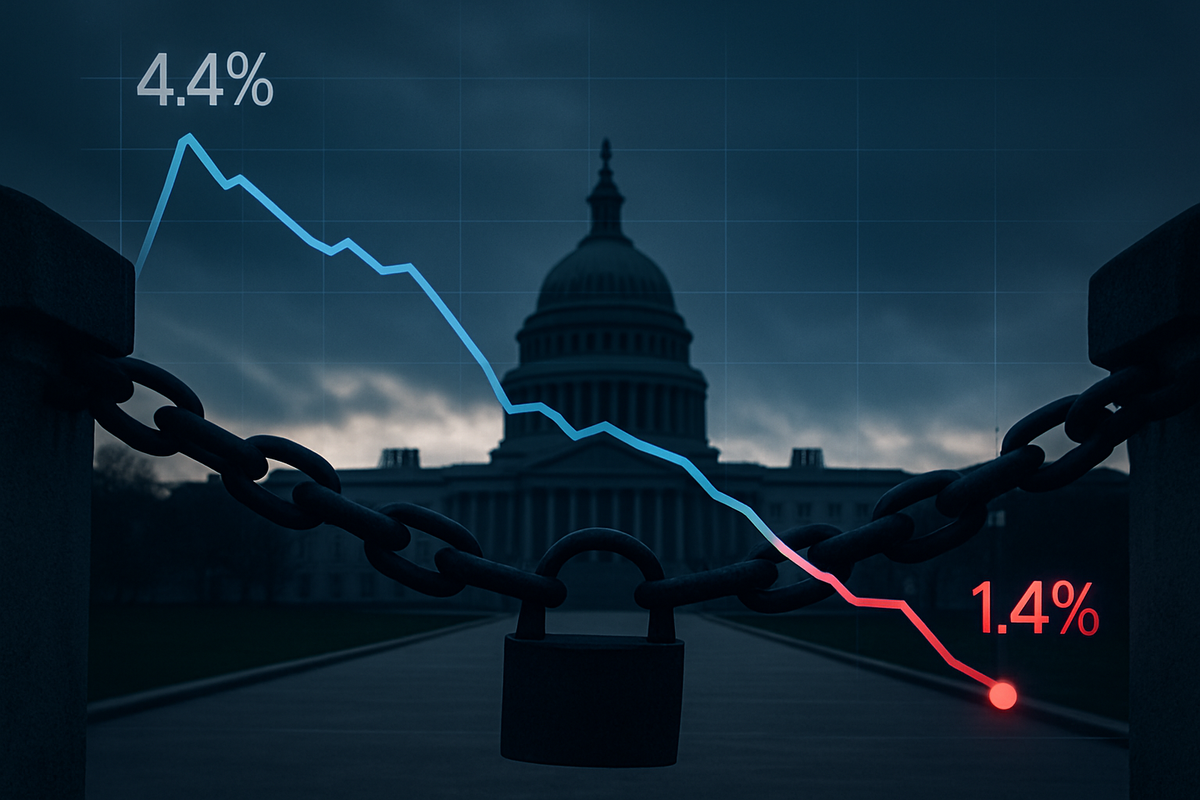

The United States economy hit a significant speed bump in the final months of 2025, as the Bureau of Economic Analysis (BEA) confirmed that fourth-quarter Gross Domestic Product (GDP) growth slowed to a tepid 1.4% annualized rate. This sharp deceleration marks a dramatic departure from the robust 4.4% growth recorded in the third quarter, signaling how quickly political instability can derail national economic momentum.

The primary culprit for this fiscal whiplash was the unprecedented 43-day federal government shutdown that paralyzed Washington from October 1 to November 12, 2025. As of today, March 31, 2026, economists are still untangling the full extent of the damage, but early consensus suggests that the "growth gap" created by the shutdown has permanently erased billions of dollars in economic output that may never be recovered.

The Longest Freeze in American History

The 43-day shutdown, triggered by a bitter congressional impasse over immigration reform and healthcare subsidies, surpassed the previous 35-day record set in 2018–2019. The BEA estimate indicates that the loss of federal government labor services alone subtracted roughly 1.0 percentage point from Q4 growth. When accounting for secondary effects—such as delayed government contracts and reduced consumer spending among federal workers—the Congressional Budget Office (CBO) suggests the total drag was closer to 1.5 percentage points.

