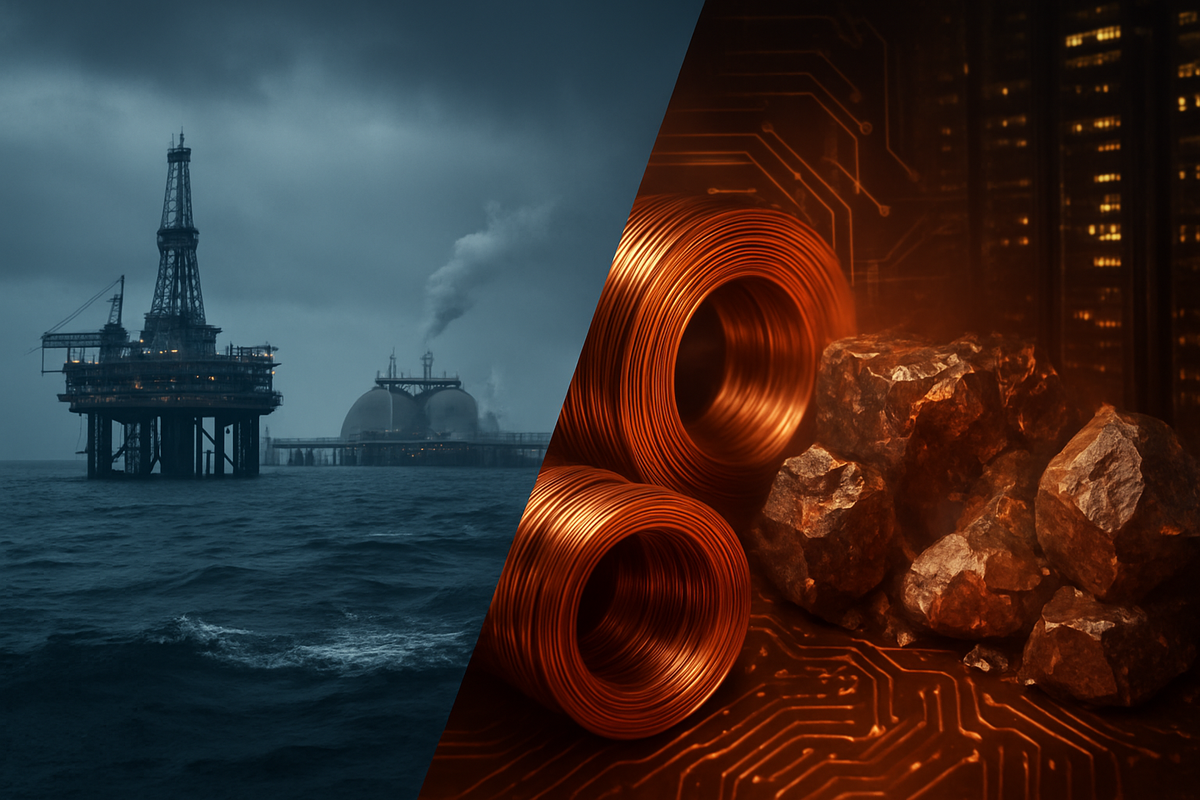

As the final trading days of 2025 unfold, the global commodities landscape is defined by a sharp contrast between a stabilizing energy sector and a record-breaking rally in industrial metals. Brent crude oil, which spent much of the fourth quarter under pressure, has staged a modest recovery to trade just above $61 a barrel, while European natural gas prices have ticked higher amid a late-December cold snap. These movements, however, are overshadowed by the extraordinary performance of the metals complex, where copper has cemented its status as the "new oil" in a year characterized by unprecedented demand from artificial intelligence infrastructure and the ongoing energy transition.

The divergence highlights a market in transition: while traditional fossil fuels grapple with a looming global surplus and shifting geopolitical dynamics, industrial metals are riding a wave of structural scarcity. For investors, the year-end roundup serves as a reminder that the "commodity supercycle" is no longer a monolith, but a fragmented landscape where technological innovation—specifically the massive power requirements of AI data centers—is now a primary driver of price discovery.

A Tale of Two Tides: Energy Recovery and Metal Records

The recent climb in Brent crude oil prices to approximately $61.95 per barrel marks a significant psychological floor for the energy market. After a bearish year that saw prices slide over 20% from their 2024 peaks, the late-December uptick is largely attributed to technical short-covering and a temporary tightening of physical supplies. This recovery comes despite a broader narrative of a "global oil surplus" projected for 2026, as production from the United States, Guyana, and Brazil continues to outpace stagnant demand growth in major economies.

Simultaneously, European benchmark gas prices, traded via the Dutch TTF hub, have risen to €28.49/MWh. This seasonal increase is driven by an Arctic weather front moving across Northern Europe, which has depleted storage levels more rapidly than in the previous two winters. While prices remain significantly lower than the crisis-era highs of 2022, the recent volatility underscores Europe’s continued sensitivity to global LNG dynamics. The market has been anchored by record-breaking U.S. LNG exports, which have grown by 25% year-over-year, acting as a crucial stabilizer for the continent's energy security.

The headline story of 2025, however, belongs to the metals sector. Copper prices on the London Metal Exchange (LME) breached the historic $12,000 per metric ton mark this month, capping a "banner year" in which the red metal surged nearly 40%. This rally was catalyzed by an "AI-driven demand shock," as the construction of massive new data centers required vast amounts of copper for electrical cabling and thermal management systems. This new demand source collided with a series of high-profile mine disruptions and chronically low global inventories, creating a perfect storm for price appreciation.

