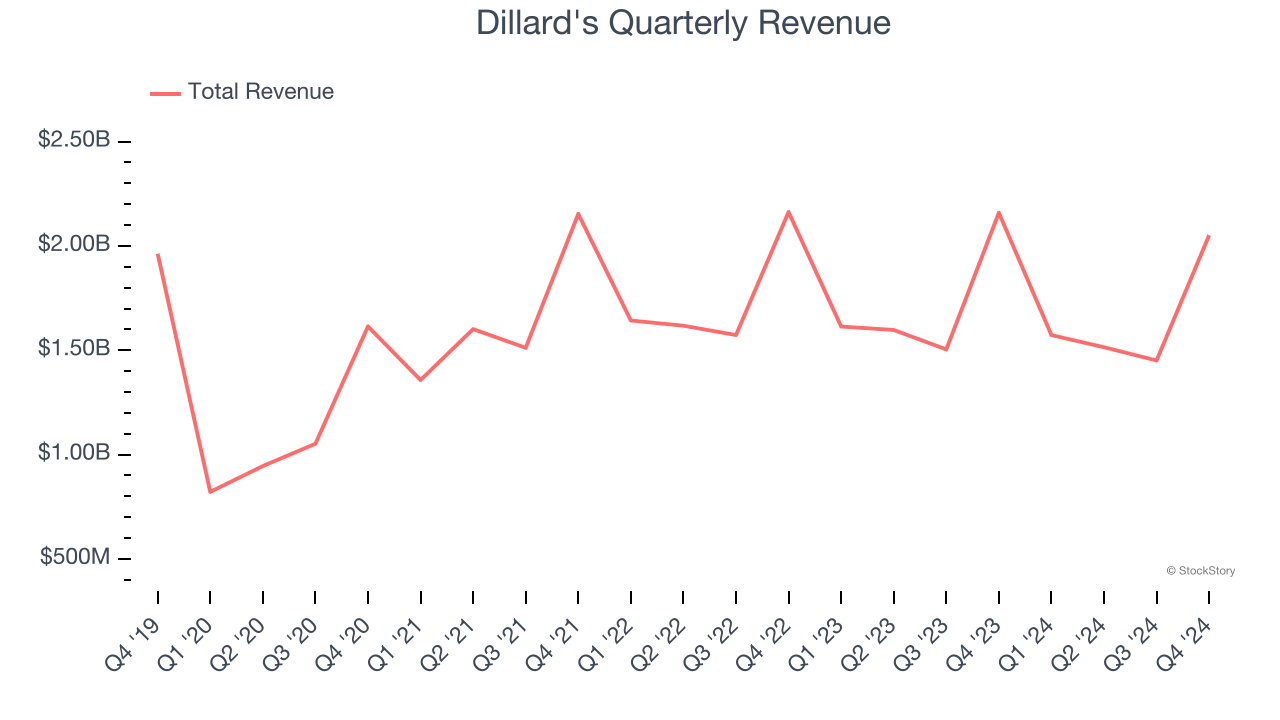

Department store chain Dillard’s (NYSE: DDS) beat Wall Street’s revenue expectations in Q4 CY2024, but sales fell by 5% year on year to $2.05 billion. Its GAAP profit of $13.48 per share was 37.2% above analysts’ consensus estimates.

Is now the time to buy Dillard's? Find out by accessing our full research report, it’s free.

Dillard's (DDS) Q4 CY2024 Highlights:

- Revenue: $2.05 billion vs analyst estimates of $2.03 billion (5% year-on-year decline, 1% beat)

- EPS (GAAP): $13.48 vs analyst estimates of $9.82 (37.2% beat)

- Adjusted EBITDA: $328.8 million vs analyst estimates of $257 million (16% margin, 27.9% beat)

