The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how productivity software stocks fared in Q3, starting with Dropbox (NASDAQ: DBX).

Rising employee costs and the shift to more remote work has increased the ever-present pressure to improve corporate productivity, which in turn has driven rising demand for productivity software that enables remote work, streamline project management and automate business tasks.

The 17 productivity software stocks we track reported a strong Q3. As a group, revenues beat analysts’ consensus estimates by 2.6% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 5.5% since the latest earnings results.

Dropbox (NASDAQ: DBX)

Originally named after the founders' tendency to "drop" files into a shared folder, Dropbox (NASDAQ: DBX) provides a content collaboration platform that helps individuals and teams store, organize, share, and work on files from anywhere.

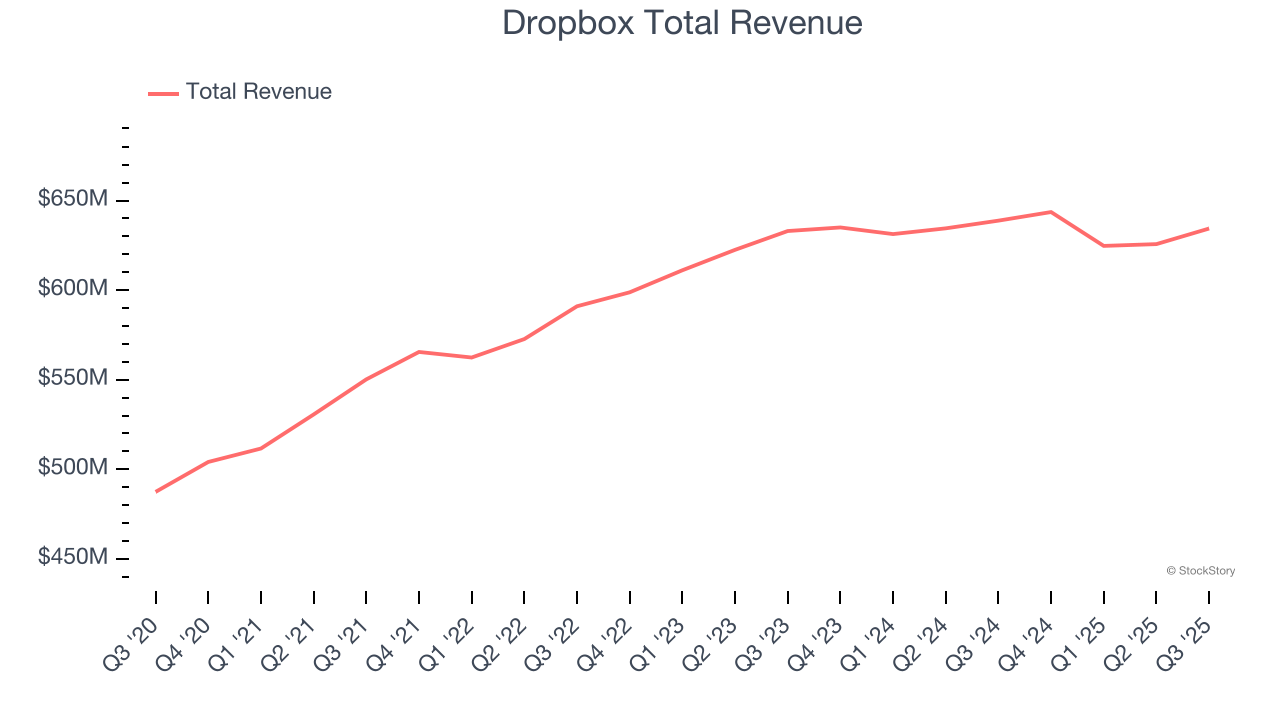

Dropbox reported revenues of $634.4 million, flat year on year. This print exceeded analysts’ expectations by 1.7%. Despite the top-line beat, it was still a mixed quarter for the company with a solid beat of analysts’ EBITDA estimates but decelerating customer growth.

Dropbox delivered the slowest revenue growth of the whole group. The company lost 60,000 customers and ended up with a total of 18.07 million. Unsurprisingly, the stock is down 6.1% since reporting and currently trades at $26.94.

Is now the time to buy Dropbox? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q3: Pegasystems (NASDAQ: PEGA)

With a "Center-out Business Architecture" approach that transcends organizational silos, Pegasystems (NASDAQ: PEGA) develops software that helps organizations automate workflows and use artificial intelligence to improve customer experiences and business processes.

