Since July 2025, Bank OZK has been in a holding pattern, posting a small loss of 1.1% while floating around $46.54. The stock also fell short of the S&P 500’s 11.3% gain during that period.

Is there a buying opportunity in Bank OZK, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Why Is Bank OZK Not Exciting?

We don't have much confidence in Bank OZK. Here are three reasons there are better opportunities than OZK and a stock we'd rather own.

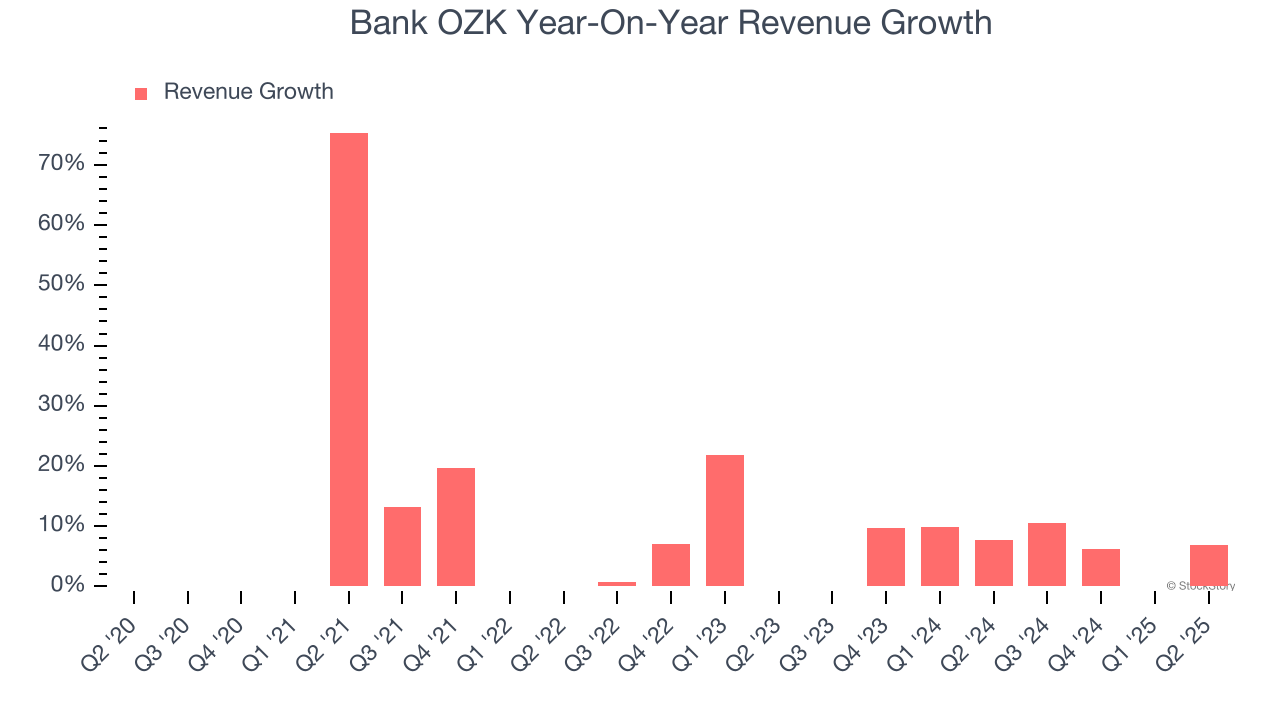

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Bank OZK’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 9.1% over the last two years was well below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

