Many founders only realize the importance of compliance requirements after a banking rejection when their US business bank application is already denied, even after completing LLC formation and EIN registration. At this stage, firms like James Baker & Associates often see clients who believed the setup process was complete, only to find that banks were actually assessing deeper compliance signals that were not properly prepared in advance.

The issue is not just paperwork or documentation; it is the hidden compliance layer that US banks review before approving any account. This includes ownership clarity, tax classification understanding, and business activity consistency, which many founders only discover once rejection has already occurred.

Why Banking Rejection Happens Even After LLC Approval

A common misunderstanding among international founders is that LLC formation equals business readiness. In reality, banking institutions apply a completely different evaluation system.

Banks focus on:

- Financial risk exposure

- Compliance readiness

- Identity verification consistency

- Business legitimacy signals

Even if your LLC is valid, rejection can still happen if compliance signals are weak or incomplete.

Key Insight: Banking approval is not based on registration status. It is based on how clearly your compliance structure is defined and verified.

This is why many founders only understand US compliance requirements after banking rejection, not before it.

The Gap Between LLC Formation and Banking Compliance Rules

The most critical issue is the timing mismatch between formation and compliance validation.

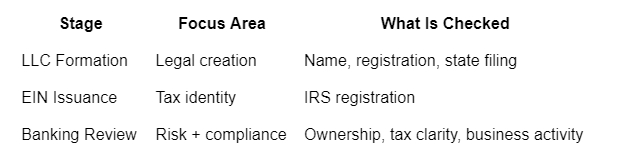

Comparison Table: LLC Setup vs Banking Review

This gap is where most founders face rejection because they assume legal formation automatically meets banking requirements.

It does not.

Banks evaluate deeper signals that are often ignored during early setup stages.

Core Compliance Requirements That Founders Miss

Many applicants only focus on incorporation and EIN, but compliance requirements after banking rejection usually point to missing foundational details.

1. Tax Classification and Reporting Clarity

Banks need to understand how your business is treated under US tax rules.

They evaluate:

- EIN verification

- Entity classification (LLC, disregarded entity, etc.)

- Reporting obligations under IRS guidelines

When this is unclear, the application appears incomplete.

Many founders working with US Tax Compliance Solutions discover that unclear tax classification is one of the most common rejection triggers.

2. Beneficial Ownership Transparency

US banks must identify the real individuals behind the company.

They review:

- Ownership percentage

- Control structure

- Identity verification documents

Even small inconsistencies between LLC documents and banking forms can create rejection signals.

3. Business Activity Description Weakness

A vague business description is one of the fastest ways to trigger rejection.

Examples of weak descriptions:

- “Online business”

- “Consulting services”

- “E-commerce activities”

Banks expect:

- Clear revenue source

- Product/service explanation

- Customer geography

- Transaction flow clarity

Without this, the application lacks credibility.

4. Cross-Border Compliance Alignment

Non-US founders often miss alignment between:

- Home country tax rules

- US reporting obligations

- Identity documentation consistency

Banks look for consistency across all submitted data.

If there is a mismatch, the system flags it as a compliance risk.

Why Founders Only Learn Compliance After Rejection

The main reason is simple: the compliance layer is invisible during formation.

Most founders follow this path:

- Form LLC

- Obtain EIN

- Apply for a bank account

- Face rejection

- Then discover compliance requirements

At step 4, the application feedback suddenly reveals gaps that were never explained earlier.

This is where founders begin searching for compliance requirements after banking rejection, trying to understand what went wrong.

Common Banking Rejection Reasons Explained

Below are the most frequent triggers that lead to rejection:

Numbered List of Key Issues:

- Incomplete ownership disclosure

- Weak or unclear business activity explanation

- Missing tax classification clarity

- Inconsistent identity or address data

- Lack of cross-border compliance alignment

Each of these signals increases perceived risk for banks.

Real-World Example of a Banking Rejection Scenario

A non-resident founder sets up a US LLC for a digital agency. Everything appears correct on paper.

However, the bank rejects the application because:

- The business description was too generic

- Ownership structure lacked clarity

- Tax classification was not properly explained

After reviewing the structure with advisors from James Baker & Associates, the founder updates documentation and resubmits.

This time, approval becomes more likely because compliance clarity has improved.

Compliance Checklist Before Submitting Banking Application

Before applying for a US business bank account, ensure the following:

- EIN is correctly issued and verified

- Ownership structure is clearly documented

- Business activity is specific and detailed

- Tax obligations are understood

- Identity documents match across all filings

- Cross-border compliance consistency is reviewed

This checklist helps reduce avoidable rejection cases.

How Banks Evaluate Risk Behind the Scenes

Banks not only read your application, but they run it through internal compliance filters.

They evaluate:

- Identity consistency across systems

- Business risk classification

- Transaction pattern expectations

- Regulatory compliance alignment

If anything appears unclear, the application is paused or rejected.

This is why many founders are surprised when rejection happens even with complete paperwork.

Practical Breakdown of Compliance Readiness

Step-by-Step View:

- Define your business model clearly

- Align ownership documents with EIN records

- Ensure tax classification is accurate

- Prepare consistent identity documentation

- Review business activity description in detail

- Validate cross-border compliance alignment

Each step reduces uncertainty during banking review.

Why Early Compliance Planning Matters

Most issues labeled as compliance requirements after banking rejection can actually be avoided before applying.

The key problem is not lack of eligibility; it is lack of clarity.

Banks want to understand:

- Who you are

- What your business does

- How money flows

- Whether reporting is clear and consistent

When these answers are unclear, rejection becomes likely.

Key Insight for Founders

Banking rejection is rarely about the LLC itself; it is about how clearly your compliance structure is presented and verified.

Understanding this shift changes how you prepare your application.

Conclusion

Most founders only discover compliance requirements after banking rejection because they assume LLC formation and EIN issuance complete the setup process. In reality, banking approval depends on how clearly your tax structure, ownership details, and business activity are defined.

When these elements are aligned before submission, rejection risk reduces significantly, and the approval process becomes more predictable.

Working with advisory teams like James Baker & Associates or US Tax Compliance Solutions helps ensure compliance clarity is addressed early rather than after rejection.

FAQ

1. Why do US banks reject LLC applications after approval of formation?

US banks reject applications when compliance details such as ownership structure, tax classification, or business activity are unclear. These factors affect risk evaluation, even if the LLC is legally formed and active.

2. What is the most common compliance issue found after rejection?

The most common issue is an unclear business activity description. Banks need a precise explanation of revenue sources, customers, and transaction flow to assess legitimacy and financial risk accurately.

3. Does having an EIN guarantee bank account approval?

No, an EIN only confirms tax registration with the IRS. Banks evaluate broader compliance factors, including ownership clarity, documentation consistency, and cross-border alignment, before approving applications.

4. How can founders avoid banking rejection?

Founders can avoid rejection by clearly defining business activities, aligning ownership documents, ensuring tax classification accuracy, and maintaining consistent identity information across all legal and financial records.

5. When should compliance be reviewed in the setup process?

Compliance should be reviewed before submitting any banking application, not after LLC formation. Early review ensures documentation consistency and reduces the risk of rejection during bank evaluation.