Over the last six months, Northwest Bancshares’s shares have sunk to $12.28, producing a disappointing 7.4% loss - a stark contrast to the S&P 500’s 10.1% gain. This may have investors wondering how to approach the situation.

Is now the time to buy Northwest Bancshares, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Northwest Bancshares Will Underperform?

Even though the stock has become cheaper, we're swiping left on Northwest Bancshares for now. Here are three reasons we avoid NWBI and a stock we'd rather own.

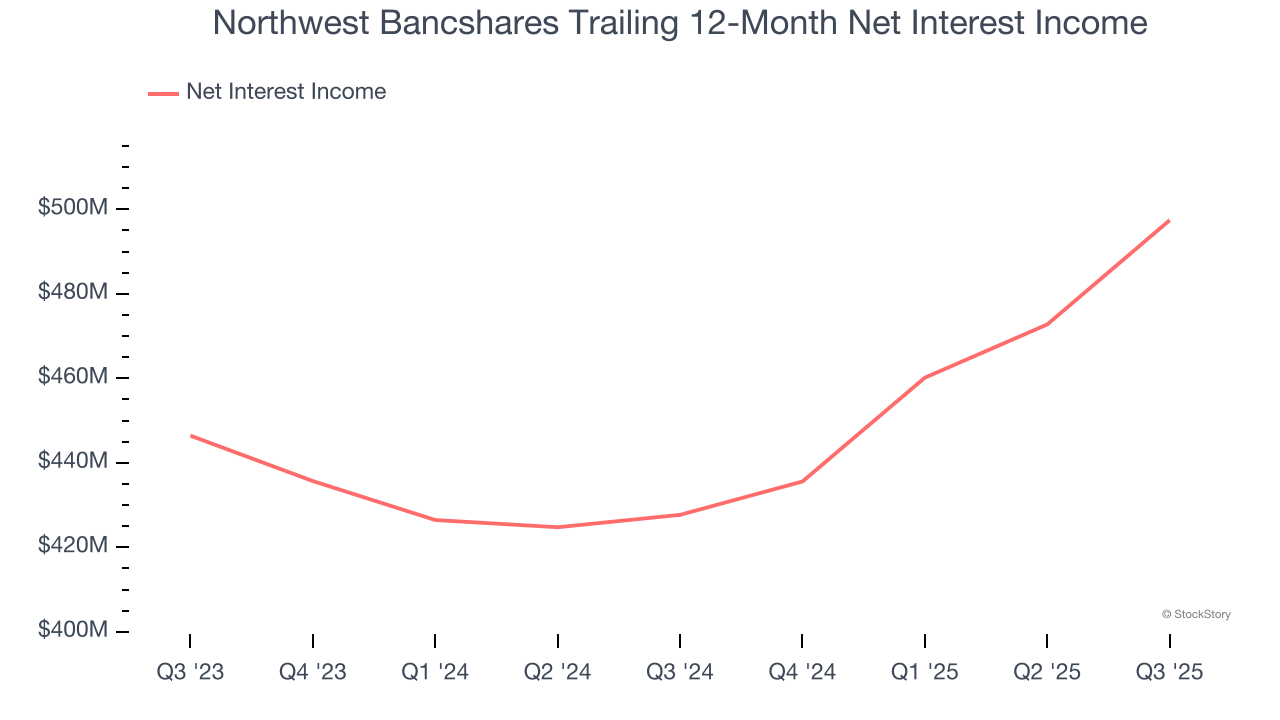

1. Net Interest Income Points to Soft Demand

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Northwest Bancshares’s net interest income has grown at a 5.7% annualized rate over the last five years, worse than the broader banking industry. Its growth was driven by both an increase in its outstanding loans and net interest margin, which represents how much a bank earns in relation to its outstanding loan book.

