What a brutal six months it’s been for Amplitude. The stock has dropped 21.5% and now trades at $9.91, rattling many shareholders. This might have investors contemplating their next move.

Is now the time to buy Amplitude, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Amplitude Will Underperform?

Despite the more favorable entry price, we're cautious about Amplitude. Here are three reasons you should be careful with AMPL and a stock we'd rather own.

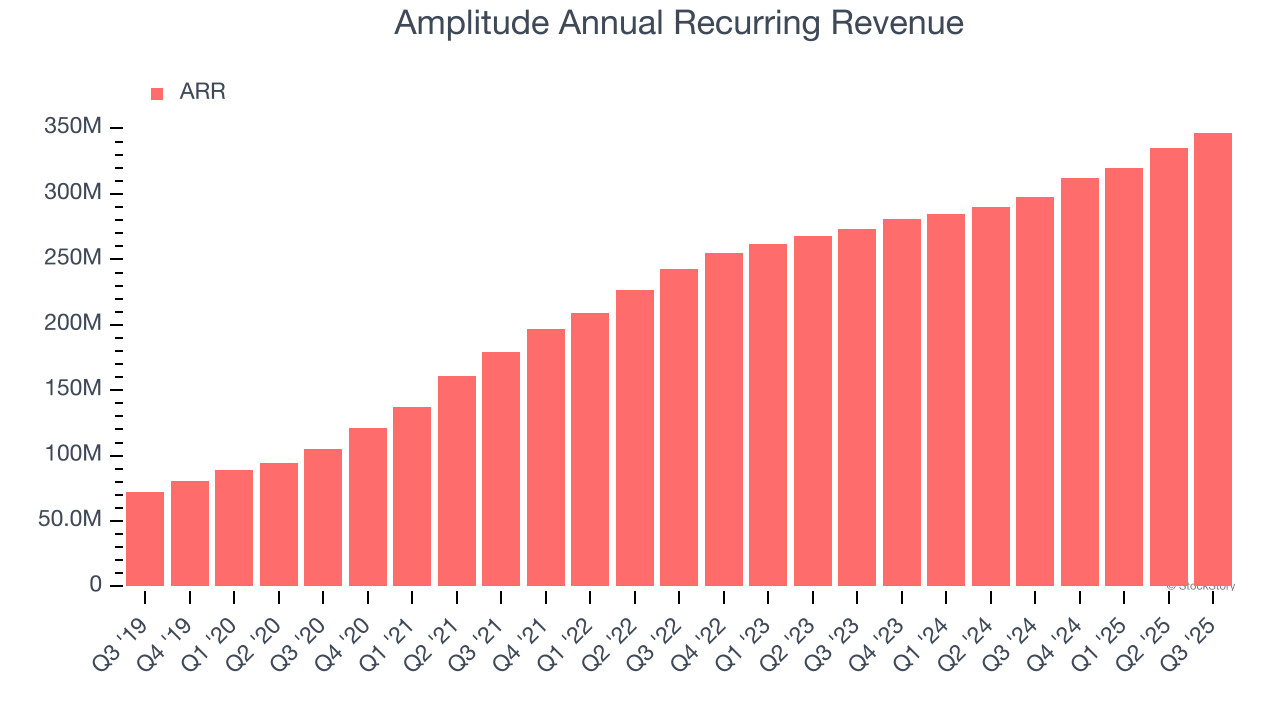

1. Weak ARR Points to Soft Demand

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Amplitude’s ARR came in at $347 million in Q3, and over the last four quarters, its year-on-year growth averaged 13.8%. This performance slightly lagged the sector and suggests that increasing competition is causing challenges in securing longer-term commitments.

