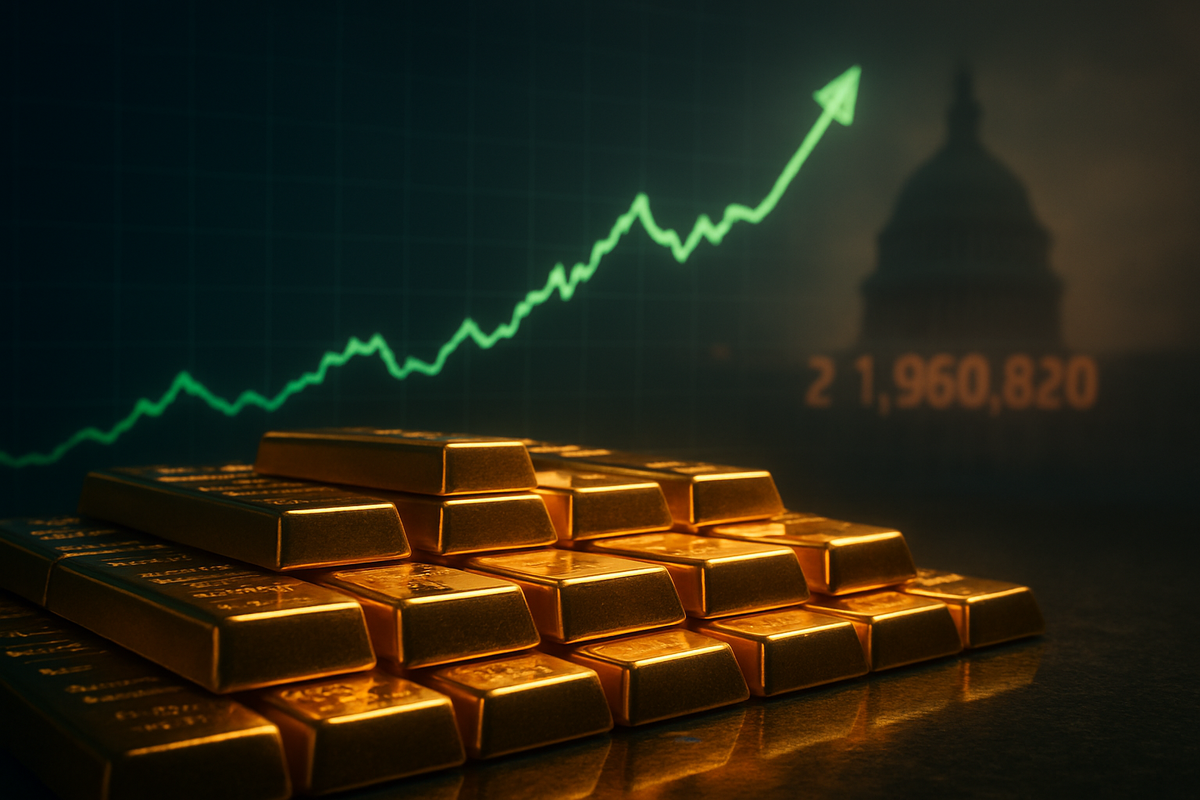

As of April 13, 2026, the global financial landscape is being reshaped by a relentless surge in precious metals, with gold prices hovering near historic highs of $4,725 per ounce. This extraordinary rally, which saw an intraday peak of $5,595 earlier this year, represents more than just a commodities boom; it serves as a stark barometer of investor anxiety regarding the stability of the U.S. dollar and the long-term viability of Western fiscal policy. With the U.S. national debt crossing the $39 trillion threshold and monthly interest payments rivaling the defense budget, the "flight to hard assets" has moved from a fringe strategy to a central pillar of institutional portfolios.

The immediate implications are profound, as the surging price of bullion ripples through the global economy. Central banks are accelerating their de-dollarization efforts, while retail investors are flocking to physical gold and exchange-traded funds to hedge against a "re-inflationary" cycle. This shift is not merely a reaction to short-term volatility but a structural adjustment to a world where the traditional "risk-free" asset—U.S. Treasuries—is increasingly viewed with skepticism due to mounting fiscal deficits.

A Timeline of Turbulence: From Geopolitics to the "Warsh Shock"

The path to $4,700 gold was paved by a series of escalating crises that began in early 2026. The primary catalyst was a direct military confrontation between the United States and Iran in late February, which threatened the Strait of Hormuz—a vital artery through which 20% of the world’s oil flows. As Brent crude prices spiked toward $150 a barrel, the "Global Energy Lockdown" fears sent the Consumer Price Index (CPI) to a 3.3% reading in March, the highest in two years. This energy-driven inflation made gold a mandatory hedge for any portfolio seeking to preserve purchasing power.

However, the rally found its true legs in the "Warsh Shock" of late March. The nomination of Kevin Warsh to succeed as the Chair of the Federal Reserve (NYSE: FED) introduced a period of intense monetary uncertainty. Investors scrambled to determine whether the new leadership would pivot toward aggressive tightening to combat the $1.2 trillion half-year fiscal deficit or succumb to the political pressure of servicing a massive debt load. By April 7, spot gold was trading at $4,685, and despite a fragile ceasefire announced in the Middle East on April 8, prices remained stubbornly high, settling in the $4,700–$4,733 range by mid-April.