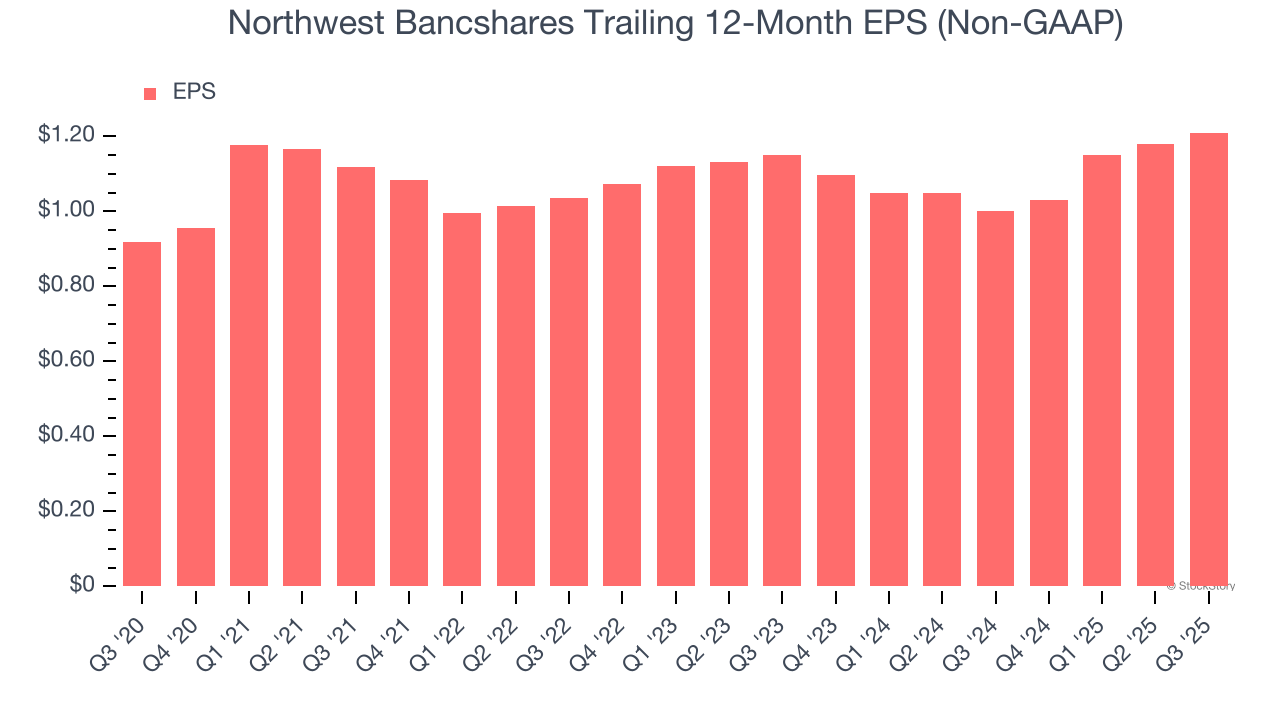

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Northwest Bancshares’s weak 5.7% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

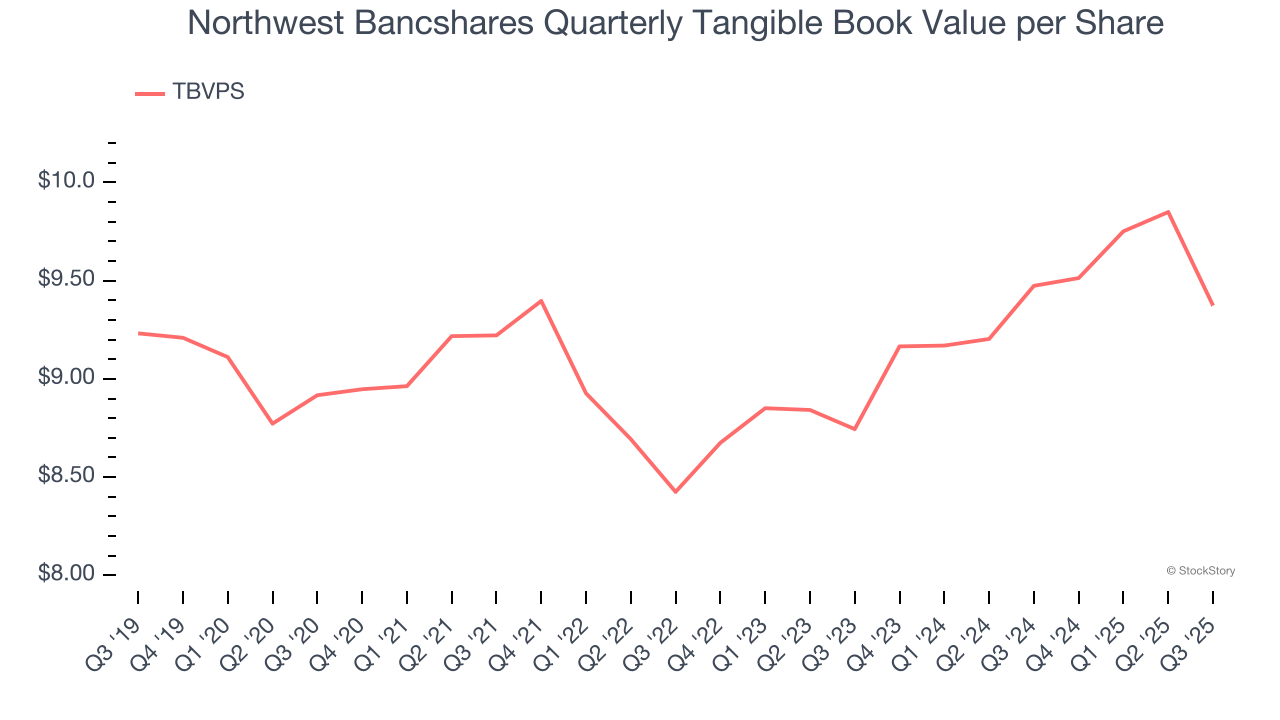

3. Substandard TBVPS Growth Indicates Limited Asset Expansion

In the banking industry, tangible book value per share (TBVPS) provides the clearest picture of shareholder value, as it focuses on concrete assets while excluding intangible items that may not hold value during challenging times.

To the detriment of investors, Northwest Bancshares’s TBVPS grew at a sluggish 3.5% annual clip over the last two years.

Final Judgment

Northwest Bancshares doesn’t pass our quality test. After the recent drawdown, the stock trades at 1× forward P/B (or $12.28 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better investments elsewhere. Let us point you toward one of our top digital advertising picks.

Stocks We Like More Than Northwest Bancshares

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.