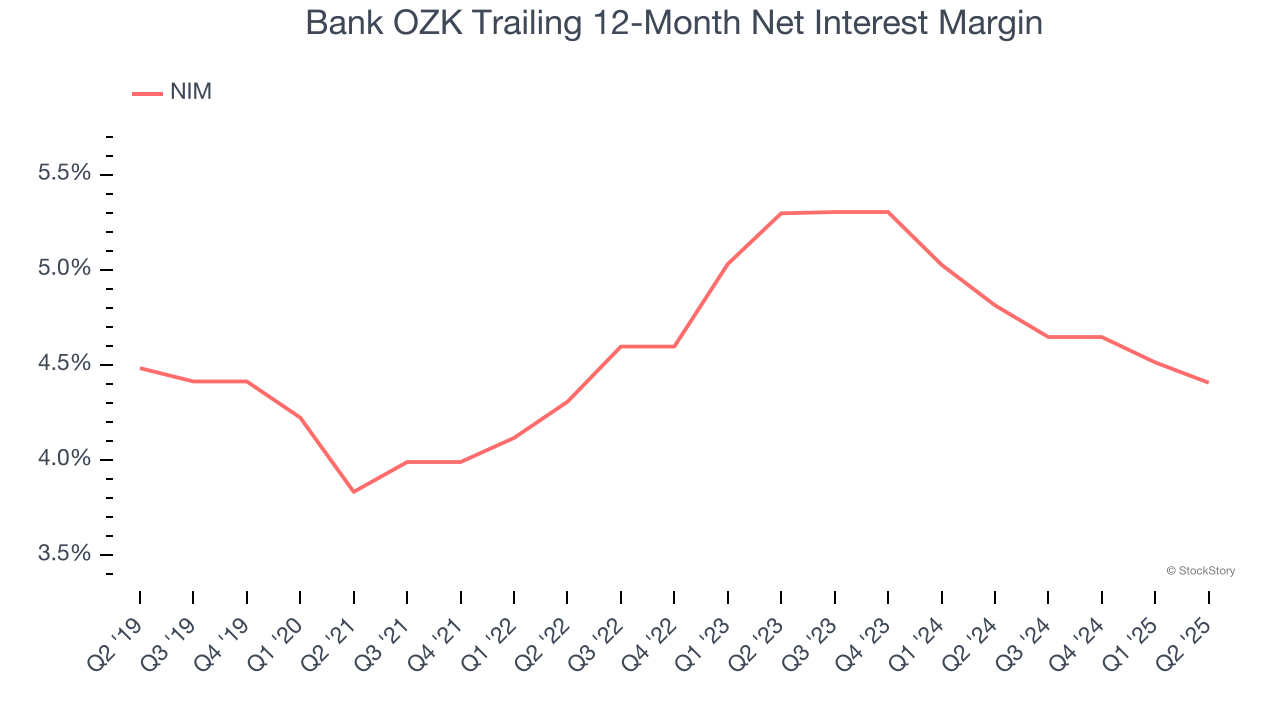

2. Net Interest Margin Dropping

Net interest margin (NIM) represents the unit economics of a bank by measuring the profitability of its interest-bearing assets relative to its interest-bearing liabilities. It's a fundamental metric that investors use to assess lending premiums and returns.

Over the past two years, Bank OZK’s net interest margin averaged 4.6%. However, its margin contracted by 89 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Bank OZK either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

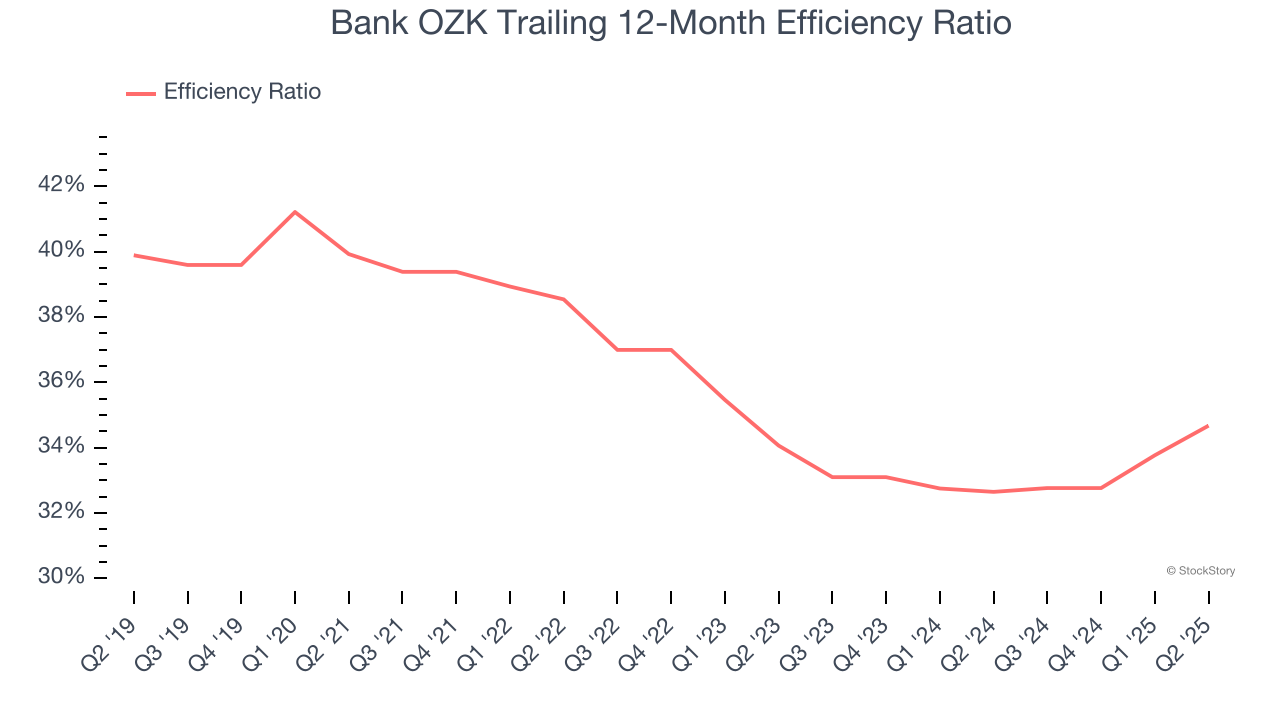

3. Efficiency Ratio Expected to Falter

The underlying profitability of top-line growth determines the actual bottom-line impact. Banking institutions measure this dynamic using the efficiency ratio, which is calculated by dividing non-interest expenses like personnel, facilities, technology, and marketing by total revenue.

Markets understand that a bank’s expense base depends on its revenue mix and what mostly drives share price performance is the change in this ratio, rather than its absolute value. It’s somewhat counterintuitive, but a lower efficiency ratio is better.

For the next 12 months, Wall Street expects Bank OZK to become less profitable as it anticipates an efficiency ratio of 37.6% compared to 34.7% over the past year.

Final Judgment

Bank OZK’s business quality ultimately falls short of our standards. With its shares trailing the market in recent months, the stock trades at 0.9× forward P/B (or $46.54 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. Let us point you toward the most dominant software business in the world.

Stocks We Would Buy Instead of Bank OZK

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.