Earnings results often indicate what direction a company will take in the months ahead. With Q3 behind us, let’s have a look at Monro (NASDAQ: MNRO) and its peers.

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

The 5 auto parts retailer stocks we track reported a satisfactory Q3. As a group, revenues were in line with analysts’ consensus estimates.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 10.5% since the latest earnings results.

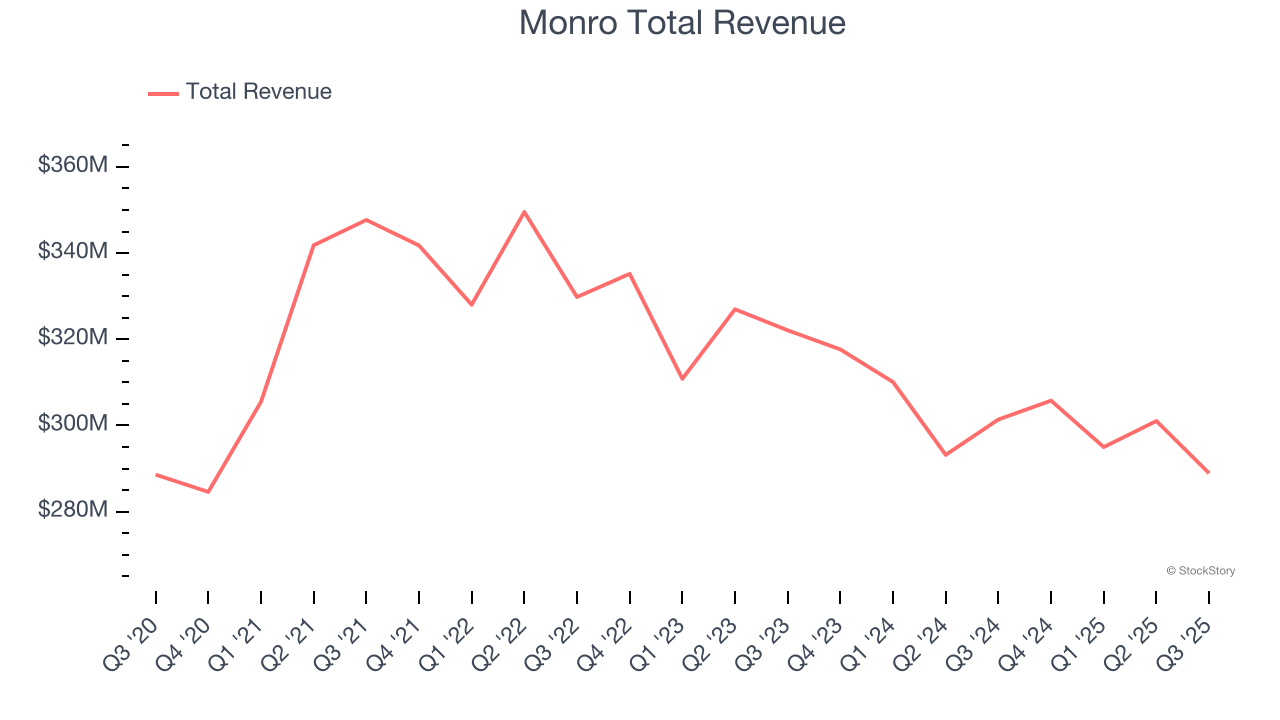

Monro (NASDAQ: MNRO)

Started as a single location in Rochester, New York, Monro (NASDAQ: MNRO) provides common auto services such as brake repairs, tire replacements, and oil changes.

Monro reported revenues of $288.9 million, down 4.1% year on year. This print fell short of analysts’ expectations by 2.8%, but it was still a strong quarter for the company with a solid beat of analysts’ EBITDA estimates and a beat of analysts’ EPS estimates.

Monro delivered the weakest performance against analyst estimates of the whole group. Unsurprisingly, the stock is down 15.5% since reporting and currently trades at $15.27.

Is now the time to buy Monro? Access our full analysis of the earnings results here, it’s free for active Edge members.

