Resideo trades at $24.07 and has moved in lockstep with the market. Its shares have returned 8.9% over the last six months while the S&P 500 has gained 7.6%.

Is there a buying opportunity in Resideo, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Resideo Not Exciting?

We're swiping left on Resideo for now. Here are three reasons why you should be careful with REZI and a stock we'd rather own.

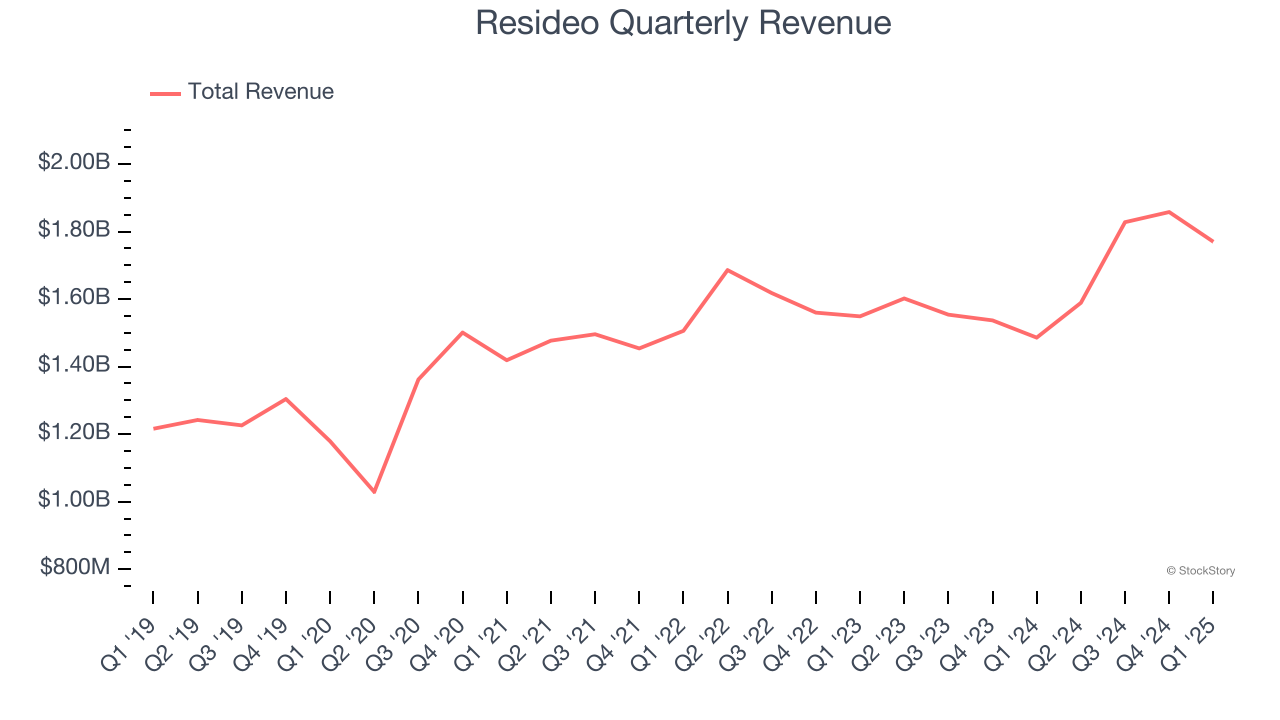

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Resideo’s 7.3% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the industrials sector.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Resideo’s revenue to rise by 4.4%, close to its 7.3% annualized growth for the past five years. This projection doesn't excite us and indicates its newer products and services will not catalyze better top-line performance yet.

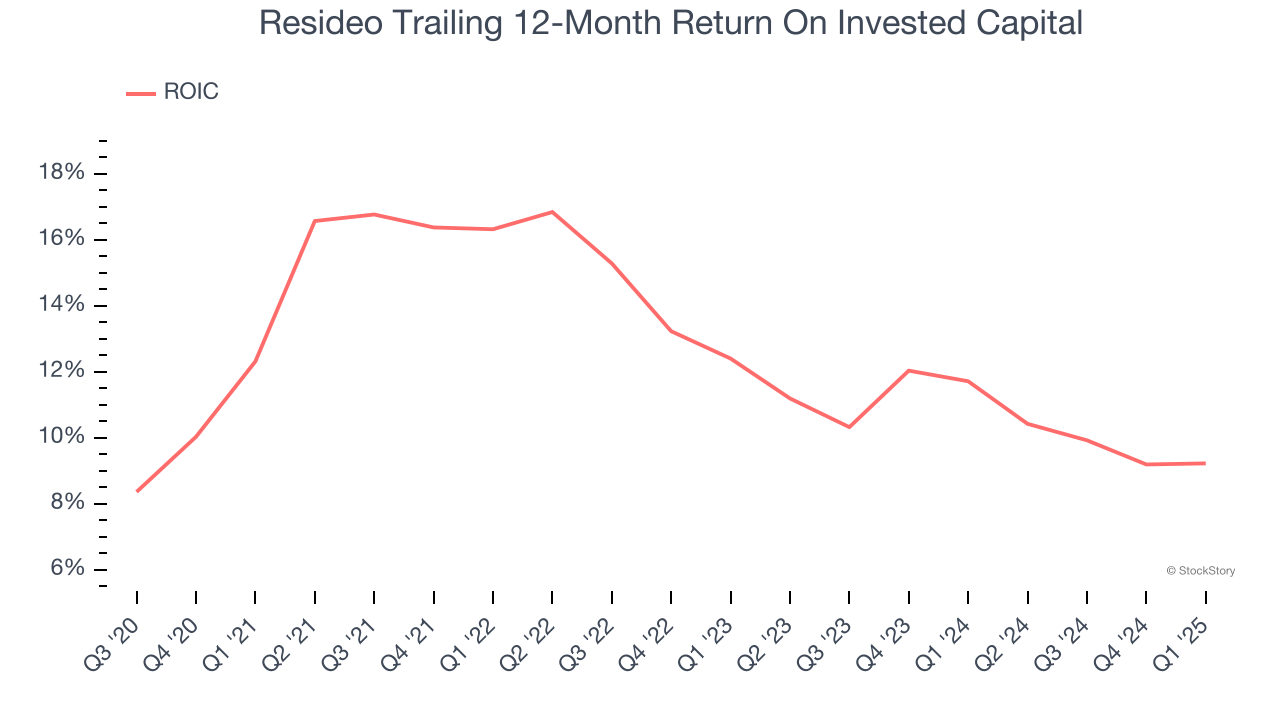

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Resideo’s ROIC averaged 3.8 percentage point decreases over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Resideo isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 5.9× forward EV-to-EBITDA (or $24.07 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. Let us point you toward one of our top digital advertising picks.

Stocks We Would Buy Instead of Resideo

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.