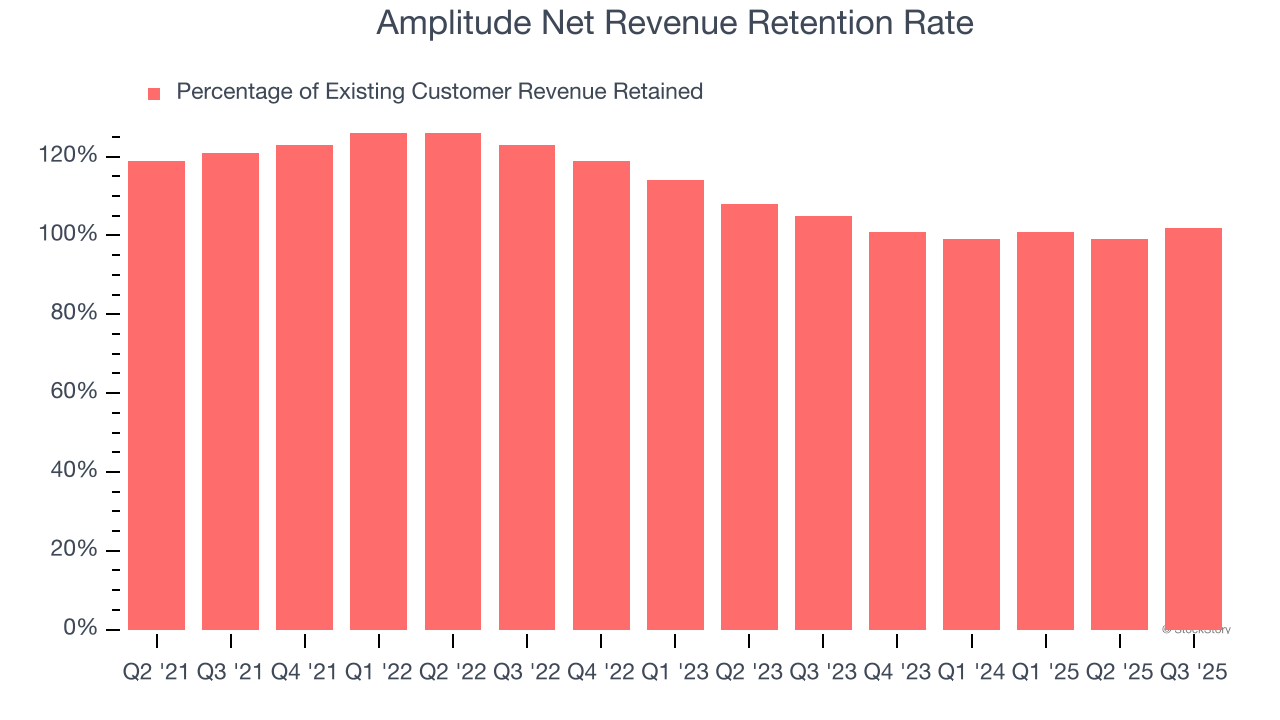

2. Customer Churn Hurts Long-Term Outlook

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Amplitude’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 101% in Q3. This means Amplitude would’ve grown its revenue by 0.7% even if it didn’t win any new customers over the last 12 months.

Amplitude has an adequate net retention rate, showing us that it generally keeps customers but lags behind the best SaaS businesses, which routinely post net retention rates of 120%+.

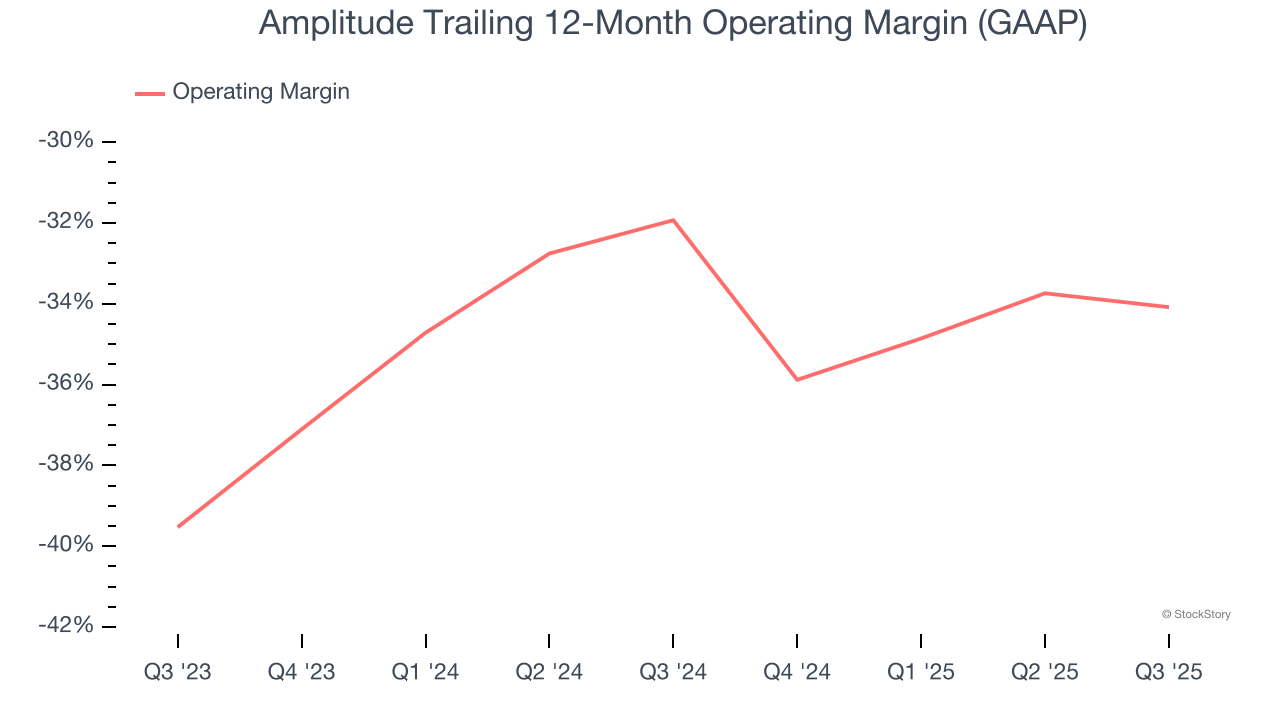

3. Shrinking Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Analyzing the trend in its profitability, Amplitude’s operating margin decreased by 2.2 percentage points over the last two years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Amplitude’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was negative 34.1%.

Final Judgment

Amplitude falls short of our quality standards. After the recent drawdown, the stock trades at 3.5× forward price-to-sales (or $9.91 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are more exciting stocks to buy at the moment. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Amplitude

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.