The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how defense contractors stocks fared in Q2, starting with Huntington Ingalls (NYSE: HII).

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

The 14 defense contractors stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 3.3% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 8.3% on average since the latest earnings results.

Huntington Ingalls (NYSE: HII)

Building Nimitz-class aircraft carriers used in active service, Huntington Ingalls (NYSE: HII) develops marine vessels and their mission systems and maintenance services.

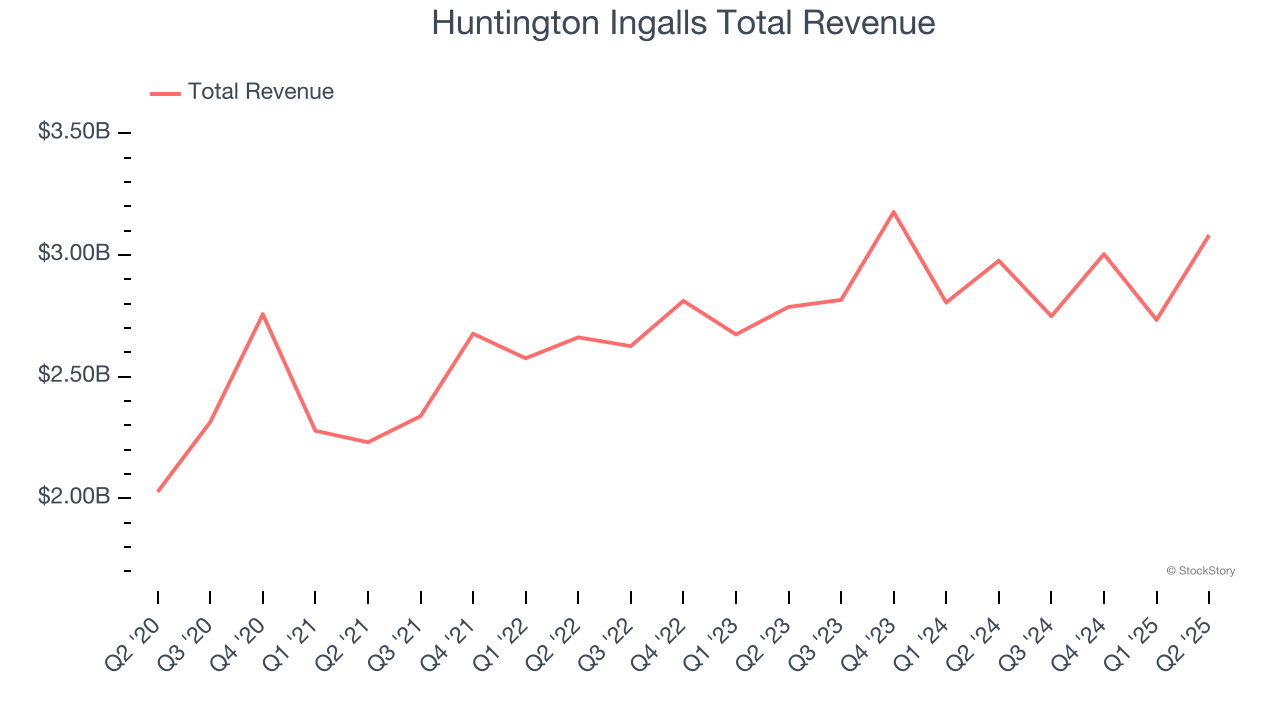

Huntington Ingalls reported revenues of $3.08 billion, up 3.5% year on year. This print exceeded analysts’ expectations by 5.5%. Overall, it was a strong quarter for the company with a solid beat of analysts’ EBITDA estimates and a beat of analysts’ EPS estimates.

“Second quarter results were largely in line with our expectations as we continue to make steady progress on our operational initiatives for 2025. We have seen early signs that targeted investments are helping to stabilize the workforce and supply chain, in support of the broader maritime industrial base," said Chris Kastner, HII’s president and CEO.

Interestingly, the stock is up 6.8% since reporting and currently trades at $276.25.

Is now the time to buy Huntington Ingalls? Access our full analysis of the earnings results here, it’s free.

Best Q2: Mercury Systems (NASDAQ: MRCY)

Founded in 1981, Mercury Systems (NASDAQ: MRCY) specializes in providing processing subsystems and components for primarily defense applications.