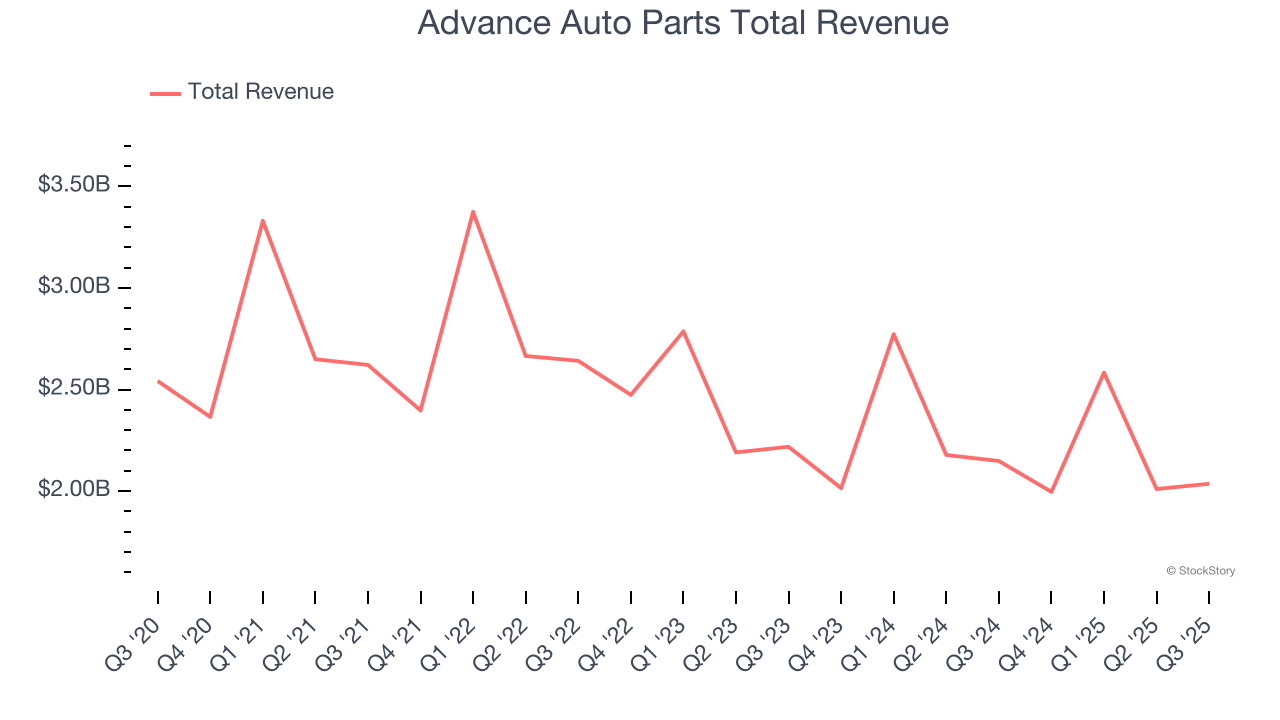

Best Q3: Advance Auto Parts (NYSE: AAP)

Founded in Virginia in 1932, Advance Auto Parts (NYSE: AAP) is an auto parts and accessories retailer that sells everything from carburetors to motor oil to car floor mats.

Advance Auto Parts reported revenues of $2.04 billion, down 5.2% year on year, outperforming analysts’ expectations by 0.7%. The business had a very strong quarter with an impressive beat of analysts’ EBITDA estimates and full-year EPS guidance exceeding analysts’ expectations.

Advance Auto Parts scored the highest full-year guidance raise among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 12.9% since reporting. It currently trades at $48.

Is now the time to buy Advance Auto Parts? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: AutoZone (NYSE: AZO)

Aiming to be a one-stop shop for the DIY customer, AutoZone (NYSE: AZO) is an auto parts and accessories retailer that sells everything from car batteries to windshield wiper fluid to brake pads.

AutoZone reported revenues of $6.24 billion, flat year on year, in line with analysts’ expectations. It was a slower quarter as it posted a miss of analysts’ EBITDA estimates and a miss of analysts’ gross margin estimates.

As expected, the stock is down 10.8% since the results and currently trades at $3,664.

Read our full analysis of AutoZone’s results here.

Genuine Parts (NYSE: GPC)

Largely targeting the professional customer, Genuine Parts (NYSE: GPC) sells auto and industrial parts such as batteries, belts, bearings, and machine fluids.

Genuine Parts reported revenues of $6.26 billion, up 4.9% year on year. This result beat analysts’ expectations by 2.2%. Taking a step back, it was a satisfactory quarter as it also logged a solid beat of analysts’ revenue estimates but full-year EPS guidance slightly missing analysts’ expectations.

Genuine Parts achieved the biggest analyst estimates beat among its peers. The stock is down 6.9% since reporting and currently trades at $122.69.

Read our full, actionable report on Genuine Parts here, it’s free for active Edge members.

O'Reilly (NASDAQ: ORLY)

Serving both the DIY customer and professional mechanic, O’Reilly Automotive (NASDAQ: ORLY) is an auto parts and accessories retailer that sells everything from fuel pumps to car air fresheners to mufflers.

O'Reilly reported revenues of $4.71 billion, up 7.8% year on year. This number met analysts’ expectations. More broadly, it was a mixed quarter as it also produced a beat of analysts’ EPS estimates but a slight miss of analysts’ EBITDA estimates.

O'Reilly delivered the fastest revenue growth but had the weakest full-year guidance update among its peers. The stock is down 6.5% since reporting and currently trades at $94.66.

Read our full, actionable report on O'Reilly here, it’s free for active Edge members.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.