- Operating Margin: 14%, in line with the same quarter last year

- Free Cash Flow Margin: 17%, down from 18.9% in the same quarter last year

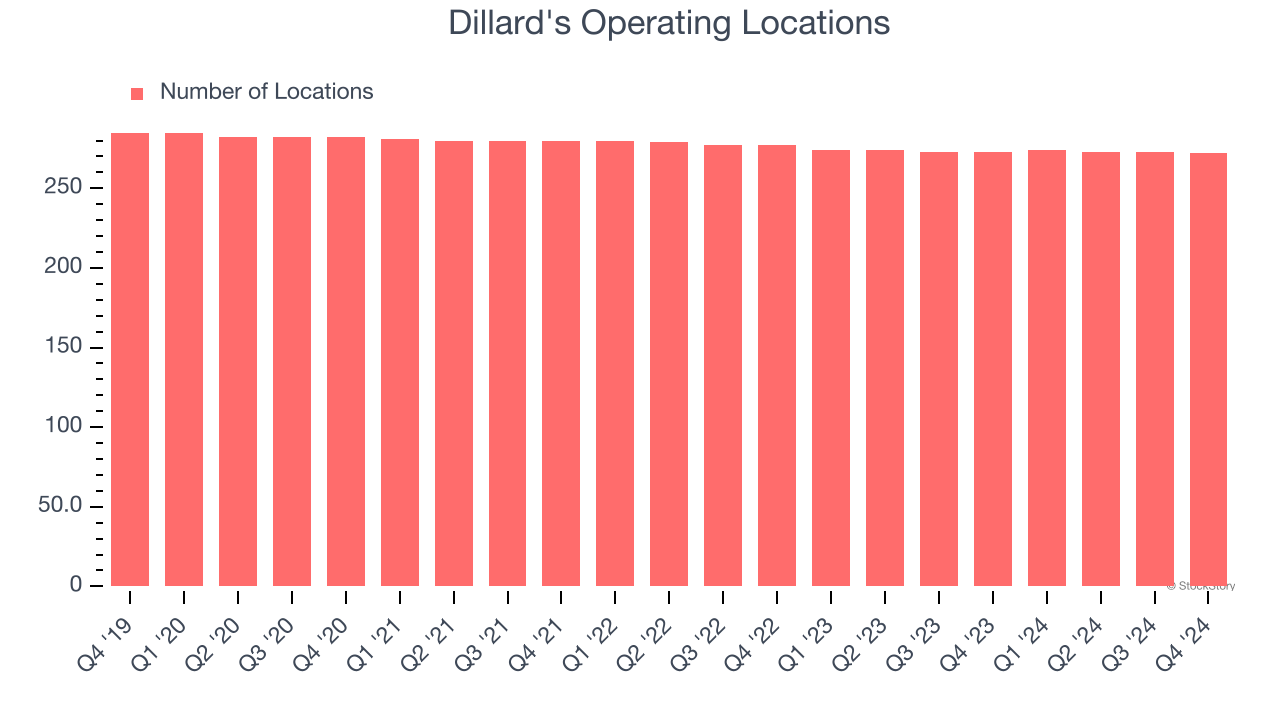

- Locations: 272 at quarter end, down from 273 in the same quarter last year

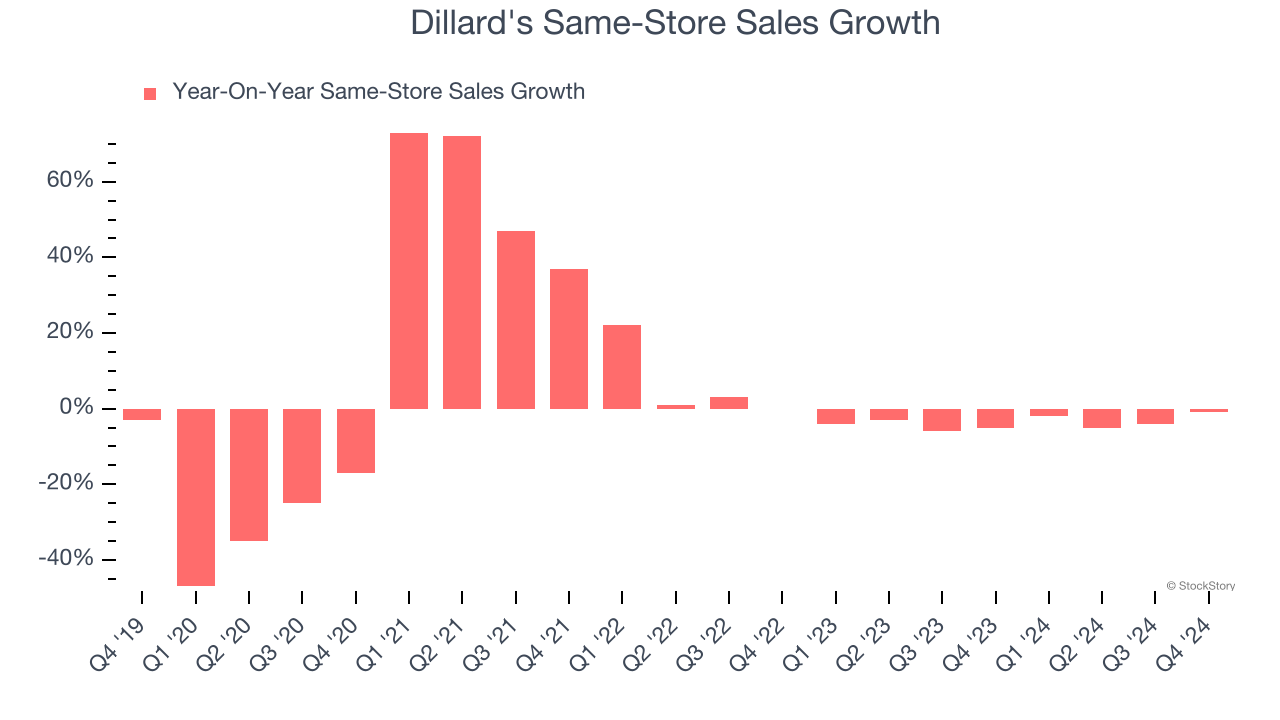

- Same-Store Sales fell 1% year on year (-5% in the same quarter last year)

- Market Capitalization: $7.64 billion

Company Overview

With stores located largely in the Southern and Western US, Dillard’s (NYSE: DDS) is a department store chain that sells clothing, cosmetics, accessories, and home goods.

Department Store

Department stores emerged in the 19th century to provide customers with a wide variety of merchandise under one roof, offering a convenient and luxurious shopping experience. They played an important role in the history of American retail and urbanization, and prior to department stores, retailers tended to sell narrow specialty and niche items. But what was once new is now old, and department stores are somewhat considered a relic of the past. They are being attacked from multiple angles–stagnant foot traffic at malls where they’ve served as anchors; more nimble off-price and fast-fashion retailers; and e-commerce-first competitors not burdened by large physical footprints.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years.

With $6.59 billion in revenue over the past 12 months, Dillard's is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Dillard's struggled to increase demand as its $6.59 billion of sales for the trailing 12 months was close to its revenue five years ago (we compare to 2019 to normalize for COVID-19 impacts). This was mainly because it didn’t open many new stores and observed lower sales at existing, established locations.

This quarter, Dillard’s revenue fell by 5% year on year to $2.05 billion but beat Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last five years. This projection is underwhelming and indicates its products will see some demand headwinds.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Dillard's listed 272 locations in the latest quarter and has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Dillard’s demand has been shrinking over the last two years as its same-store sales have averaged 3.8% annual declines. This performance isn’t ideal, and we’d be concerned if Dillard's starts opening new stores to artificially boost revenue growth.

In the latest quarter, Dillard’s same-store sales fell by 1% year on year. This decrease was an improvement from its historical levels. It’s always great to see a business’s demand trends improve.

Key Takeaways from Dillard’s Q4 Results

We were impressed by how significantly Dillard's blew past analysts’ EPS and EBITDA expectations this quarter. We were also excited its revenue outperformed. Zooming out, we think this quarter featured some important positives. The stock remained flat at $455.54 immediately after reporting.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.