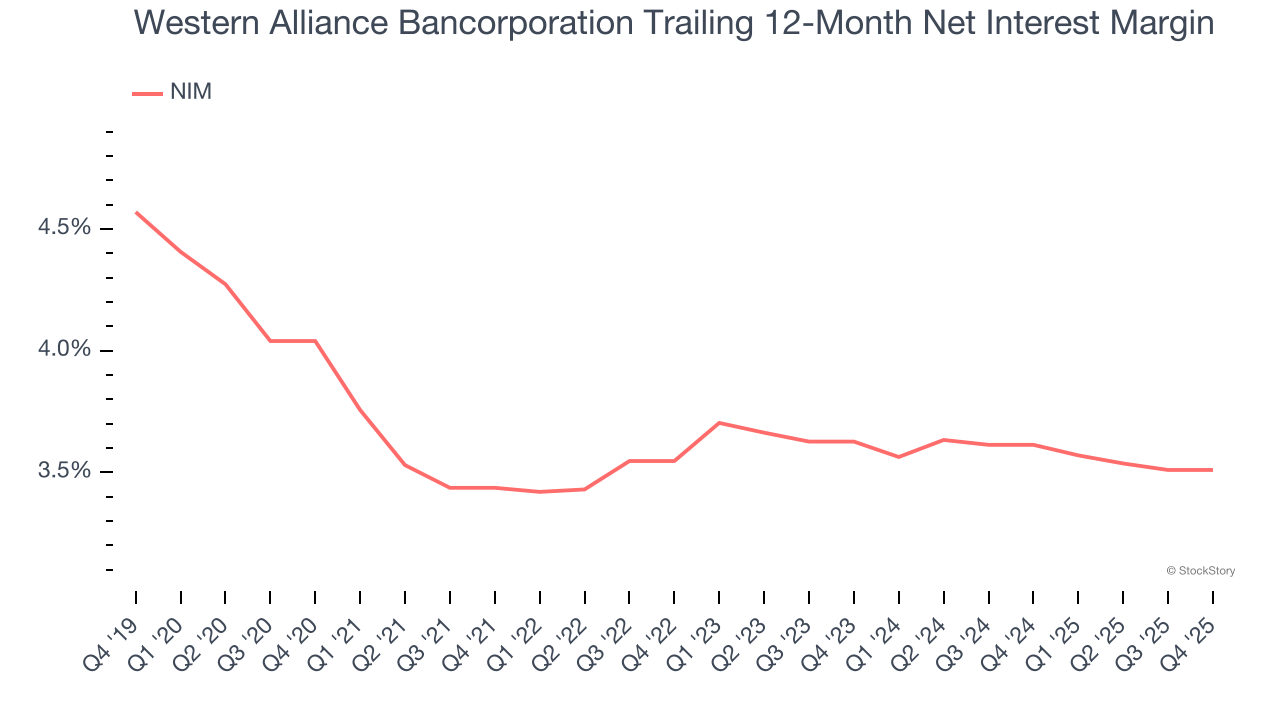

2. Net Interest Margin Dropping

Net interest margin (NIM) represents the unit economics of a bank by measuring the profitability of its interest-bearing assets relative to its interest-bearing liabilities. It's a fundamental metric that investors use to assess lending premiums and returns.

Over the past two years, Western Alliance Bancorporation’s net interest margin averaged 3.6%. However, its margin contracted by 11.7 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Western Alliance Bancorporation either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

Final Judgment

Western Alliance Bancorporation isn’t a terrible business, but it isn’t one of our picks. After the recent drawdown, the stock trades at 0.9× forward P/B (or $67.82 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at the most dominant software business in the world.

Stocks We Would Buy Instead of Western Alliance Bancorporation

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.