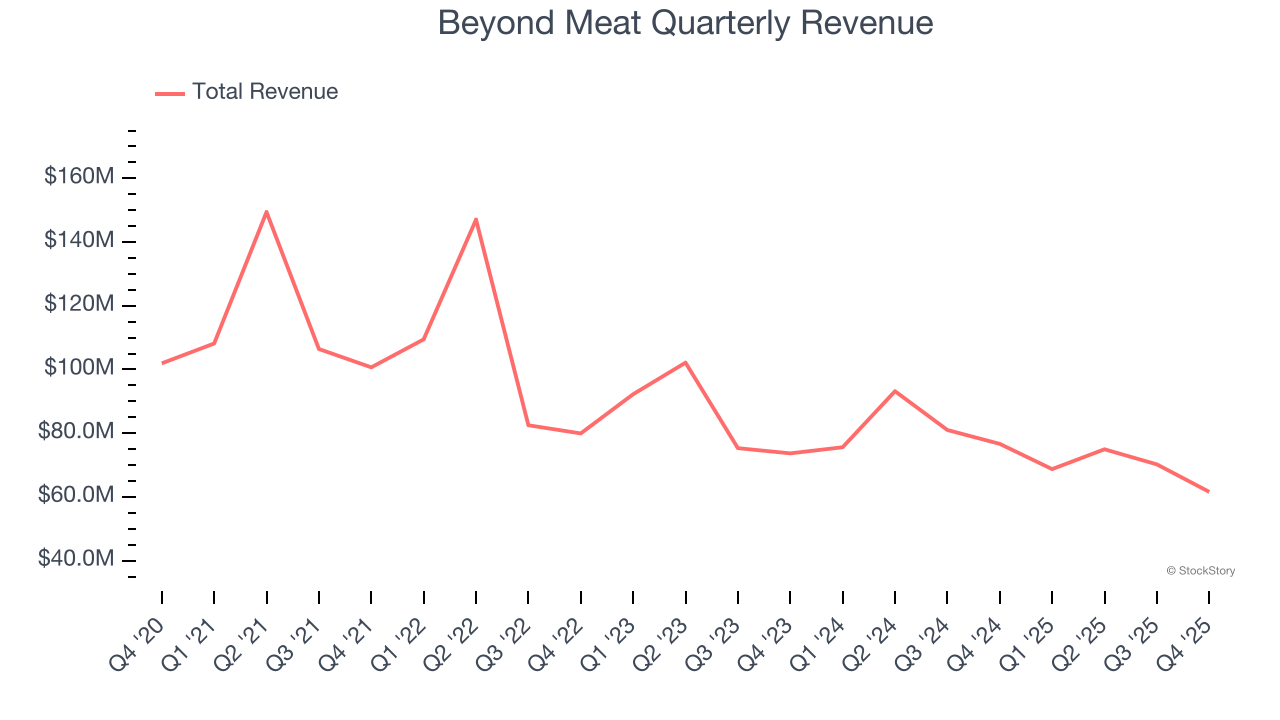

Plant-based protein company Beyond Meat (NASDAQ: BYND) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 19.7% year on year to $61.59 million. Next quarter’s revenue guidance of $58 million underwhelmed, coming in 13.1% below analysts’ estimates. Its GAAP loss of $0.29 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Beyond Meat? Find out by accessing our full research report, it’s free.

Beyond Meat (BYND) Q4 CY2025 Highlights:

- Revenue: $61.59 million vs analyst estimates of $62.77 million (19.7% year-on-year decline, 1.9% miss)

- EPS (GAAP): -$0.29 vs analyst estimates of -$0.08 (significant miss)

- Adjusted EBITDA: -$69.05 million (-112% margin, 166% year-on-year decline)

- Revenue Guidance for Q1 CY2026 is $58 million at the midpoint, below analyst estimates of $66.75 million

- Operating Margin: -216%, down from -49.3% in the same quarter last year

- Free Cash Flow was -$49.77 million compared to -$35.43 million in the same quarter last year