During the height of the crisis, nearly 2 million active-duty military personnel and essential civilian employees were forced to work without pay, while hundreds of thousands of others were furloughed. The timeline of the event saw a complete cessation of non-essential government travel and the closure of national parks, which ripple-effected through the hospitality and service industries during the onset of the holiday season. Market reactions were initially volatile, with the S&P 500 experiencing a 6% pullback in October before stabilizing once a continuing resolution was finally signed in mid-November.

Corporate Fallout: Winners, Losers, and the Fragile Supply Chain

The defense sector bore a heavy burden during the 43-day impasse. While "prime" contractors like Lockheed Martin (NYSE: LMT) and RTX Corporation (NYSE: RTX) maintained stability due to massive backlogs and deep liquidity, the shutdown effectively froze the awarding of new contracts. This hit Research, Development, Test, and Evaluation (RDT&E) programs particularly hard. However, the true victims were the Tier 2 and Tier 3 small-business suppliers within the defense ecosystem, many of whom lacked the capital to survive nearly two months of payment delays, leading to lingering "supply chain snags" that are still being addressed in early 2026.

The travel industry also faced severe turbulence. Delta Air Lines (NYSE: DAL) and United Airlines Holdings (NASDAQ: UAL) reported operational strains as unpaid TSA agents and air traffic controllers faced staffing shortages. The FAA was forced to reduce flight frequencies at over 40 high-traffic airports, leading to thousands of cancellations. The U.S. Travel Association estimated a total economic loss of $6.1 billion for the sector during the shutdown period. Conversely, large-scale discount retailers like Walmart (NYSE: WMT) saw a minor "defensive" boost as furloughed workers and cautious consumers pivoted away from discretionary spending toward essential goods.

A Wider Significance: The Cost of Fiscal Fragility

This event fits into a broader, more concerning trend of "fiscal fragility" that has come to define the mid-2020s. The contrast between the Q3 growth of 4.4% and the Q4 growth of 1.4% highlights how sensitive a modern, high-tech economy is to administrative stability. Unlike the 16-day shutdown of 2013 or even the 35-day event in 2018, the 2025 shutdown occurred during a period of delicate transition for the Federal Reserve, complicating their efforts to manage interest rates without the aid of timely government data.

The regulatory implications are significant. Lawmakers are now facing renewed pressure to pass "automatic" funding triggers to prevent future shutdowns, though political polarization remains a formidable barrier. Historically, shutdowns have often been followed by a "snapback" in growth, but the 43-day duration of this event suggests that a portion of the $7 billion to $14 billion in lost productivity is gone forever. This serves as a stark reminder to investors that political risk is no longer a peripheral concern but a central component of macroeconomic forecasting.

The Road Ahead: Q1 2026 and Beyond

As we move through the first quarter of 2026, the market is looking for signs of a "springboard effect." Most analysts expect Q1 2026 GDP to show a rebound as backlogged federal spending is finally released into the economy. However, the shadow of the shutdown remains; many federal agencies are still playing catch-up on security clearances and permit processing, which could act as a lingering headwind for the construction and energy sectors.

The Federal Reserve is in a difficult position. The artificial dip in GDP growth complicates their read on inflation and employment. If the Fed interprets the 1.4% growth as a sign of underlying economic weakness rather than a temporary political glitch, they may be tempted to cut rates prematurely. Investors should watch for the upcoming "final" GDP revisions and the Fed’s next policy meeting in May for clues on how they intend to navigate this distorted data landscape.

Final Reflections for the Market

The descent from 4.4% to 1.4% growth is a sobering illustration of the high cost of political brinkmanship. While the U.S. consumer remains resilient, the 43-day shutdown of 2025 proved that the federal government is a vital cog in the economic engine that cannot be removed without immediate friction. The key takeaway for investors is the importance of diversification into sectors less reliant on federal appropriations and the necessity of pricing in "governance risk."

Moving forward, the market will be hyper-focused on the next round of budget negotiations. If Congress cannot find a permanent solution to the recurring funding crises, the "1.4% floor" seen in Q4 2025 may become a recurring nightmare for the American economy. For now, the watchword is cautious optimism, as the private sector attempts to reclaim the momentum lost during those 43 days of silence in Washington.

This content is intended for informational purposes only and is not financial advice.