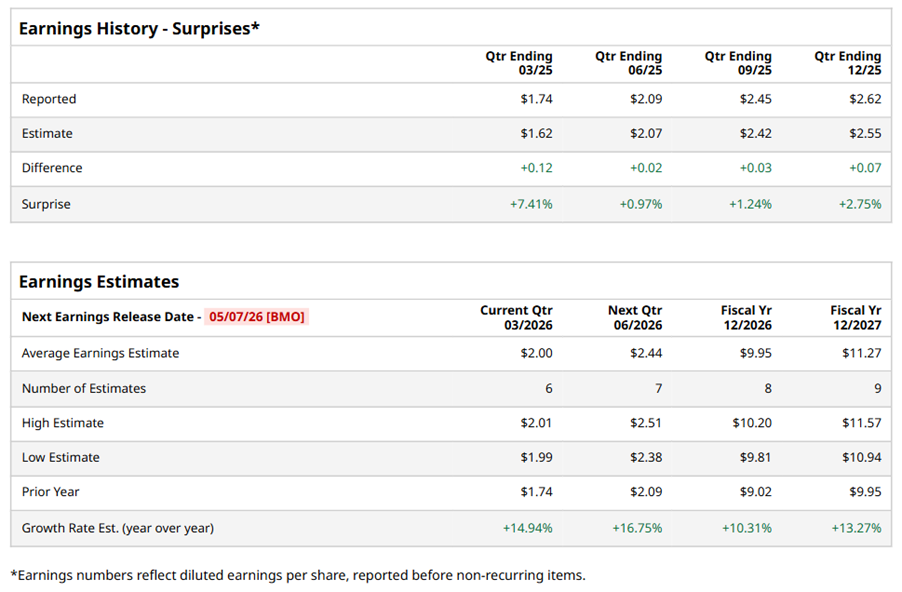

EPAM Systems, Inc. (EPAM), headquartered in Newtown, Pennsylvania, offers digital platform engineering and software development services. Valued at $6.9 billion by market cap, the company provides software development, outsourcing services, e-business, enterprise relationship management, and content management solutions. The IT services giant is expected to announce its fiscal first-quarter earnings for 2026 before the market opens on Thursday, May 7.

Ahead of the event, analysts expect EPAM to report a profit of $2 per share on a diluted basis, up 14.9% from $1.74 per share in the year-ago quarter. The company has consistently surpassed Wall Street’s EPS estimates in its last four quarterly reports.

For the full year, analysts expect EPAM to report EPS of $9.95, up 10.3% from $9.02 in fiscal 2025. Its EPS is expected to rise 13.3% year over year to $11.27 in fiscal 2027.

EPAM stock has notably underperformed the S&P 500 Index’s ($SPX) 34.9% gains over the past 52 weeks, with shares down 10.8% during this period. Similarly, it considerably underperformed the State Street Technology Select Sector SPDR ETF’s (XLK) 60.1% gains over the same time frame.

EPAM stock remains under pressure due to sector-wide technology weakness and investor concerns regarding AI’s impact on the IT services model. The slide worsened following its Q4 results, when below-consensus guidance and issues with key clients spooked investors, driving shares down 17% in a day. Furthermore, its near-term profitability is also squeezed as EPAM ramps pay and spends heavily to deepen vertical specialization and strengthen sales execution.

Analysts’ consensus opinion on EPAM stock is reasonably bullish, with an overall “Moderate Buy” rating. Out of 18 analysts covering the stock, 10 advise a “Strong Buy” rating, one suggests a “Moderate Buy,” and seven give a “Hold.” EPAM’s average analyst price target is $190.62, indicating an ambitious potential upside of 45.1% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Fighting for the 25th Hour: The Biological Limits of Netflix’s Expansion

- Trump Sends Compass Pathways Stock Soaring as He Backs Psychedelics. Should You Buy CMPS Here?

- As Oracle Launches New Agentic AI Tools, Should You Buy, Sell, or Hold ORCL Stock?

- Is GOOG Stock a Buy Ahead of Q1 Earnings and Amid Fragile Peace in the Middle East?