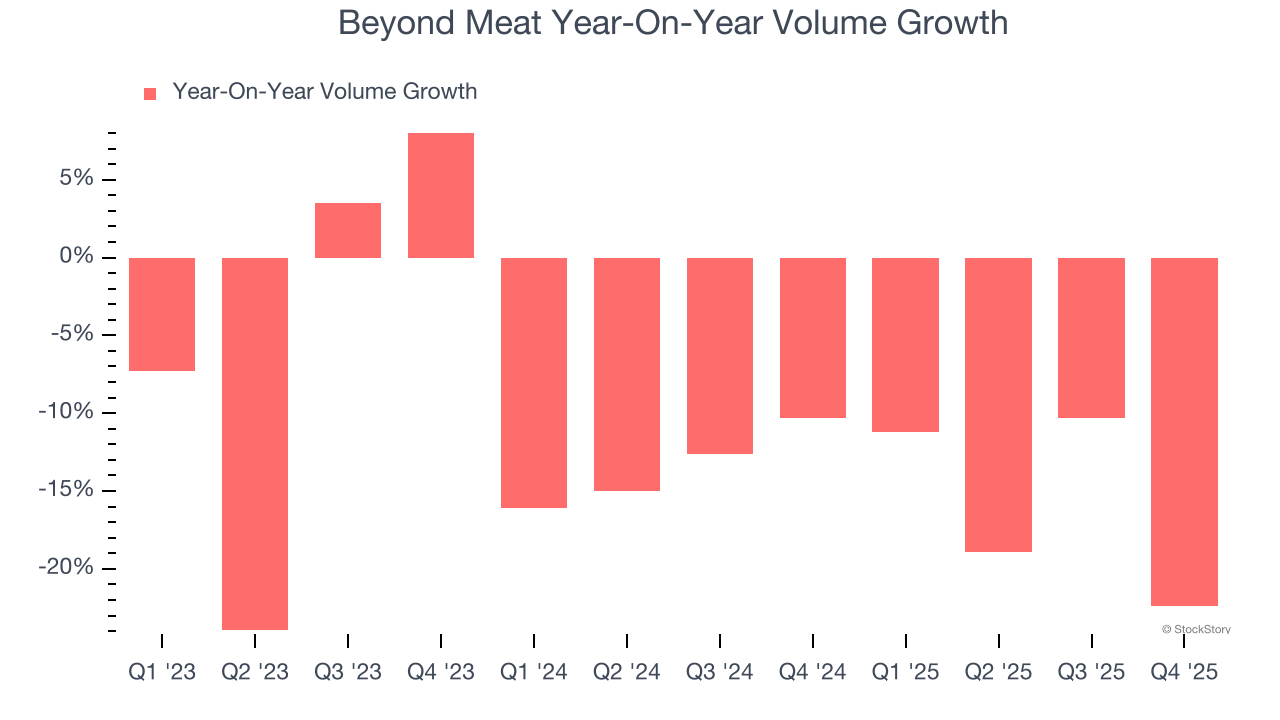

- Sales Volumes fell 22.4% year on year (-10.3% in the same quarter last year)

- Market Capitalization: $276.6 million

Company Overview

A pioneer at the forefront of the plant-based protein revolution, Beyond Meat (NASDAQ: BYND) is a food company specializing in alternatives to traditional meat products.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $275.5 million in revenue over the past 12 months, Beyond Meat is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Beyond Meat’s revenue declined by 13% per year over the last three years as consumers bought less of its products.

This quarter, Beyond Meat missed Wall Street’s estimates and reported a rather uninspiring 19.7% year-on-year revenue decline, generating $61.59 million of revenue. Company management is currently guiding for a 15.6% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection implies its newer products will fuel better top-line performance, it is still below the sector average.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Beyond Meat’s average quarterly sales volumes have shrunk by 14.6% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

In Beyond Meat’s Q4 2025, sales volumes dropped 22.4% year on year. This result represents a further deceleration from its historical levels, showing the business is struggling to move its products.

Key Takeaways from Beyond Meat’s Q4 Results

We struggled to find many positives in these results. Its revenue guidance for next quarter missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 6.7% to $0.67 immediately after reporting.

Beyond Meat didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).