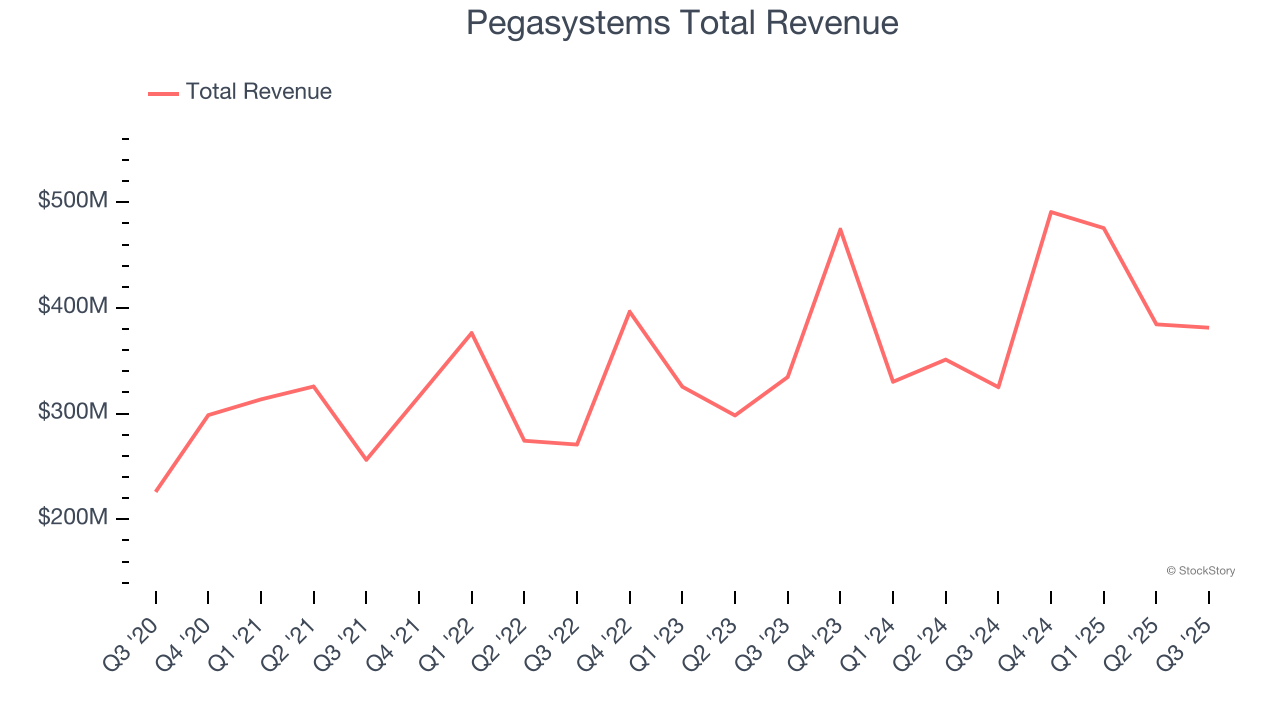

Pegasystems reported revenues of $381.4 million, up 17.3% year on year, outperforming analysts’ expectations by 8.5%. The business had a stunning quarter with an impressive beat of analysts’ billings estimates and a solid beat of analysts’ EBITDA estimates.

Pegasystems achieved the biggest analyst estimates beat among its peers. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $57.09.

Is now the time to buy Pegasystems? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: SoundHound AI (NASDAQ: SOUN)

Born from the idea that machines should understand human speech as naturally as people do, SoundHound AI (NASDAQ: SOUN) develops voice recognition and conversational intelligence technology that enables businesses to integrate voice assistants into their products and services.

SoundHound AI reported revenues of $42.05 million, up 67.6% year on year, exceeding analysts’ expectations by 2.7%. Still, it was a softer quarter as it posted a significant miss of analysts’ EBITDA and billings estimates.

As expected, the stock is down 26.1% since the results and currently trades at $10.61.

Read our full analysis of SoundHound AI’s results here.

Microsoft (NASDAQ: MSFT)

Originally named "Micro-soft" for microcomputer software when founded in 1975, Microsoft (NASDAQ: MSFT) is a global technology company that develops software, cloud services, devices, and AI solutions for consumers, businesses, and organizations worldwide.

Microsoft reported revenues of $77.67 billion, up 18.4% year on year. This print beat analysts’ expectations by 2.9%. It was a very strong quarter as it also produced a narrow beat of analysts’ revenue estimates, as the beat in Intelligent Cloud and Business Services trumped the miss in Personal Computing and a solid beat of analysts’ revenue estimates.

The stock is down 13% since reporting and currently trades at $473.29.

Read our full, actionable report on Microsoft here, it’s free for active Edge members.

Asana (NYSE: ASAN)

Born from the founders' frustration with the inefficiencies of email-based collaboration at Facebook, Asana (NYSE: ASAN) provides a work management platform that helps organizations track projects, set goals, and manage workflows in a centralized digital workspace.

Asana reported revenues of $201 million, up 9.3% year on year. This number topped analysts’ expectations by 1.1%. Overall, it was a strong quarter as it also put up EPS guidance for next quarter exceeding analysts’ expectations and a solid beat of analysts’ EBITDA estimates.

The company added 407 enterprise customers paying more than $5,000 annually to reach a total of 25,413. The stock is down 3.5% since reporting and currently trades at $12.97.

Read our full, actionable report on Asana here, it’s free for active Edge members.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.