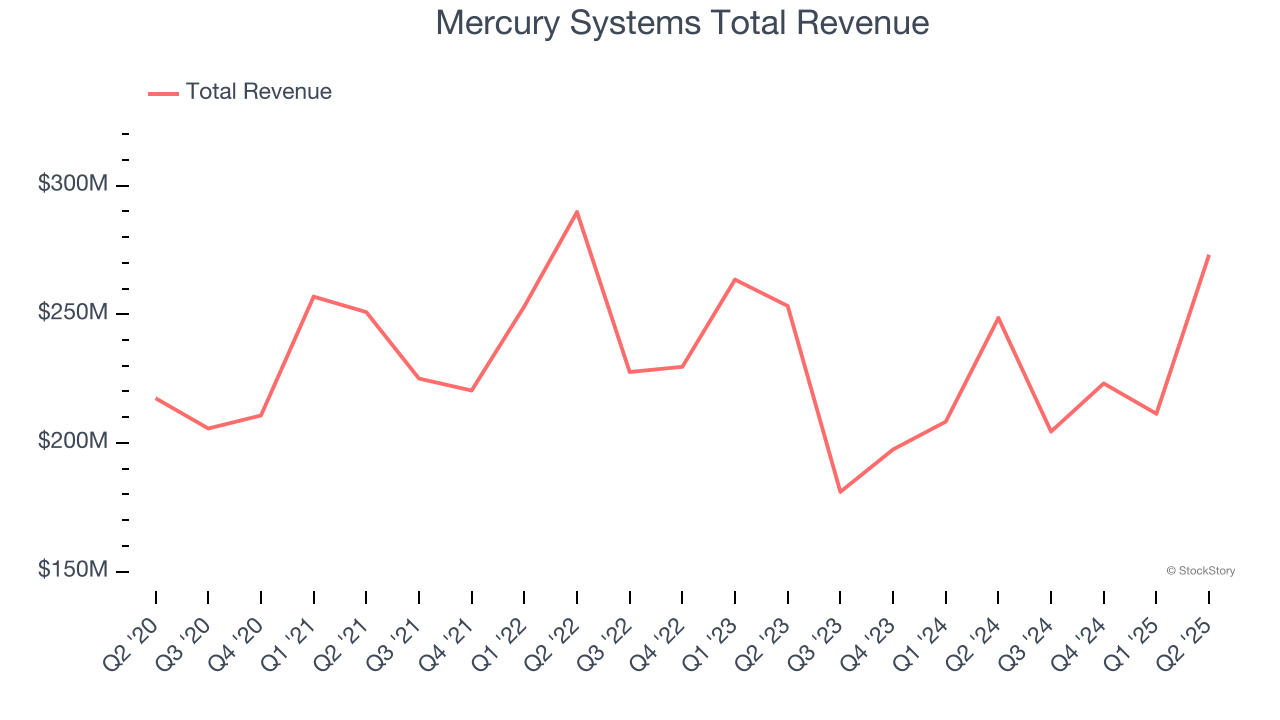

Mercury Systems reported revenues of $273.1 million, up 9.9% year on year, outperforming analysts’ expectations by 11.9%. The business had an incredible quarter with an impressive beat of analysts’ organic revenue and EPS estimates.

The market seems happy with the results as the stock is up 36.8% since reporting. It currently trades at $73.48.

Is now the time to buy Mercury Systems? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Lockheed Martin (NYSE: LMT)

Headquartered in Maryland, Famous for the F-35 aircraft, Lockheed Martin (NYSE: LMT) specializes in defense, space, homeland security, and information technology products.

Lockheed Martin reported revenues of $18.16 billion, flat year on year, falling short of analysts’ expectations by 2.3%. It was a softer quarter as it posted full-year EPS guidance missing analysts’ expectations and a significant miss of analysts’ adjusted operating income estimates.

Interestingly, the stock is up 1.9% since the results and currently trades at $470.19.

Read our full analysis of Lockheed Martin’s results here.

CACI (NYSE: CACI)

Founded to commercialize SIMSCRIPT, CACI International (NYSE: CACI) offers defense, intelligence, and IT solutions to support national security and government transformation efforts.

CACI reported revenues of $2.30 billion, up 13% year on year. This number surpassed analysts’ expectations by 0.5%. Taking a step back, it was a mixed quarter as it also produced a beat of analysts’ EPS estimates but a significant miss of analysts’ backlog estimates.

The stock is up 3.5% since reporting and currently trades at $493.

Read our full, actionable report on CACI here, it’s free.

Leonardo DRS (NASDAQ: DRS)

Developing submarine detection systems for the U.S. Navy, Leonardo DRS (NASDAQ: DRS) is a provider of defense systems, electronics, and military support services.

Leonardo DRS reported revenues of $829 million, up 10.1% year on year. This result met analysts’ expectations. It was a strong quarter as it also produced an impressive beat of analysts’ backlog estimates and full-year revenue guidance slightly topping analysts’ expectations.

The stock is down 12.5% since reporting and currently trades at $42.20.

Read our full, actionable report on Leonardo DRS here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.