The role of central banks during this period cannot be overstated. The World Gold Council has projected that official-sector demand will reach up to 900 tonnes for the full year of 2026. Dominant buyers like the People’s Bank of China have continued to aggressively add to their reserves, with China adding 25 tonnes in February alone. This sustained demand from emerging markets has created a structural floor for gold prices, preventing the sharp pullbacks that typically follow such meteoric rises.

The Corporate Divide: Winners and Losers in a High-Gold World

The primary beneficiaries of this environment have been the major gold mining corporations, which have seen their profit margins expand to record levels. Newmont Corporation (NYSE: NEM) has emerged as a clear winner, with its stock trading near $120 in mid-April, representing a staggering 122% total return over the past year. With an All-In Sustaining Cost (AISC) projected at roughly $1,680 per ounce, the current gold price of over $4,700 allows Newmont to generate unprecedented free cash flow, making it a "cash cow" for institutional investors looking for exposure to the S&P 500's only major gold producer.

Similarly, Barrick Gold Corporation (NYSE: GOLD) has seen its shares surge to approximately $43.55, a 136% increase over the previous 12 months. While Barrick has faced higher operational costs, with an AISC between $1,760 and $1,950 per ounce due to rising energy and labor expenses, the high realized price of gold has more than compensated for these headwinds. Other winners include specialized investment vehicles like the SPDR Gold Shares (NYSE Arca: GLD) and the iShares Gold Trust (NYSE Arca: IAU), both of which have seen massive inflows as investors seek liquid ways to participate in the rally.

On the losing side are companies sensitive to rising input costs and a weakening currency. Consumer discretionary firms and retailers are struggling as "re-inflation" eats into household budgets, while debt-heavy firms in the tech and real estate sectors face a "double whammy" of rising interest rates and a potential credit squeeze. Furthermore, companies that rely heavily on dollar-denominated international trade are finding their margins squeezed by the dollar’s perceived instability, as foreign partners increasingly demand payment in local currencies or gold-backed instruments.

Historical Echoes and the New Monetary Order

The events of April 2026 mirror historical precedents, such as the stagflationary era of the late 1970s, but with a modern, more systemic twist. Unlike previous rallies, this surge is deeply tied to the "fiscal dominance" of the U.S. government. With the national debt at $39 trillion, the Federal Reserve's ability to raise interest rates without triggering a sovereign debt crisis is severely limited. This has led to the emergence of what analysts call the "New Monetary Order," where gold is no longer seen as a "pet rock" but as a critical component of global reserve management.

The broader industry trend is one of "de-dollarization" and regionalization. The BRICS+ nations (including new members Indonesia and Malaysia) are increasingly using gold to settle trade imbalances, circumventing the traditional SWIFT system. This shift has regulatory implications, as Western governments may eventually face pressure to re-evaluate the role of gold in their own reserve accounts or implement "gold-link" policies to restore faith in their fiat currencies. The current crisis has effectively ended the era of "low-volatility inflation," forcing a total rethink of the traditional 60/40 portfolio.

The Path Ahead: Strategic Pivots and Scenarios

In the short term, the market is closely watching the Islamabad peace talks. If a permanent ceasefire is reached between the U.S. and Iran, a tactical pullback in gold to the $4,200–$4,500 range is possible as the "war premium" evaporates. However, long-term indicators remain overwhelmingly bullish. The primary challenge for the market will be the psychological barrier of $5,000 per ounce. If gold breaks and holds above this level, it could trigger a new wave of retail "FOMO" (fear of missing out), potentially pushing prices toward $6,000 by year-end.

For mining companies, the strategic pivot will involve managing the "cost creep" associated with higher energy and equipment prices. We may see an increase in mergers and acquisitions as larger players like Newmont and Barrick look to acquire junior miners to replenish their reserves in a high-price environment. Investors should also watch for the emergence of "digital gold" products and blockchain-based gold settlement systems, which are gaining traction as alternatives to the traditional banking system.

Summary: A Paradigm Shift in Value

The surge of gold in April 2026 is a clarion call for the global financial system. It underscores a fundamental shift in how value is perceived in an era of fiscal excess and geopolitical fragmentation. The key takeaway for investors is that gold has reclaimed its throne as the ultimate hedge against systemic risk. While the rapid price appreciation offers significant opportunities in the mining sector, it also highlights the fragility of the current monetary framework.

Moving forward, the market will remain highly sensitive to U.S. Treasury auction results and the rhetoric coming from the new Federal Reserve leadership. The lasting impact of this rally will likely be a permanent increase in gold's weighting within institutional portfolios. Investors should keep a close eye on central bank gold reserve reports and any signs of "fiscal consolidation" from Washington—though the latter remains a distant hope in the current political climate.

This content is intended for informational purposes only and is not financial advice.