The Corporate Landscape: Mining Giants Surge as Energy Majors Pivot

The primary beneficiaries of the 2025 commodities shift have been the large-scale copper producers. Freeport-McMoRan (NYSE: FCX) has seen its valuation climb by nearly 30% this year, as its status as a premier pure-play copper producer made it a favorite for institutional investors seeking exposure to the AI infrastructure boom. Similarly, Rio Tinto (NYSE: RIO) has gained 33% year-to-date. While Rio Tinto's iron ore business faced headwinds from a slowing Chinese property sector, its aggressive expansion into copper—highlighted by its Simandou project and new Arizona partnerships—has more than offset those losses.

In the energy sector, the narrative has been one of disciplined capital management in a low-price environment. Shell (NYSE: SHEL) has emerged as the standout performer among the European "supermajors," outperforming its peers by roughly 7% this year. Shell’s strategy of focusing on high-margin fossil fuel assets while pragmatically slowing its rollout of lower-return renewable projects has resonated with shareholders. The company’s decision to halt several green hydrogen and biofuels projects in mid-2025 allowed it to maintain a robust share buyback program even as oil prices hovered in the $60 range.

Conversely, BP (NYSE: BP) has spent 2025 in a state of strategic realignment. Following a difficult start to the year, the company appointed Meg O’Neill as its new CEO in December, signaling a definitive pivot back toward its core oil and gas competencies. BP has begun divesting non-core solar and wind assets, such as its stake in Lightsource, to focus on the high-yield deepwater projects that investors are now demanding. While BP’s stock lagged for much of the year, it saw a 10% recovery in the final quarter as the market cheered its return to "financial prudence."

Broader Significance: The AI X-Factor and the New Geopolitics

The events of 2025 represent a fundamental shift in how commodities are valued. For decades, oil was the primary barometer of global economic health. Today, that title is increasingly shared with copper and other industrial metals like aluminum and silver. The "AI X-Factor" has introduced a new layer of demand that is less sensitive to traditional economic cycles and more tied to the pace of technological advancement. This shift has created a "banner year" for metals that mirrors the tech-led rallies of the early 2000s, but with a physical supply constraint that was not present in the software era.

Historically, a Brent price of $61 would have been viewed as a sign of global economic weakness. In the current context, however, it reflects a market that has successfully navigated the transition away from Russian supply and toward a more diversified, Western-led production base. The dominance of U.S. LNG in the European market has also shifted the geopolitical leverage, moving the needle away from traditional pipeline diplomacy and toward long-term maritime trade agreements.

Furthermore, the regulatory environment is beginning to catch up with these market realities. Governments in the U.S. and EU have accelerated permitting for critical mineral mines in 2025, recognizing that the "green transition" and the "AI revolution" are both contingent on a steady supply of metals. This policy shift is a direct response to the supply-side vulnerabilities exposed by this year's price spikes, marking a new era of "resource nationalism" where securing the supply chain is as important as the price of the commodity itself.

What Comes Next: 2026 and Beyond

Looking ahead to 2026, the primary challenge for the energy sector will be managing the anticipated supply surplus. With OPEC+ potentially unwinding voluntary production cuts and non-OPEC supply continuing to grow, Brent crude could face further downward pressure unless geopolitical tensions provide a new floor. Analysts are closely watching the $50.55 level as a potential support zone for the coming year. Energy companies will likely continue their trend of "capital discipline," prioritizing dividends and buybacks over aggressive production growth.

In the metals market, the question is whether the "banner year" of 2025 can be sustained. While the structural deficit in copper is expected to persist for the remainder of the decade, some cooling of the current rally is possible if high prices begin to trigger significant substitution or if the pace of data center construction slows. However, with silver also seeing a massive 128% year-to-date gain and gold trading near $4,500 an ounce, the precious and industrial metals complex remains the clear choice for momentum investors.

Strategic pivots will be required for companies that have not yet secured their long-term mineral supplies. We expect to see more "downstream-to-upstream" partnerships, where technology firms and automakers take direct equity stakes in mining projects to ensure they aren't left behind in the race for resources. This trend will likely blur the lines between the tech and commodity sectors even further in 2026.

Market Wrap-Up and Investor Outlook

The 2025 commodities roundup paints a picture of a market defined by resilience in energy and exuberance in metals. The stabilization of Brent crude near $61 and the seasonal rise in European gas prices suggest that the energy markets have found a temporary equilibrium, even as they face long-term structural challenges. Meanwhile, the record-shattering performance of copper and its industrial peers has redefined the "banner year," proving that the physical materials required for the digital age are now the most valuable assets in the global economy.

For investors, the key takeaway is the importance of sector selection within the commodities space. The era of "buying the index" is over; the focus must now be on pure-play producers like Freeport-McMoRan (NYSE: FCX) and diversified giants like Rio Tinto (NYSE: RIO) that are positioned to capture the AI and green energy tailwinds. In the energy sector, companies like Shell (NYSE: SHEL) that prioritize shareholder returns over speculative growth remain the safest bets in a low-price environment.

As we move into 2026, market participants should keep a close watch on global inventory levels and the pace of Fed rate cuts, which could further fuel industrial demand. The commodities market is no longer just about fueling our cars and heating our homes; it is about powering the intelligence of the future.

This content is intended for informational purposes only and is not financial advice.